The Rise of the East European Billionaires

The Rise of the East European Billionaires

(Bloomberg) -- They own superyachts and a team in your favorite league. They mingle with movie stars and meddle in politics. They control vast amounts of wealth and, sometimes, their nation’s future.

Oligarchs, billionaires and business tycoons have come to represent eastern Europe as surely as the endless steppe, the concrete block flats or the proverbial Polish plumber.

And just a generation ago they didn’t even exist. They emerged from the rubble of communism as centrally planned economies gave way to open markets and widening income gaps.

In 1989, it became clear that there was no going back. Thirty years ago this month, Romanians revolted and the country’s communist dictator was executed, while former dissident Vaclav Havel became Czechoslovakia’s president. In the final days of the year, Poland’s president signed a new economic program that opened the door to capitalism and became a blueprint for much of the region’s transformation. The Soviet Union would last another two years but the empire had collapsed.

As the shackles of communism fell away, countries in what was once called the Eastern Bloc rushed into the brave new world of open markets. With it, came a generation of new tycoons and oligarchs from Almaty to Prague, from Moscow to Zagreb. Many of them have become legendary for their extravagant lifestyles or political influence. And even three decades on, the list of the region’s richest still has a Soviet tint.

“Many of those who had power under Communism maintained it under the new structure,” Mark Mobius, the veteran emerging-market investor who set up Mobius Capital Partners LLP last year after three decades at Franklin Templeton Investments, said by email. “The difference is that with a market oriented system some of the old apparatchiks could not adjust to the new regime and faded away while new and young entrepreneurs rose up.”

Half of the wealthiest people in the region come from a group that was close to power at the end of communism, benefited from privatization—or both. Self-made billionaires are rarer, poorer and mostly hail from countries that had fewer resources and were weaker politically.

Their rise—and sometimes fall—tells the story of eastern Europe’s transformation in the past 30 years. Their tales offer a glimpse into this unique period of history.

Late 1980s

The Early Birds

Economic decline was a major driving force behind the political upheaval—by the 1980s, many countries were forced to give up on lavish social programs or go deep into debt to maintain them. As the end of the decade approached, narrow openings appeared for private investors to take advantage of cash-starved governments. The process was largely unplanned, unstructured, haphazard and benefited those in the know.

Petr Kellner, Czech Republic

Net Worth: $12.8 billion

Born in Czechoslovakia in 1964, Kellner studied economics and was selling Ricoh photocopiers shortly after the Communist Party fell in the 1989 Velvet Revolution. His life changed when the newly capitalist state started selling assets in a unique scheme: it handed vouchers to the public, exchangeable for shares in companies. To take advantage, Kellner and his partners in 1991 set up what became PPF Group, in which he now controls about 99%.

Using vouchers and a loan, PPF started accumulating assets and built a 20% stake in Ceska Pojistovna, the country’s largest insurer, which he later made profitable—and the bedrock of his wealth. He cashed out in 2013, selling the insurance assets to Italy’s Generali in a $3.3 billion deal.

PPF’s operations span finance, telecommunications, biotech, real estate and engineering. Its Home Credit Group unit is one of the largest consumer lenders in central and eastern Europe, and has expanded into China, Vietnam, India, Indonesia, the Philippines and Kazakhstan.

Kellner rarely appears in public. In an interview 17 years ago, he painted the post-communism world as “a definite opportunity that perhaps will never repeat itself.” Kellner told the Prague newspaper Mlada Fronta Dnes: “I was able to find capable people, judge risks and make short-term sacrifices for long-term projects.”

Mid-1990s

Asset Grab

For early democratic governments, the sale of state assets to private investors became a cornerstone of economic programs. They craved foreign currency, idealized western know-how and were eager to shed the cost of subsidizing failing legacy industries. It gave unprecedented momentum to the first wave of private asset accumulation in the region for almost a century. The process took on many forms, from direct bidding to stock listings. In the run-up to Russia’s first post-Soviet presidential election, Boris Yeltsin’s struggling government borrowed from a group of bankers, referred to as the oligarchs, pledging as collateral—and later forfeiting—shares in major industrial assets.

