In Brexit Endgame, Complacency and Confusion Bedevil Markets

In Brexit Endgame, Complacency and Confusion Bedevil Markets

(Bloomberg) -- May’s deal, no deal, no Brexit at all. If only it were so simple.

With just a few months to go, Britain’s exit from the European Union still presents a baffling array of potential outcomes, including everything from the government being overthrown to a second referendum. And it’s testing the mettle of traders already worn down by two years of political anguish.

Right now, markets appear to have eased up on no-deal bets ahead of the Dec. 11 vote that threatens to torpedo Prime Minister Theresa May’s accord with the European Union. The calculation is that the chances of delaying or even ditching Brexit are increasing. Yet fresh waves of political uncertainty are likely to follow that vote, and there are fears investors may be living in a false sense of security.

“The endgame is very hard to predict,” said Pieter Jansen, a senior investment strategist at NN IP. “Markets are prepared for a soft Brexit outcome and approval of the deal would be a relief to financial markets. In case of a no deal uncertainty would obviously go up.”

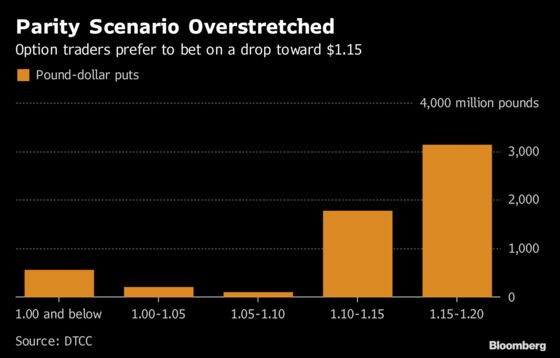

Keeping the Faith

The pound isn’t trading at levels that reflect a “more disorderly scenario,” Bank of England Governor Mark Carney said this week. In the central bank’s own grim assessment of a no-deal exit, sterling could slide by as much as a quarter, but foreign-exchange markets aren’t buying it.

Demand for sterling puts below parity with the dollar -- contracts giving the owner the right to sell a certain amount of the currency at a set price -- represent just half a percentage point of the total traded since September, according to DTCC data.

Put simply, most traders aren’t preparing for the pound to fall below the greenback, as Carney’s prediction implies. Instead, the bulk of the trading activity is for puts between $1.20 and $1.30. Sterling was at $1.2776 as of 4:26 p.m. in London. Even the contracts below $1.20 are concentrated at $1.10 and above.

“Although the odds are clearly against Theresa May, we do not think the markets have yet fully priced in a defeat,” Morten Lund, analyst at Nordea Bank AB, wrote in a note.

He expects the pound to tumble by as much as 4 percent against the euro if May fails to get her deal through Parliament in the first round. The FTSE 100 would also drop amid the political upheaval, offsetting the boost to the local value of overseas earnings from a weaker currency, according to the Nordea strategist.

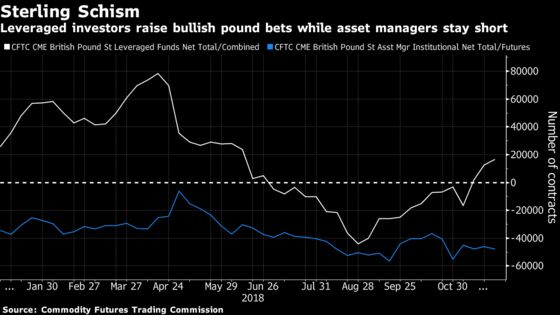

Sterling Stress

The biggest action for a no-deal outcome is playing out in the sterling options market -- but it’s hard to glean a clean signal.

While the cost of hedging over the next two weeks remains close to 2018 highs, euro-pound risk reversals, another barometer of sentiment, have eased closer to average levels notched last year. The same metric for pound-dollar on a one-week horizon is climbing -- suggesting investors are easing up on their negativity.

Meanwhile, fast-money traders have flipped to long sterling positions of late, in contrast to asset managers.

