History Shows Fed Pause May Require More Than an SOS From Stocks

U.S stocks sell-off stirred memories of past market turbulence as investors begin questioning viability of Fed’s tightening path.

(Bloomberg) -- The U.S. stocks sell-off has stirred memories of past market turbulence as investors begin to question the viability of the Federal Reserve’s tightening path. While it’s come to the market’s rescue in the past, it hasn’t done so recently without a distress signal from the economy.

A well-telegraphed increase this December is seen as a near certainty and U.S. economic growth remains above trend, but doubts are building over the three quarter-point rate hikes that central bank officials had projected for 2019 in September. With stocks now down more than 10 percent from their intraday peak that month, the prospect of a ‘Powell Put’ is gaining traction, amid slowing global growth and subdued inflation. In recent weeks, widening credit-market spreads and a freefall in oil prices have added to investor anxiety. Complicating matters is President Donald Trump’s criticism of the Fed and its Chairman Jerome Powell for continuing to raise interest rates as equities slide.

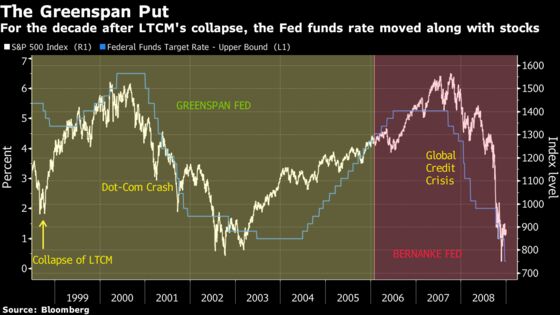

The tenure of former Fed chief Alan Greenspan is emblazoned in traders’ memories as the era of the ‘Greenspan Put’. Following the collapse of hedge fund Long-Term Capital Management in September 1998, and against a backdrop of emerging-market crises, Greenspan’s interventions to cut interest rates were closely correlated to stock market swoons, and markets had only to guess the level.

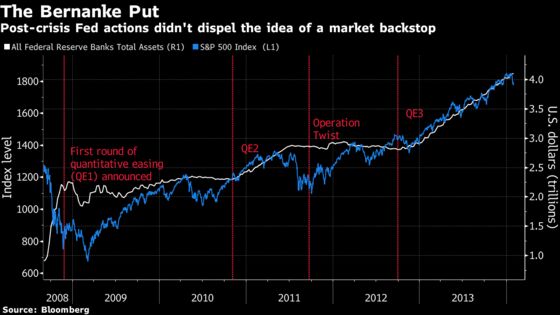

The lessons of the dot-com crash in 2000 and the global financial crisis in 2008 have exposed the risks of keeping rates too low for too long. But investors have continued to look toward the Fed for support. Ben S. Bernanke, Greenspan’s successor, slashed rates in the U.S. downturn of 2007 and 2008, and after running out of ammunition with rates near zero, he turned to the central bank’s balance sheet as his dominant tool for responding to threats.

That said, Bernanke and subsequently Janet Yellen did not act on every major market downturn. And that has given observers some pause for thought about how the Fed might respond to the latest ructions in global markets.

Looking at significant stock-market declines since 1994, Goldman Sachs economists led by Jan Hatzius concluded that the Fed is unlikely to pause this time around, and reiterated their forecast for four rate hikes in 2019. That’s a more aggressive call than the Fed’s median projection for three, and is unchanged even after comments by Powell and other Fed officials that have tempered money-market expectations for hikes.

“We find that the Fed responds with more accommodative policy only when other financial conditions such as credit spreads also deteriorate substantially or when growth is below potential,” Goldman economists wrote. “Today, in contrast, credit spreads have widened only moderately, and growth remains significantly above potential, with limited recession risk over the next year.”

Next month’s Federal Open Market Committee statement, which will be accompanied by new rate projections, will likely provide more clarity on how officials are thinking about the latest turmoil. In the meantime, episodes from recent years may provide a guide:

Debt-Ceiling Standoff: July 2011

- Market impact: S&P 500 shed more than 16% in just over two weeks and benchmark Treasury yields fell

- Fed response: Operation Twist

The economy and markets pushed the Fed to act, as a standoff over raising the debt ceiling between the new Republican house majority and the Democratic administration sparked fears of a U.S. default. The growth backdrop was shaky, with the U.S. still in recovery mode and the European sovereign debt crisis weighing on the global outlook. Bernanke warned of a “financial calamity” that could dwarf the Lehman Brothers collapse, and in early July he raised the potential for a third round of quantitative easing. President Barack Obama signed a plan to raise the federal debt limit on Aug. 2, and the Fed on Sept. 21 announced that it would reinvest maturing bonds into longer-dated debt, a plan known as Operation Twist. Even then, stocks took another leg down before finding a floor in early October.

Taper Tantrum: May 2013

- Market impact: Global market volatility, a spike in Treasury yields and a fall of about 7 percent in MSCI World Index of stocks

- Fed response: Communication

The standoff in May 2013 is often invoked as a template for market pushback against the Fed. In what became known as a “taper tantrum”, markets balked at the Fed’s first hint at withdrawing crisis-era accommodation by foreshadowing an end to QE asset purchases. The episode drove up volatility globally and spurred a spike in Treasury yields to over 3 percent, although the S&P 500 Index dropped no more than 6 percent in the month after Bernanke’s May 22 comments to Congress that tapering could begin in the “next few meetings.” The markets were soothed somewhat as the Fed subsequently emphasized that policy is not predetermined and that the FOMC expected “a considerable interval of time to pass” between ceasing bond purchases and lifting rates. The Fed did not step in with any additional stimulus measures, but it did carry on purchasing bonds at the same pace until January 2014 and stopped in October 2014. It didn’t implement its first rate increase until December 2015.

Slow-Motion Lift-Off: 2015 and 2016

- Market impact: Global market volatility, the S&P fell more than 10 percent in the opening weeks of 2016 and the Hang Seng plunged more than 16 percent

- Fed response: Lift-off delayed, projections dialed back

Market turbulence -- this time outside the U.S. -- did sway the Fed’s plans around its crucial first post-crisis rate hike. In early 2015, angst over China’s growth and the spillover to global markets thwarted the Fed’s tentative signals for a “lift-off” in the U.S. summer and again in September. Fed Chair Janet Yellen opted to delay the first rate hike until December 2015. Credit spreads widened into the year end and in January 2016, the S&P 500 fell alongside a rout in Asian markets. Pundits debated whether the Fed’s tightening cycle amounted to “one and done,” and by mid-February markets were pricing a rate cut. At lift-off in December 2015, the Fed’s median projection was for four rate hikes in that first full year of tightening, but only one materialized, at the end of 2016.

--With assistance from Benjamin Purvis and Alister Bull.

To contact the reporters on this story: Emily Barrett in New York at ebarrett25@bloomberg.net;John Authers in New York at jauthers@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Jenny Paris

©2018 Bloomberg L.P.