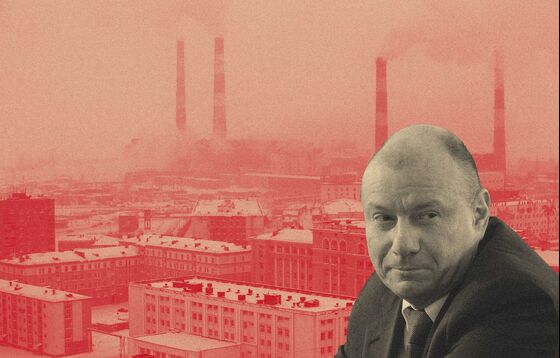

Vladimir Potanin, Russia

Net Worth: $28.5 billion

Only a few of Russia’s original “oligarchs” continue to wield power and the country’s richest man is one of them. Potanin, 58, was already powerful enough during Yeltsin’s presidency to shape economic policy.

A graduate of Moscow’s uber-elite State Institute of International Relations, Potanin worked in foreign trade, which gave him a headstart as the economy opened up. His main holding company, Interros, was registered in 1990, before the Soviet Union collapsed.

Potanin quickly formed one of capitalist Russia’s first banking empires and was a driving force behind Yeltsin’s now infamous loans-for-shares scheme, which distributed key assets between a handful tycoons in the mid-1990s.

“Private property was supposed to be the medicine, the only alternative to the failed state administration,” Potanin said in an interview. “Effective owners don’t appear out of nowhere. For them to appear, state assets had to be transferred into private hands.”

In late 1995, Potanin and his then business partner Mikhail Prokhorov gained a dominant stake in Norilsk Nickel, the world’s largest refined nickel and palladium producer, for just over $170 million. While the privatization process has been criticized, it’s how the assets are now managed that is important, Potanin says. The company’s capitalization has climbed to more than $40 billion, and his almost 35% stake makes up the biggest part of his fortune.

The following year, Potanin helped Yeltsin’s campaign attain a surprise re-election victory over a Communist rival and was appointed deputy prime minister in charge of the economy and state property. He resigned in less than a year.

With his resource wealth, Potanin weathered financial crises in 1998 and 2008, and he adjusted to the new reality of Vladimir Putin’s rise to power. The two Vladimirs now sometimes play hockey together in a promotional league that features famous athletes, politicians and business leaders.

1990-2000

Wild East

The previously closed economies threw their doors open to foreign goods and investors, and allowed those who’d escaped the socialist camp to return. Many turned to hustling and trading after the system they’d been raised in turned into a capitalist free-for-all. The arrival of western companies was celebrated as a validation of government policies, the fastest route to revamp dilapidated industries and create a business culture. Those views grew more jaded as time went on, with some coming to view investors as economic colonizers interested only in cheap labor and an expanded consumer base.

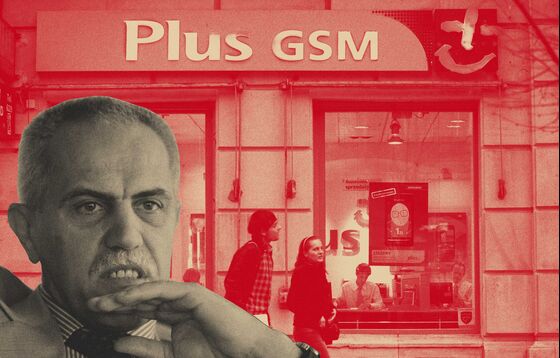

Zygmunt Solorz, Poland

Net Worth: $2.7 billion

Poland’s richest man has been evasive about his early days behind the Iron Curtain. Legend has it that the man of many names—born in in a city 100 kilometers (62 miles) south of Warsaw as Zygmunt Krok—once made a living selling cemetery candles. The story hasn’t been confirmed.