“I think there is a lot of confusion in the pound market” reflecting the frenetic newsflow and Brexit brinkmanship, said Jane Foley, head of FX strategy at Rabobank.

Traders in the interest rate market are showing no more certainty. They’re no longer pricing a rate hike next year as a sure thing, in a sign of doubts that a deal will be reached protecting the U.K. economy.

Since the day before Brexit Secretary Dominic Raab resigned -- plunging May’s campaign to sell her deal to colleagues into crisis -- the odds of a 25 basis-point rate increase by the end of 2019 have tumbled from more than full-priced to 76 percent, according to data compiled by Bloomberg. Traders pushed back wagers on the next rate hike to May 2020.

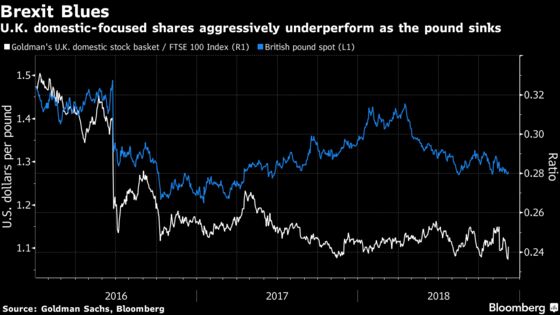

‘Uninvestable’

With a torrent of outflows and ever-falling valuations, stock investors have given up hope that a withdrawal agreement in the current form will be passed. The FTSE 250 Index is down by about 17 percent from a peak in June.

For good reason. The never-ending political distress has turned the U.K. equity market into no-go territory, with euro-area stocks offering better rewards, according to Sanford C Bernstein Ltd.

“We think that the U.K. market might be ‘uninvestable’ in the specific sense that the near term movement is likely to be dominated by political forces that, bluntly, are very hard to model,” strategists including Inigo Fraser Jenkins wrote in a note last month.

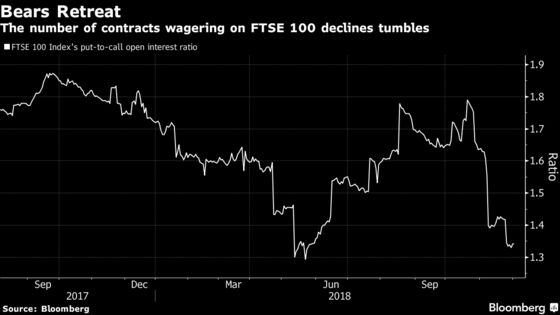

Ain’t So Bad

Yet key pockets of equity derivative markets remain unbowed.

Even after a spike during Thursday’s broad market sell-off, the FTSE 100’s volatility remains below this year’s high and is still trading beneath that of the Euro Stoxx 50 and the S&P 500.

On a six-month horizon, covering the U.K.’s exit from the EU in March, implied price swings for large caps have jumped to February levels -- which were spurred by the U.S. equity rout -- but remain below the referendum peak.

U.K.-listed multinationals offer cheap valuations with protection from further weakness in the sterling. That might explain muted demand to bet against the asset class, with the put-to-call ratio -- the volume of outstanding bearish contracts versus bullish -- tumbling ahead of Theresa May’s make-or-break vote.

All told, conviction trades wagering on either doomsday or a reprieve seem to be off the table amid the waves of uncertainty lashing investors of all stripes. As a result, markets risk sleepwalking into a shock.

“The tail risk of a hard Brexit is being underestimated by market participants,” David Riley, chief investment strategist at BlueBay Asset Management, told Bloomberg TV last week. “The consensus is still a deal will be done. I think that’s too much complacency, just as there was before the actual Brexit vote itself.”

--With assistance from David Goodman, Vassilis Karamanis, Justina Lee, Tanvir Sandhu, James Hirai and Francine Lacqua.

To contact the reporters on this story: Sid Verma in London at sverma100@bloomberg.net;Samuel Potter in London at spotter33@bloomberg.net

To contact the editors responsible for this story: Samuel Potter at spotter33@bloomberg.net, Cecile Gutscher

©2018 Bloomberg L.P.