One Bond Fund Is Returning 10% Without Going the Way of H2O

How One Bond Fund Is Returning 10% Without Going the Way of H2O

(Bloomberg) -- Richard Hodges is happy to tell you he can beat the market without the exotica that has gotten more eminent investors into trouble.

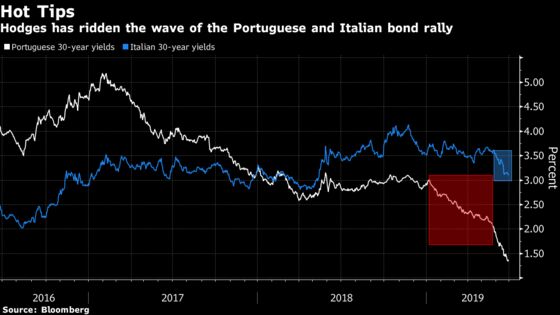

Investing in widely held and easily traded assets -- such as government bonds from Italy and Portugal -- his Global Dynamic Bond Fund has returned 10% this year, putting it in the top percentile among its peers.

“My fund performance has shot the lights out,” Hodges, head of total return fixed income at Nomura Holdings Inc.’s asset-management arm, said in an interview. “We’re not doing the same as other people to generate a level of income. We’ve not moved into private credit assets. I’ll never hold a private credit asset.”

That’s how Natixis SA’s H2O Asset Management unit and star stock picker Neil Woodford have gotten into trouble; funds like theirs even earned a rebuke from Bank of England Governor Mark Carney. H2O’s portfolios hemorrhaged $7 billion in five days after it was found to be holding a number of illiquid bonds tied to a controversial businessmen, Lars Windhorst. Woodford had to freeze withdrawals as clients exited, having invested in small, unlisted companies.

In contrast, Hodges says he can liquidate 40% of his fund in two minutes should things get hairy. The sovereign bonds that are his key holdings have surged this year as central banks across the globe ramp up plans to inject money back into their stalling economies.

Portuguese debt has been his top performer, carrying the fund, after he bought 30-year bonds in January. These have posted equity-beating returns this year of more than 30%. Yields tumbled nearly 150 basis points before Hodges then sold them all for Italian 15- and 30-year securities three weeks ago.

Since then, Italy’s debt has been on a tear, with 30-year yields dropping about 50 basis points, as the potential for European Central Bank interest-rate cuts and further quantitative easing gives traders a green light to bet on bonds. The position is not without risk -- Italian assets were battered during a budget dispute with the European Union last year.

Twelve percent of the $420 million portfolio is now tied up in Italy, according to Hodges -- a bet that investors will continue to overlook the nation’s simmering politics and snap up some of the highest-yielding government debt in the euro area. Longer-maturity bonds are also better protected against any flaring tensions, and yields can fall another 50 basis points in the next four months, he said.

“It’s criminal this fund is less than $1 billion,” 51-year-old Hodges said over coffee in the City of London, where he heads up the four-person fund. “It should be an awful lot bigger than it is.”

Juicing Returns

Hodges’ first job as a Eurobond settlements clerk at Chase Manhattan Securities coincided with the “Big Bang” in 1986, the rapid deregulation of financial markets under then U.K. Prime Minister Margaret Thatcher. His near 30-year career as a fund manager took him through the financial crisis and the collapse of Lehman Brothers, as well as a multi-decade bull run in bonds.

He gained a lesson in risk after a motorcycle crash in 2011 left him with titanium plates in his left arm and right leg. He continued to manage his fund from the Royal London Hospital in Whitechapel, while it took three years of physiotherapy to walk properly again.

“It made me more humble and appreciate the uncertainty,” he said.

Money managers have been pushed to take bigger risks by the meager returns on offer following unprecedented monetary easing in the past decade, with benchmark yields turning negative in Germany, France and the Netherlands this month. Funds have been increasing leverage to juice returns, or snapping up privately placed bonds, which prove tricky to shift when investors pull their cash.

H2O has announced plans to jettison the controversial holdings and park them in a new portfolio for “deep value” securities to stem outflows and bolster confidence in its funds. Natixis’ shares are down 10% since June 19.

“Investor Neil Woodford’s liquidity troubles, Natixis’ share-price slide and GAM’s 2018 bond-fund suspensions have all raised scrutiny of fund liquidity and transparency,” wrote Jonathan Tyce and Georgi Gunchev, analysts at Bloomberg Intelligence. “Fast-growing funds’ risk of style-drift, clarity on the type of underlying asset, and quality and liquidity of investments are critical questions.”

Lot Underwater

While Italy’s bond market has been hit by volatility and illiquidity, Hodges would be able to dissolve 87% of the fund within a day, and 98% of it in under seven days, assuming normal market conditions, according to Arkus Financial Services, a third-party advisory firm. While Morningstar Inc. suspended and then downgraded its rating of H2O’s Allegro fund, which had returned 28% last year, Nomura’s Global Dynamic Bond Fund retains a five star rating.

BOE Governor Carney this week slapped the wrist of investment funds that hold illiquid assets but allow unlimited withdrawals, saying that they “are built on a lie.” The structure of funds, such as H2O, might also be systemic to the system, he added.

For Hodges, more funds might find themselves beset by the same problems that roiled H2O and Woodford’s Equity Income Fund, given the pressure to beat the market. He has outperformed funds operated by Amundi SA and Allianz SE, and posted double the returns of his peers based on data compiled by Bloomberg.

“You buy these assets, you leverage that and that’s where you generate 30%-plus returns when everyone else is not,” said Hodges. “This is just the tip of the iceberg. The iceberg is very broad and there’s a hell of a lot of it underwater.”

--With assistance from Tanvir Sandhu, Nishant Kumar and Lucca de Paoli.

To contact the reporter on this story: John Ainger in London at jainger@bloomberg.net

To contact the editors responsible for this story: Ven Ram at vram1@bloomberg.net, James Hertling, Neil Chatterjee

©2019 Bloomberg L.P.