What’s known is that by his early twenties he’d made it to Germany via Austria and set up a transport company. He used a friend’s name, Piotr Podgorski—friends still call him Piotrek—when he registered as a refugee, to shield his family back in closed-off Poland. In the 1980s, he took yet another name, becoming Solorz after his first wife, and for a while he was known as Solorz-Zak, adding the hyphen during a second marriage.

In the 1980s, he sold cars and other goods from the West in Poland. After the communist regime fell, Solorz returned and began building his empire, starting the country’s first and biggest private television network, Telewizja Polsat SA, in 1992. His holdings now include Cyfrowy Polsat SA, one of the largest digital platforms in Europe, a retail bank, and Polkomtel, the country’s second-largest mobile phone operator, which he bought in a record M&A deal. He’s also planning to build Warsaw’s most exclusive residential district.

The media-shy billionaire, who owns lignite-fueled power plants, surprised Poles this year when he spoke out publicly as a climate advocate, starting a charity to fight pollution and giving more airtime to environmental issues. It’s unclear, though, if he went as far as giving up his favorite means of transport, a helicopter.

1990-2000

Family Ties

While the more than two dozen countries that emerged from the rubble of communism all espoused democratic ideals, for some western alignment was an afterthought and local strongmen kept hold of the reins. With them rose a well-connected business class, many with family ties.

Timur Kulibayev and Dinara Kulibayeva, Kazakhstan

Net Worth: $5 billion

There’s no lineage more prestigious in central Asia than Dinara’s: she is the middle daughter of Nursultan Nazarbayev, Kazakhstan’s president from 1990 until March, the country’s leader for life, and the man after whom the country’s capital is now named.

The family has also done well in business: Dinara is considered the richest woman in the country. She and her husband, Timur, control financial institutions including Kazakhstan’s biggest lender, agricultural and oil trading businesses, and real estate developments at home and in Dubai.

Dinara studied theater in Moscow and earned an MBA at home. Timur went to university for economics, also in the Russian capital, and later worked at the state oil and gas producer. He served as chairman of the country’s sovereign wealth fund, Samruk-Kazyna, until 2011 and sits on the board of the Russian gas giant, Gazprom.

Timur has a reputation for being a shrewd negotiator, once described by U.S. diplomats as a “manicured billionaire.” He has influence over large swaths of the economy as head of a powerful energy lobby and chairman of the largest Kazakh business chamber.

1998

Devaluation, Crash, Contagion

Russia’s default on domestic debt and devaluation of the ruble in 1998 capped years of economic mismanagement. Banks collapsed, and with them people’s savings once again disappeared overnight. The effects reverberated through the region’s young capital markets, shaking trust in the new system and gutting a generation of potential retail investors. It also cleared space for those who weathered the crisis to expand their empires.

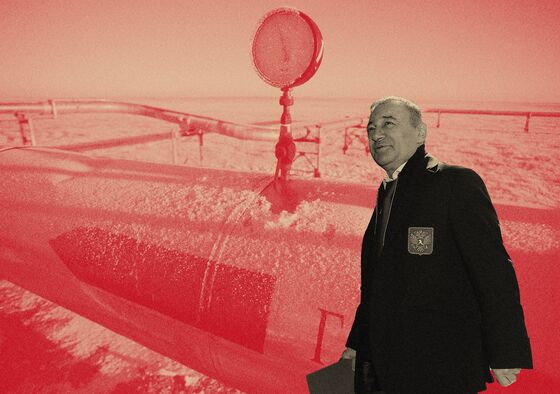

Andrey Melnichenko, Russia

Net Worth: $15.2 billion

Melnichenko, one of the ten richest Russians, was too young to benefit from privatization. Instead, he made his fortune in the next economic upheaval. While studying physics at Moscow State University, he started trading currencies with classmates, which led to the creation of MDM Bank.

Unlike many bigger rivals, MDM came through the 1998 crisis nearly unscathed, thanks to a conservative credit policy, the lack of illiquid assets and no exposure to government bonds. As competitors went under, the lender snagged some of the biggest Russian companies as clients.

