How Investors' Gloomy Take on Japan May Be Upended by Inflation

How Investors' Gloomy Take on Japan May Be Upended by Inflation

(Bloomberg) -- The Abenomics trade is so 2013. Foreign investors haven’t been much interested in Japan lately, despite the strongest economy in two decades. What could turn that around, some market observers say, is a surprise revival of inflation.

While the official consumer price index rose at just half of policy makers’ 2 percent target in the latest reading, less-watched gauges suggest cost pressures are building. Prices paid by services companies are climbing the most since the early 1990s, as is worker compensation. Rents are accelerating in major cities, led by Tokyo. As companies start passing those costs along, and generalized inflation takes hold, investor attention could pick up.

“Investors generally agree that Japanese companies have become more focused on improving profit margins and gradually increasing shareholder returns,” but this hasn’t caused them to view Japan’s market more constructively, said Jaewoo Nakajima, a research analyst at Evercore ISI in New York. “Signs of inflation acceleration may be the big consensus shifter.”

While Japanese stocks have been caught in the global sell-off that hit equities this month, the Nikkei 225 Stock Average at the start of October touched its highest level since 1991. That’s a testament to record profits among the nation’s companies and an investment-driven rebound in growth that’s helped pull unemployment down to the lowest in more than a quarter century this year.

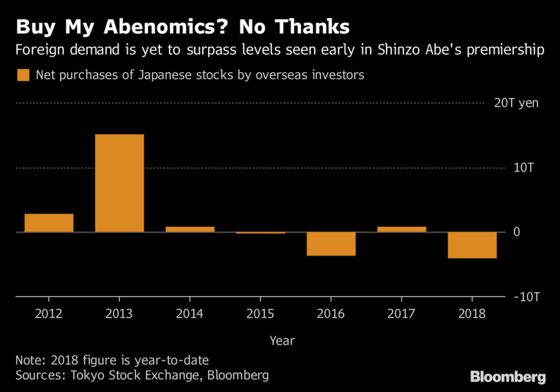

Despite all that, Japanese equities trade at the cheapest relative to global peers since 2002 on a price-to-book value basis. And foreign investors have yanked about 4 trillion yen ($36 billion) out of the market, according to Tokyo Stock Exchange data, on track for the third year of net sales in the past four.

It’s a big change from when overseas fund managers were big buyers of Prime Minister Shinzo Abe’s reflation program. Buying peaked at 15.1 trillion yen in 2013, the year when Abe proclaimed “buy my Abenomics!” at the New York Stock Exchange.

Analysts at UBS Group AG’s wealth management arm, once convinced that Japan’s tight labor markets would spur its stocks, abandoned that call last week. While the dynamic will change the economy and corporate culture in time, for now consumption is “relatively weak” and households are boosting savings, so a slower earnings outlook may dull investor interest, they wrote in a note.

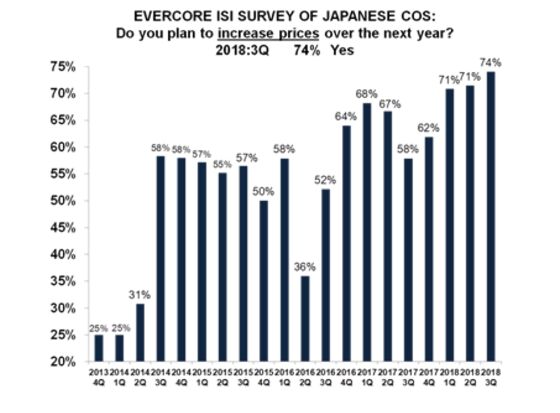

But corporate culture may already be shifting. Surveys by Evercore ISI indicate a steady increase in the proportion of companies expecting to raise prices over the coming year. The latest reading was 74 percent for the third quarter.

Other indications of reflation progress include a 7.6 percent jump in Tokyo office rents last month compared with a year earlier, according to data from Miki Shoji Co., a property agent. Evercore ISI notes accelerating gains in Osaka, Nagoya and Fukuoka as well. Nationwide producer prices are also on the up, with the services industry seeing the fastest gains -- stripping out sales tax hikes -- since before deflation took hold in the mid-1990s.

Morgan Stanley strategists are among those anticipating an improving environment for Japanese stocks. They calculated in a note last month that return on equity has more than doubled from before Abenomics, to 9.8 percent, with more gains to come. With costs rising, companies are ramping up capital spending. With this type of “self-funded” growth, ROE is seen rising in the bank’s base case to 12 percent by 2025.

“The success of the turnaround will become embedded in market pricing, which it is not today,” the strategists led by Jonathan Garner wrote. Among their “overweight” recommendations are builder Komatsu Ltd., developer Mitsui Fudosa Co. and East Japan Railway Co.

--With assistance from Toshiro Hasegawa.

To contact the reporters on this story: Adam Haigh in Sydney at ahaigh1@bloomberg.net;Gregor Stuart Hunter in Hong Kong at ghunter21@bloomberg.net

To contact the editors responsible for this story: Christopher Anstey at canstey@bloomberg.net, Cormac Mullen

©2018 Bloomberg L.P.