How RBA’s Easing Backfired in a Flash Crash for Aussie Bonds

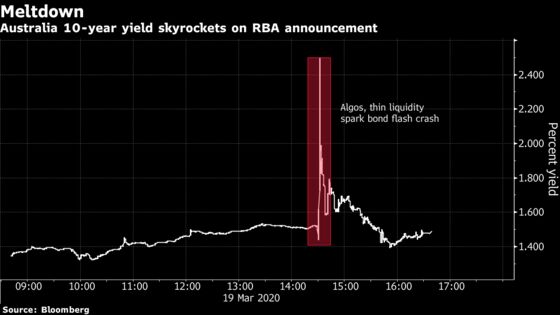

The nation’s benchmark 10-year bond yield surged to a record intraday gain of 128 bps, only to plunge 90 bps minutes later.

(Bloomberg) -- Just when investors thought central banks were beginning to calm a global bond rout, the epicenter of chaos shifted to Australia as its market went into meltdown on March 19. The trigger was the announcement of the country’s own quantitative easing program, which should have soothed nerves, not frayed them.

The episode underscores the continuing vulnerability of markets as policy makers push into uncharted territory to protect their economies from a viral pandemic they have never faced before. While the worst of the violent price moves were over in minutes, the impact is still reverberating. Low liquidity, algorithmic trading and a mismatch between investor expectations and the central bank’s plan all played a role.

The day began with traders digesting the aftermath of a roller-coaster session in Europe and the U.S., and preparing for the main event Down Under: the Reserve Bank of Australia’s emergency meeting.

What followed was unprecedented. Wild moves saw the nation’s benchmark 10-year bond yield skyrocket to a record intraday gain of 128 basis points, then plunge more than 90 basis points minutes later.

“The whole thing reeks of a flash crash,” said Chris Weston, head of research at Pepperstone Group in Melbourne. “There was disappointment the RBA didn’t give quantifiable numbers to bond purchases, liquidity was almost impossible, bid-offer spreads were blown out -- the statement was the trigger.”

Here’s a snapshot of how the action unfolded, in local time in Sydney:

2:00 p.m.

Traders and fund managers gathered at their desks to await the RBA’s decision due in 30 minutes.

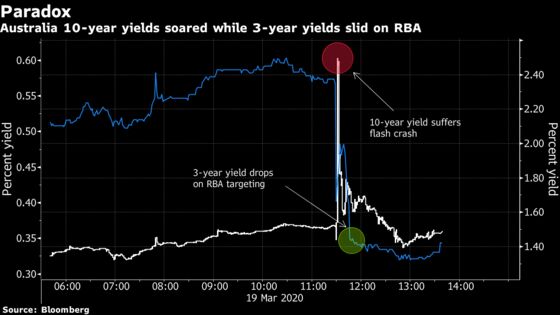

One of them was Antares Capital portfolio manager Tano Pelosi, who had observed a steady rise in the three-year Australian bond yield since morning. As yields started climbing toward an intraday high of 0.60%, Pelosi started to buy.

“That part didn’t make sense to me, that three-year bonds were underperforming leading up to 2.30, when yield-curve control was likely coming for the short-end,” he said. “I traded.”

2:15 p.m.

Nomura Holdings Inc. strategist Andrew Ticehurst was at his computer screens, flanked by on-edge sales traders, more than 40 stories above Sydney’s central business district in the Governor Phillip Tower.

“I was strapped to my desk, speaking to traders and clients,” said Ticehurst, who had recommended investors buy shorter-dated government debt to prepare for QE.

While the three-year yield was hovering near its intraday high, the 10-year was holding steady around 1.50%.

2:30 p.m.

RBA headlines flashed across news screens. The central bank had cut interest rates and set a 0.25% target for the three-year yield.

Yields on these securities plunged more than 10 basis points in little more than a minute to about 0.40% as traders scrambled to buy the bonds.

2:31 p.m.

With the RBA’s focus seemingly limited to the shorter maturity debt, 10-year yields headed in the opposite direction with alarming ferocity. In the blink of an eye, they clocked up the record intraday gain of 128 basis points.

Algorithms look to have accelerated a move that got started when one or two large sell orders came through amid low liquidity, several market participants said.

Many investors couldn’t keep up.

“It just happened so fast,” said AMP Capital Investors Ltd.’s Shane Oliver, who was tracing the action from his office on Alfred Street, a stone’s throw away from Sydney Harbour. “My initial reaction was that the RBA focusing on the three-year part of the curve was a bit of a mistake -- it would have made more sense to anchor the longer-end. That’s how markets too clearly had interpreted it.”

2:33 p.m.

No sooner had the yield reached 2.50% than it was coming back down. More than 50 basis points of the drop came in a minute.

At Nomura, traders were yelling news headlines and trying to fathom the wild moves. “The market has very poor tolerance for surprises, especially when liquidity was already so poor,” said Ticehurst. “It showed on Thursday.”

2:35 p.m.

More headlines scrolled across screens, saying that the RBA would buy bonds across the curve. Still elevated, the 10-year yield kept working its way lower, but at a more reasonable pace.

“Markets took a little bit of a breather and comfort from the statement, and the algos I think settled,” said Pepperstone’s Weston. “The fact that yields came down pretty much straight away suggested it was a liquidity issue -- still, some might have had a very painful trade from that.”

3:00 p.m.

The Australian Stock Exchange said it had fielded cancellation requests as a result of the yield spike, though after some investigation traders were told that all their trades would stand.

3:30 p.m.

As markets digested the RBA’s plans, bond yields across the curve started to settle.

The three-year had fallen to 0.33%, hovering above the central bank’s new target, while the 10-year calmed around 1.50%.

As the afternoon wore on, Antares’ Pelosi saw an opportunity to enter a curve flattener-position. He’d already had made a tidy profit on the three-year trade in the morning.

“It was pretty crazy,” said Pelosi, who earned a PhD in economics at the University of New South Wales. “It wouldn’t shock me if we see more wild times ahead -- these are pretty unprecedented times we’re living in.”

©2020 Bloomberg L.P.