The turmoil also helped MDM take a leap as it started buying assets from oligarchs who’d run into trouble. The first was the Volzhsky pipe plant, acquired from Mikhail Khodorkovsky’s Menatep bank. It kicked off a new phase of expansion under the MDM Group umbrella into steel pipe production, fertilizers, and coal.

“My vision then was to consolidate fragmented assets in risky and then-derelict industries and create leading international blue chips in new areas,” Melnichenko said by email through a representative. “I saw an opportunity to invest into industrial assets, fertilizer and coal production. These industries were not considered to be ‘strategic’ for Russia and were not subject to the political influence that dominated other sectors, like oil and gas, diamond and gold mining.”

Melnichenko’s luck stayed with him in the 2008 crisis. Just a year earlier, he and his business partner, Sergei Popov, split up their holdings. Melnichenko got the industrial assets, including fertilizer-maker EuroChem and coal miner SUEK, which were less exposed to turbulence in financial markets. Popov agreed to sell the bank to a larger rival in 2015.

Early 2000s

The Rise of Putin

As the first decade after Communism ticked down, an ailing Yeltsin searched for a successor to stem the chaos as Russia’s economy lurched from crisis to crisis. On New Year’s Eve in 1999, Yeltsin resigned in favor of a former KGB colonel, Putin, who quickly set out to reshape the country’s power structure. Within three years, he had crushed the oligarchs’ political independence. Power-broker Boris Berezovsky and media magnate Vladimir Gusinsky fled the country. In 2003, Mikhail Khodorkovsky, once the richest Russian, was arrested and jailed on tax evasion and fraud charges. A year later, the government began selling off parts of his oil company, most of which now belong to state-owned Rosneft. After a decade in prison, Khodorkovsky was pardoned by Putin in December 2013. He now lives in London where he funds a vocal opposition group.

The shift in power also gave rise to a new class of billionaire that’s continued to thrive as Putin rounds out two decades of power.

Arkady Rotenberg, Russia

Net Worth: $2.1 billion

Arkady Rotenberg was born in Leningrad in 1951. In his youth, he met and befriended Putin through judo. Rotenberg later worked as an instructor in the martial art and after the collapse of the Soviet Union organized competitions around the country. Eventually, he headed a club founded by billionaire Gennady Timchenko, where Putin was the honorary chairman.

Rotenberg began building a business empire after Putin rose to the presidency. In 2001, he acquired a stake in SMP Bank, which was sanctioned by the U.S. after Russia annexed Crimea. In 2007, he founded Stroygazmontazh, a gas pipeline construction company, with his younger brother, Boris Rotenberg, who also became a billionaire.

The brothers acquired five companies a year later, and in 2014 controlled the main pipeline-builder for Gazprom, Russia’s biggest gas exporter. Their company, which also built the bridge that connects Russia with Crimea, was reportedly sold to Gazprom affiliates in 2019.

Like Potanin, Rotenberg plays hockey with Putin and isn’t shy about his loyalty to his onetime judo mate. “We have been friends, and we’ll remain friends no matter what happens,” Rotenberg said in a recent interview with RT.

2004-2013

EU and the World

As Putin consolidated power in Russia, former allies in eastern Europe fixed their gazes westward. They worked toward joining the European Union and NATO, revamped legal systems and harmonized business practices. In waves between 2004 and 2013, 11 former communist countries joined the EU and five adopted the euro. More open and flexible economies and easy access to a market of 500 million people helped the foster the rise of the self-made billionaire.

Ivan Chrenko, Slovakia

Net Worth: $1.4 billion

Chrenko, born in Sala, Czechoslovakia in 1967, made it big in real estate almost by accident. His first business in the newly independent Slovakia, selling audio equipment, floundered and as he wound up the company, he was left with a warehouse to sell. That deal gave him a start in the property market.

By the middle of the 1990s, Chrenko was in the thick of it. His company, HB Reavis, constructed its first office building in the young nation’s flourishing capital, Bratislava. The developer eventually struck gold with Aupark, a shopping mall in the city center.

