Huarong Posts $15.9 Billion Loss as Leverage Hit 1,333 Times

Huarong Posts $15.9 Billion Loss in 2020, Flags Asset Sales

(Bloomberg) -- China Huarong Asset Management Co.’s long-delayed 2020 results showed a record loss, with leverage hitting 1,333 times and capital buffers far short of the regulatory minimum, emphasizing the difficult task ahead for the bad-debt manager that recently secured a government bailout.

Huarong reported a 102.9 billion yuan ($15.9 billion) loss for all of last year, slashing shareholder equity by nearly 85%, according to a Sunday exchange filing. The company booked 107.8 billion yuan in impairments and suffered a 12.5 billion yuan loss on financial assets. While it returned to a small profit in the first half this year, Chairman Wang Zhanfeng said the firm will apply to the regulator for temporary tolerance with key capital measures below requirements as of June.

After five months of turmoil since it delayed its earnings report in March, China’s biggest bad debt manager this month secured a rescue package from some of the nation’s biggest financial firms. Its plight had become the biggest test in decades of whether Beijing would still shield state-owned firms from market forces amid a renewed push by President Xi Jinping to rein in debt growth as defaults have hit records.

“The company may only have just taken the first steps out of the woods,” said Jason Tan, a senior analyst at CreditSights Singapore LLC. Its journey back to “full health” will probably be “a bumpy and arduous one, dependent on shoring up core business operations in distressed debt management and shrewd divestments of non-core business units,” he said.

The firm said on Sunday that it plans to dispose of subsidiaries with non-core business activities in the “near future” to increase internally generated fund inflows and to replenish capital. It cut its non-financial local and offshore units to 13 from 27 through 2020.

Huarong is still working with its strategic investors on the details of a recapitalization, Wang said during a Monday conference call, adding that more companies may be join the original group. He didn’t provide further clarity on the bailout.

State-owned investors including Citic Group, China Insurance Investment Co. and China Life Asset Management Co. on Aug. 18 agreed to put fresh capital in Huarong. The firm would receive $7.7 billion as part of an overhaul plan with control shifting to Citic from the Finance Ministry, though details were still being finalized and could change, people familiar with the matter have said.

Significant Impact

A review of assets and risks last year “had a significant impact on the operating results and is a harsh lesson to be learned in the development history of the company,” Wang said in the earning report. “What is gone is gone, but go for what to come. We will learn from the lesson and take it as valuable experience and the desire to move forward.”

The company said by implementing measures including asset sales and a capital boost it can ensure operations for the next 12 months.

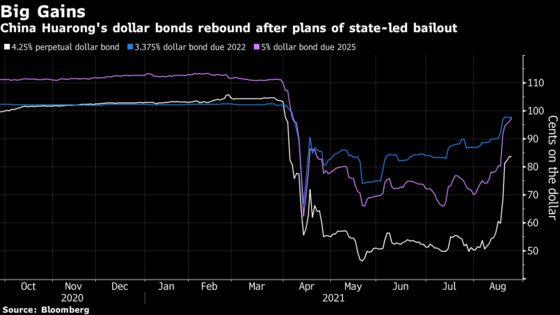

Huarong’s longer-dated dollar bonds rose Monday. The firm’s 4.25% perpetual note climbed 1.3 cents on the dollar to 87.4 cents, its highest price since early April, Bloomberg-compiled data show.

Huarong has $238 billion in different liabilities -- including more than $20 billion of offshore bonds -- and has drawn close scrutiny from investors across the world.

The company’s borrowings amounted to 782 billion yuan as of June 30, of which those coming due within one year amounted to 578 billion yuan. It warned that the significant decline in operating performance and its financial condition may trigger immediate repayment of about 17.9 billion yuan.

Huarong’s capital adequacy ratio slumped to 4.16% at the end of last year and stood at 6.32% as of June 30. Chinese regulators demand a minimum 12.5% for bad loan asset managers, and at least a 9% core tier-1 ratio. Its leverage ratio, calculated as interest-bearing debt to equity, fell from 1,333 to 37.1 as of June 30. That’s still four times higher than its level at the end of 2019 and compares with 6.8 times at major rival China Cinda Asset Management Co.

“We will move from making quick bucks to earning slow and hard money for the long-term,” Huarong President Liang Qiang said in the conference call.

Huarong’s auditor Ernst & Young expressed reservations on the company’s income and cash flow statements for 2020, as it was unable to obtain “sufficient appropriate audit evidence” to ascertain whether any of the associated gains and losses recognized by Huarong in 2020 should have been recorded in previous years.

Moody’s Investors Service last week cut Huarong’s credit rating to Baa2, two levels above junk, and put it on watch for a potential further downgrade, citing deterioration of its capital and profitability. The projected 2020 loss “could result in a failure to comply with the minimum regulatory requirements on capital adequacy and leverage, and indicate that the company cannot sustain its operation without support arranged by the government.”

The firm’s shares, which will remain suspended from trading, have slid 67% since their debut. Before it went public in 2015, it was backed by heavyweights including Warburg Pincus and Goldman Sachs Group Inc.

Huarong has been effectively frozen out of the bond market since the second quarter, even as the company has been servicing its debt on time and reached agreements with state-owned banks to ensure it can meet obligations through at least the end of August. The firm assured investors this month that it has no plan to restructure its debt and has made preparations for future bond payments.

While defaults at state-owned Chinese companies have become more common in recent years, none of the borrowers that missed payments have been as systemically important as Huarong. Aside from its close link to China’s central government and complex web of connections to other financial institutions, Huarong is also one of the country’s biggest issuers of offshore bonds that sit in portfolios from Hong Kong to London and New York.

If Huarong lost its investment-grade credit rating, 56% of surveyed fund managers that hold its dollar bonds would be forced to sell, according to a Bank of America report dated Aug. 17.

Huarong, together with Cinda, China Great Wall Asset Management Co. and China Orient Asset Management Co., was created to buy bad loans from banks in the aftermath of the Asian financial crisis, when decades of government-directed lending to state companies had left China’s biggest lenders on the brink of insolvency.

The bad-debt firms later expanded beyond their original mandate, creating a labyrinth of subsidiaries to engage in other financial businesses and borrow billions from the bond market. Huarong was the most aggressive of the four under former Chairman Lai Xiaomin, who was executed in January for crimes including bribery.

©2021 Bloomberg L.P.

With assistance from Bloomberg