In Defense of the Rally: Five Pros Who Say the New Bull Has Legs

In Defense of the Rally: Five Pros Who Say the New Bull Has Legs

(Bloomberg) --

It’s not hard to find people with a dim view of the stock rally. Just as many or more embrace it, and are happy to explain why.

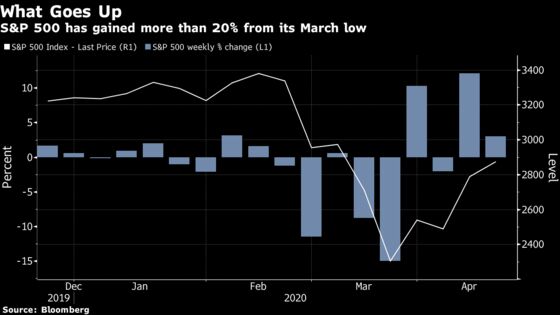

Conventionally defined, the S&P 500 is in a new bull market, having climbed 28% since mid-March. Indexes have closed higher for three weeks in four, with two of the advances exceeding 10%, a feat unseen since 1933. Gains in giant tech stocks have turned the Nasdaq 100 green for the year.

Believers are out there, pointing to unprecedented and swift actions by the Federal Reserve and Congress, and the propensity of markets to anticipate negative data and price it in. If earnings are your worry, take heart -- there were many periods when stocks surged while they tanked. Others cite progress on the coronavirus and a hopeful return to normalcy.

So forget the bear case, the view that it’s all a mind-boggling instance of perceptions coming unglued from reality, which may end up being the worst economic downturn since the Great Depression. While the economy is without a doubt taking a big hit, bullish arguments are winning out for now. Here are five views in the rally’s defense.

A Very Good Time

For anyone but the shortest-term tactical trader, Sean Naughton, senior vice president of U.S. equities at RBC Wealth Management, sees plenty of reasons why the S&P 500 still looks attractive near 2,800.

“If you have a three- to five-year type of time horizon, it’s still a very good time to be getting invested,” he said by phone. “Even at these levels with the rebound.”

After steep corrections like the S&P 500’s record 34% fall, forward returns are typically quite positive, according to his team’s analysis. When the Federal Reserve is aggressive with its actions, as it is now, stocks perform well, Naughton says. Interest rates are also extremely low, allowing for higher valuation multiples, and 2021 should see a more normalized earnings scenario.

Resilience In Asset Prices

At Pacific Life Fund Advisors, the team upped exposure to roughly 40% risk-on on March 20, three days before the stock-market lows. That helped the firm, which oversees $32 billion, turned around a quarter’s worth of underperformance in a week, as the S&P 500 embarked on a 27% rally.

At the time, the Newport Beach-based money manager believed assets were pricing in a deep recession, but not yet the stimulus unleashed to combat it. Max Gokhman, Pacific Life’s head of asset allocation, has been encouraged by muted market reactions to weak economic data. To up risk exposure even further, he’s eyeing economic data and earnings, the trajectory of the virus, and signs of more stimulus.

“If the market is moving down but not crashing when we get a bad surprise print, that’s a good sign that there’s greater resilience in asset prices,” Gokhman said of reactions to economic data. “Ultimately there will be more stimulus than was necessary which will in turn help growth as we get into the recovery phase in the back half of the year.”

Key Covid Trends

Markets in late February and early March started to anticipate negative economic data. They priced in an average recession and right now are primarily being driven by medical figures, many of which are improving -- including a flattening of the curve in major hot spots, says Deepak Puri, CIO Americas at Deutsche Bank Wealth Management, which had about EUR213 billion ($235 billion) in assets at the end of January.

“The S&P tends to lead GDP and other macro data so I’m not too shocked with the rally,” he said by phone. “The market is sensing that the social distancing measures that have been deployed have made a positive impact.”

To be sure, weak company earnings reports and guidance as well as a deterioration in medical trends could still cloud the outlook over the next couple of weeks. But stocks have already retraced 50% of their losses since the March low, which is a positive development. When that happens, the chance of plumbing new lows goes down “tremendously,” said Puri.

Looking ahead, an emergence out of the lockdown in a slow but normalized manner would be “the best news for the markets.”

Stimulus Support

Economists right now are struggling to project how intense the virus-induced recession will be in the U.S. While data released for March paints a frightful picture, most predict the biggest hit is yet to come. But Matt Lloyd at Advisors Asset Management is finding comfort in the massive Congressional stimulus package aimed at offsetting the declines in growth.

A 25% drop in GDP during the second quarter -- which, to be sure, would be the deepest such contraction on record -- would equal to an output cut of about $1.3 trillion. It’s not insignificant but it’s more than offset by the $2 trillion stabilization package intended to provide support to individuals, businesses and states and supersedes other losses, said the firm’s chief investment strategist in a phone interview.

“If you look historically, markets rebound in defiance of what the data is saying because they’re not looking right now -- they’re looking down the road,” he said. “Markets take uncertainty and price uncertainty usually a little bit greater, which is why we had such an exacerbated sell-off -- but then, conversely, why we rallied from those levels.”

Many fund managers currently have high cash balances they can deploy, said Lloyd. His firm, which had more than $33 billion in assets under management at the end of December, has favored municipal bonds and shorter-term investment-grade credit over the past month, among other things.

No Dichotomy in Reality

To Brent Schutte, chief investment strategist at Northwestern Mutual Wealth Management, the stock rally makes perfect sense, and its root cause is the fact that social distancing practices have worked so well to slow the virus’s spread. The way he sees it, the economic data has been so horrible because Americans have been “so good at performing our recommended treatment.” Now that the curve has flattened, dialog can turn to reopening the economy and getting back to work.

“There is no dichotomy in reality,” said Schutte, whose firm manages more than $161 billion. “We’re seeing bad data because good social distancing means a better virus outlook, less social distancing, leading to a rising market on the belief that the data will get better.”

©2020 Bloomberg L.P.