Icahn’s ‘Beautiful Trade’ Pays Off Early With Malls Shut

Icahn’s ‘Beautiful Trade’ Pays Off Early With Malls Forced Shut

(Bloomberg) -- Eastview Mall, 14 miles southeast of downtown Rochester, New York, was a rare bright spot among regional shopping centers.

A fixture in the area for almost 50 years, it served a thriving community, with jobs in health care and at the nearby university. And it had so far managed to survive the trends that were killing off other malls: the relentless rise of online shopping, over-leveraged retail chains and shifting populations.

Now, nothing is showing at Eastview’s Regal Cinema. Plans to convert the space once occupied by Sears into a Dick’s Sporting Goods are on hold. PF Chang’s is still open, but only for takeout and delivery, including beer.

With the Covid-19 pandemic forcing stores to remain closed, some of them aren’t paying landlord Wilmorite, a family-owned real estate developer. Wilmorite, in turn, missed about $820,000 of mortgage payments due in April, filings show.

“Eastview is in a good financial situation and we are looking forward to supporting our tenants and reopening as soon as possible,” Wilmorite spokeswoman Janice Sherman said in an email, noting that most tenants are asking to defer their rent payments for three months. The landlord, in turn, is seeking the same forbearance from its lenders, she said.

While similar stories are unfolding across the U.S., what makes Eastview’s stand out is its role in one of Wall Street’s most closely watched trades, with billions of dollars on the line.

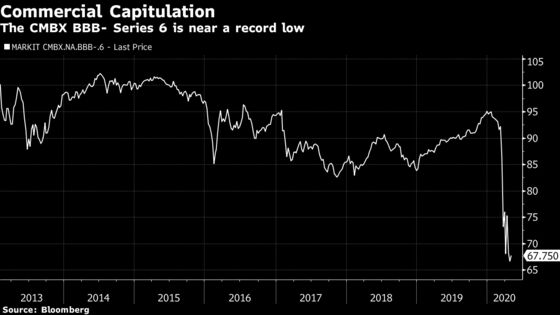

The $210 million loan is one of the largest in deals referenced by the CMBX 6, a derivatives index that investors use to bet on the future of brick-and-mortar retail in the country. With businesses shuttered from Maui to Maine, the CMBX has cratered.

“We expected this trade to play out over one to two years,” said Dan McNamara, a principal at MP Securitized Credit Partners, which has a short position on the index, meaning the firm benefited from the decline. “In reality, it played out in one to two months.”

The CMBX trade gained prominence in 2017, when firms including Deutsche Bank AG and Morgan Stanley recommended short bets as waves of retailers filed for bankruptcy. The credit-default swaps indexes, the first of which debuted in 2006, are tied to commercial mortgage-backed securities containing real estate of all kinds. Series 6 of the index, linked to debt issued in 2012, has outsize exposure to shopping malls, making it appealing to traders who want to short the retail sector.

As of March 20, traders had wagered a net $9.4 billion on the BBB- slice of CMBX 6, and an additional $2.3 billion on the junk-rated portion of the index, according to the International Swaps & Derivatives Association. Billionaire Carl Icahn became a vocal short seller, and a well-timed bet helped Apollo Global Management Inc.’s flagship credit hedge fund to a 6% gain through early April. Mutual fund giants Putnam Investments and AllianceBernstein Holding LP have taken the other side of the trade, wagering that malls will withstand the changing retail environment. Both declined to comment.

“We have billions and billions of dollars on the short side of this,” Icahn said last week in an interview with Bloomberg Television. “It really is a beautiful trade on a risk-reward basis.”

The performance of the index has been mixed in recent years. While one-time retail powerhouses like J.C. Penney Co. and Sears Holdings Corp. shuttered stores, bruising the CMBX 6 in 2017 and 2018, it rebounded the following year as the U.S. economy remained strong, with the unemployment rate touching a 50-year low. The commercial mortgage bonds that underpin the index also are exposed to office and hotel loans, which had been more resilient and mitigated some of the retail pain before the pandemic.

Hedge fund Alder Hill, which had been short the CMBX 6 since at least early 2017, shuttered last year as losses on the trade piled up.

But the forced shutdown of businesses has caused investors to flee mortgage securities, with worries about overdue rent mounting. Mortgage servicers cited Covid-19 in commentaries on more than 600 commercial real estate deals that were delinquent in April, according to data tracked by Bloomberg.