At the end of 2005, a little more than a year after Slovakia entered the European Union, the bloc’s largest owner of shopping centers—Netherlands-based Rodamco Europe NV—bought half of the complex. Eventually, HB Reavis raked in almost 400 million euros ($440 million) including dividends on its initial investment of 77 million euros.

The proceeds let Chrenko levy opportunities as borders and financial barriers crumbled. HB Reavis now has more than $2 billion of assets under construction, with projects from London and Berlin to Warsaw and Budapest.

Chrenko himself stays out of the spotlight. He stepped down from the chief executive position in 2013 and doesn’t give interviews. While HB Reavis lists dozens of executives on its website, the chairman appears only at the very bottom of the page, listed as a non-executive board member.

2008-2009

More Crisis and Contagion

After two decades, eastern European countries had integrated themselves into the global economy. The temptation to borrow in dollars or euros to expand left them exposed to the global credit crunch of 2008 and 2009. While the sudden weakness of western competitors offered some opportunities, the ensuing economic slowness undermined the emergent consumer economy.

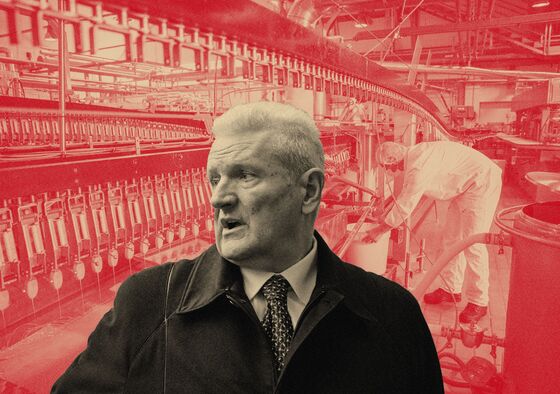

Ivica Todoric, Croatia

Bankrupt

Croatia’s one-time richest man, Todoric was the founder, owner and manager of Agrokor dd, once the biggest company in the Balkans. He weathered the fall of communism, the wars that tore apart Yugoslavia and, for a while, the 2008 global crisis.

Todoric and his father started out trading flowers in the business friendlier climate of late 1980s Yugoslavia and then expanded into the food business.

With the fall of communism came demands for independence that erupted into the deadliest wars Europe had seen in 50 years. Todoric rode out the turmoil and bought property from the state in privatization sales, often working closely with the government to thrive in the newly formed Croatia and other nations carved out of the former Yugoslavia in the second half of the 1990s.

Over the next two decades, Todoric kept expanding. The 2008 financial crisis, which tipped Croatia’s economy into six years of zero growth, didn’t slow his ambitions. In 2014, he set out to buy Slovenia’s biggest retail chain, Mercator. The steep interest rates he accepted to finance the deal proved to be a bridge too far: in 2017 the government undertook the financial restructuring of Agrokor and Todoric was removed as head of the company.

The same year, Todoric fled to the U.K. as authorities in Croatia investigated his role in Agrokor’s demise. He was extradited to Zagreb in December 2018, and the case remains open. Agrokor, meanwhile, changed its name and is now owned by its former creditors—including Russia’s biggest banks.

2010s

Populist Wave

The 2008 crisis did more than destroy wealth, it also destroyed many illusions about capitalism. The disenchantment and economic pain ushered in a new type of politician: the eastern European populist. Spearheaded by Hungary’s Prime Minister Viktor Orban, they position themselves as ready to right the wrongs of the previous decades, in part by redistributing wealth.

Lorinc Meszaros, Hungary

Net Worth: $1.5 billion

A former schoolmate of Orban, Meszaros started a small gas-fitting company in their home village of Felcsut in the 1990s. Unknown on the national stage, he started a stratospheric rise after his childhood friend became prime minister in 2010, quickly climbing to the top of the country’s rich list.

Meszaros himself once said that his rapid ascent may be because he’s smarter than Mark Zuckerberg—and attributed his wealth to God, luck, and Orban.

