How China’s JPMorgan Wannabe Became a $34 Billion Debt Risk

CMIG’s liquidity crunch is caused by what analysts describe as combination of mismanagement, tighter lending conditions in China.

(Bloomberg) -- It was supposed to be China’s answer to JPMorgan Chase & Co.

But less than five years after China Minsheng Investment Group Corp. embarked on plans to become a financial colossus, the company has instead turned into a symbol of the turmoil sweeping China’s once-vaunted private sector. CMIG shocked investors when it missed a bond payment on Jan. 29, and markets remain jittery about the company even after it scraped together enough cash to repay the overdue note on Thursday.

CMIG’s liquidity crunch, caused by what analysts have described as a combination of mismanagement and tighter lending conditions in China, underscores a sometimes overlooked risk to the global economy in the era of Trump, Brexit, and trade wars. As China reins in the shadow-banking system that supported its private sector with cheap credit for more than half a decade, companies that were meant to be pillars of the nation’s growth miracle are proving surprisingly fragile.

“CMIG is not an isolated case,’’ said Fan Wei, vice general manager of the fixed-income department at Shenwan Hongyuan Securities Co. “Many Chinese companies face declining investment returns and refinancing difficulties that have plunged them into debt woes.’’

For now, CMIG has avoided becoming one of China’s biggest-ever defaulters. Shanghai Clearing received a payment for its 3 billion yuan ($443 million) overdue note on Thursday, people familiar with the matter said.

China’s government has stepped in to help resolve CMIG’s liquidity problems, according to the 21st Century Business Herald, which reported that the company plans to introduce strategic investors and has signed deals to dispose of some assets.

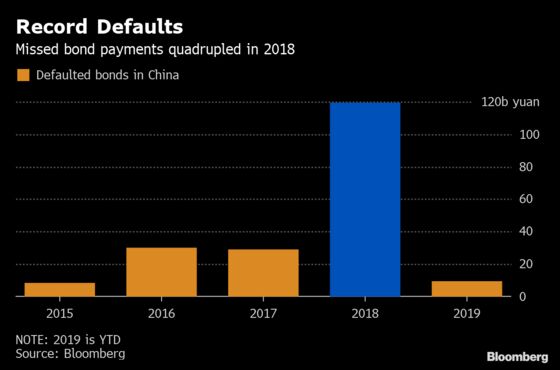

Whether or not CMIG gets its $34 billion debt load under control, analysts say China’s record string of defaults is far from over. The risk is that investors sharply curtail funding to non-state borrowers, which represent more than 60 percent of annual output and 80 percent of employment in the world’s second-largest economy.

CMIG shows how rapidly sentiment can turn. Founded in 2014, the company is the brainchild of Dong Wenbiao, the former chairman of China’s largest non-state bank who’s known as the “godfather’’ of the nation’s private sector. Billing CMIG as a Chinese version of JPMorgan, Dong convinced 59 non-state companies to join forces as the company’s founding shareholders. He even won an endorsement from Chinese Premier Li Keqiang.

CMIG expanded quickly into industries spanning finance, real estate, health care, aviation and energy. Like HNA Group Co. and other non-state conglomerates that have run into cash shortages in recent years, CMIG often financed itself with short-term debt.

Its total obligations more than doubled in less than four years, while cash holdings amounted to just 1 percent of liabilities as of June, according to Shanghai Brilliance Credit Rating & Investor Service Co. The company’s funding eventually dried up as its investments struggled and shadow banks pulled back because of tighter regulation and slowing economic growth.

“CMIG’s business model was flawed even with the very capable Dong Wenbiao at the helm,’’ said Zhou Dewen, deputy head of the China Association of Small and Medium Enterprises, who has studied private businesses for more than three decades.

Calls to Dong, who retired as CMIG chairman last year, went unanswered. The People’s Bank of China and the Shanghai government didn’t immediately respond to faxed requests for comment.

Investors are watching CMIG closely for clues on how Chinese authorities respond to the prospect of a major private-sector default. While policy makers have been trying to avoid the moral hazard associated with government-orchestrated bailouts, they face growing pressure to prop up struggling businesses as the economy slows and China’s trade spat with U.S. President Donald Trump rumbles on. Over the past few months, Chinese leaders have announced a flood of policies to help reduce private sector costs and make financing more available.

With a record 5.9 trillion yuan of debt coming due in 2019, including 33.6 billion yuan from CMIG, the question is whether China’s non-state companies can convince investors to stick with them. It won’t be easy, said Lv Pin, a fixed-income analyst at Citic Securities Co.

“Investor appetite for private sector debt has hit rock bottom,” Lv said. “Many institutions are avoiding the private sector all the together. Investors should be very cautious toward those issuers that expanded debt aggressively.”

--With assistance from Emma Dong, Molly Dai and Carrie Hong.

To contact Bloomberg News staff for this story: Lianting Tu in Hong Kong at ltu4@bloomberg.net;Jun Luo in Shanghai at jluo6@bloomberg.net;Tongjian Dong in Shanghai at tdong28@bloomberg.net;Ina Zhou in Hong Kong at hzhou179@bloomberg.net;Yuling Yang in Beijing at yyang329@bloomberg.net

To contact the editors responsible for this story: Neha D'silva at ndsilva1@bloomberg.net, Michael Patterson, Sarah Wells

©2019 Bloomberg L.P.

With assistance from Bloomberg