As for those who managed to stick with their shorts, the stampede has brought redemption.

McNamara’s MP Securitzed Credit Fund, which lost 37% in 2019, surged 53% in the first quarter.

Cuomo’s Order

The longer the shutdown lasts, the better that bet will look.

New York Governor Andrew Cuomo has extended his stay-at-home order to many parts of the state until the middle of May, while saying a case could be made for reopening some regions sooner than others.

“There’s about $1 trillion of mortgage debt that underlies the shopping-center industry,” said Tom McGee, chief executive officer of the International Council of Shopping Centers. “If it somehow becomes unserviceable, it’s going to create an enormous strain on capital markets and communities.”

Even as other parts of the commercial mortgage market struggle, there are signs that a retail recovery might be particularly prolonged. Just one-third of American adults said they’ll feel safe shopping in a mall after stores reopen, according to an April 20 survey by First Insight Inc., a retail analytics firm.

Still, shares of mall operators climbed this week after reports that Simon Property Group Inc. plans to reopen dozens of malls in states that are easing stay-at-home restrictions.

Deutsche Bank analyst Ed Reardon, citing the limited ability of mall owners to reposition their properties for other uses, said lenders could lose 80 to 90 cents on the dollar. Such catastrophic losses “will basically wipe out” the subordinate, or riskiest portions, of CMBS deals with exposure to large retail loans.

Eastview Mall is a case in point. It’s among the largest loans in two CMBX 6 referenced deals. It performed well before the pandemic: Even as some tenants went bust, they were quickly replaced and occupancy had averaged more than 90% since 2012.

The mall, a 20-minute drive from the University of Rochester, serves a relatively affluent population. The median annual household income within a 3-mile radius exceeded $125,000 in 2011, when the loan was originated. It employed about 3,800 people and generated $10 million a year in municipal and county sales taxes, according to the Finger Lakes Times, a local newspaper.

Wilmorite, the mall owner, was founded in the 1940s by brothers James and William Wilmot and is still run by the family. It owns several shopping centers in the Rochester area and beyond, as well as interests in construction and gaming.

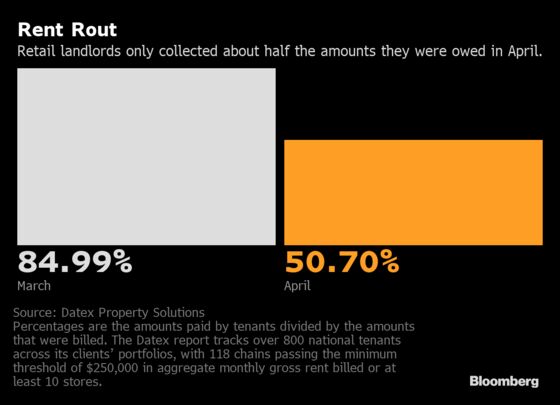

Now, at least a dozen Eastview tenants are behind on their rent, according to Datex Property Solutions, a real estate industry research firm. They include Regal Cinemas, Ann Taylor, Staples, Gap and Foot Locker. The Datex data show that landlords they track collected just 51% of their usual payments in April, compared with 85% in March.

That number may be poised to drop further.

“The more big-name companies that say ‘I’m not paying’ -- it creates a ripple effect,” said Lindsay Dutch, a Bloomberg Intelligence analyst.

While some landlords have managed to tap other sources of cash to make their payments, that will be increasingly difficult the longer the shutdown persists.

“Landlords can probably cover some lost revenue,” Dutch said, but “having excess cash and liquidity to lean on is going to be key.” More landlords will almost certainly fail to make mortgage payments next month.

If the shutdown ends soon and stores open, Eastview and other malls that have missed payments could still recover. But some investors with short positions said they believe the crisis is already fundamentally changing Wall Street’s view of brick-and-mortar retail.

“I don’t think that Covid did anything besides speed up what was inevitable,” McNamara said. “If the storm in 2008 was the residential mortgage market, the storm in 2020 is certainly going to be in the commercial mortgage market.”

The BBB- tranche of the CMBX index tumbled 29% this year through Tuesday, not far from a record low of 65 on March 23.

“We’re still trying to figure out how far this thing could drop,” McNamara said.

©2020 Bloomberg L.P.