“I never had any business relations with the prime minister, our relationship is private in nature,” Meszaros said by email. “I’ve known Viktor Orban since his childhood. I respect what he has achieved and consider him a friend.”

Meszaros is the president of a sprawling soccer academy Orban founded near his weekend house and owns top-flight teams in Hungary and Croatia. His businesses, consolidated mostly under the holding company Opus Global, range from construction to media and wineries and are frequent winners of government contracts.

2014-2019

Sanctioned Russia

Tensions between Russia and the West blew up in Ukraine, putting the country on front pages across the globe for much of 2014. Protests broke out in November 2013 after the government failed to sign an economic accord with the EU in favor of ties with Russia. The demonstrations turned deadly in 2014, with more than 100 killed, and the pro-Russian president fled the country. That year, Putin annexed Crimea, and Kremlin-backed forces helped foment a separatist insurgency in Ukraine’s east. Western countries responded with economic sanctions, targeting officials and executives, as well as a number of the oligarchs who emerged in the past 30 years. In just a generation, the billionaires became chess pieces in a geopolitical game.

In waves, more sanctions were added, including limits on technology transfers to Russia and the ability of state-controlled companies to raise long-term funds internationally. The U.S. administration headed by President Donald Trump—who had pledged during his campaign to improve ties with the Kremlin—imposed the harshest measures yet in 2018, and punishing several billionaires and their companies, roiling markets.

Oleg Deripaska, Russia

Net Worth: $3.4 billion

A winner of the “Aluminum Wars,” Deripaska grew rich in the 1990s. Later, his family ties also helped—he married the daughter of Yeltsin’s chief of staff.

Deripaska started a massive international expansion before the 2008 crisis, buying stakes in the construction giant Strabag SE and Magna International Inc, the world’s biggest car parts manufacturer. Through his flagship company United Co. Rusal he also acquired a stake in Norilsk Nickel.

“The ’90s were a time of chaos and opportunities and they were as transformative for me as they were for the country,” Deripaska said by email. “I was very young at the time and very enthusiastic. I was never given any assets. What I have, I made myself.”

The 2008 crisis left Deripaska badly wounded. The debt he took on to finance the expansion left him exposed to margin calls. The Norilsk Nickel purchase, coupled with falling aluminum prices pushed Rusal to the verge of bankruptcy: the company went through a $17 billion debt restructuring, still the biggest in Russian corporate history.

Then came Crimea. The international fallout led to a currency collapse, suddenly inflating the ruble value of Rusal’s dollar revenue. That was great news for Deripaska, until last year. The U.S. imposed sanctions on most of his companies, including Rusal, in effect halting Rusal’s ability to sign new contracts and sell advanced products. Rusal shares plummeted, and the global aluminum market went into shock.

Intense lobbying—and the global supply change implications—helped eventually lift the sanctions on Rusal, though not Deripaska himself. To help his companies, the tycoon agreed to cut his stakes below control and quit management.

“The U.S. sanctions are nothing more than shameless personal attacks on individuals to give the appearance of taking strong action against Russia,” Deripaska said.

The sanctions were imposed over Russia’s “range of malign activity around the globe” and because the “government operates for the disproportionate benefit of oligarchs and government elites,” U.S. Treasury Secretary Steven Mnuchin said in a statement at the time.

These days, Deripaska is trying to get sanctions lifted from his automotive business in exchange for cutting his stake. He has also taken an interest in archaeology and is supporting the largest dig in Russia, on the Black Sea coast.

--With assistance from Zoltan Simon, Marton Eder, Gordana Filipovic, Nariman Gizitdinov, Jasmina Kuzmanovic, Ott Ummelas, Wojciech Moskwa, Milda Seputyte, Irina Reznik, Irina Vilcu, Slav Okov, Maciej Martewicz, Radoslav Tomek and Tom Maloney.

To contact the editor responsible for this story: Torrey Clark at tclark8@bloomberg.net, David MerrittPierre Paulden

©2019 Bloomberg L.P.