High-Rolling ‘Fujian Gang’ Caught in China Property Crisis

High-Rolling Real Estate ‘Gang’ Gets Caught in China Debt Crisis

(Bloomberg) -- “Work hard when young or enjoy no reputation later in life.” So goes a famous saying from China’s Fujian province.

Ou Zongrong stood by it, building a property empire with its roots in the province.

At first, things worked out well. Now the tide has turned.

In February, Ou’s Zhenro Properties Group Ltd. spooked investors by saying it may not have cash to redeem a perpetual note, just weeks after promising it would. In fact, it said it may not have enough liquidity to repay other near-term maturities.

That was a shock for investors in a developer that had been weathering China’s massive real estate crisis relatively well, never missing a public debt payment until then.

Zhenro’s stock slumped on the announcement, taking its drop for the year to 77%, while its dollar bonds plummeted to around 20 cents on the dollar from near par in January. Ou transferred about one-third of his stake in the company’s property-services unit to settle loans following a forced disposal of some Zhenro shares. Market watchers began questioning the firm’s transparency, eroding already-fragile confidence in the sector’s corporate governance.

The latest blow came on Wednesday, when Fitch Ratings Ltd. downgraded Zhenro to restricted default.

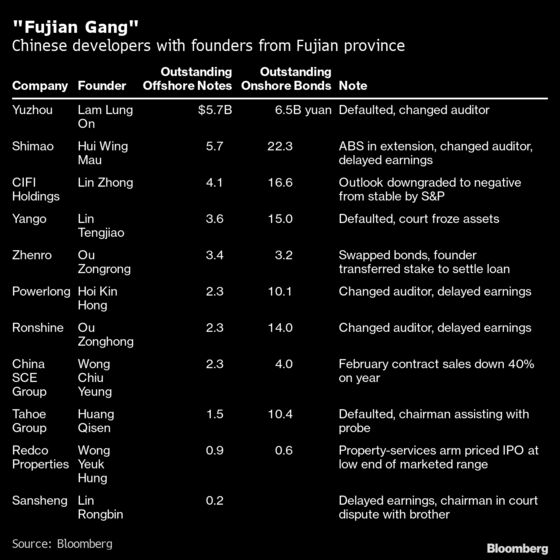

Zhenro’s fallout is a warning for investors in what is known as the “Fujian Gang”: publicly listed developers whose bosses came from the province and are famous for their risk-taking, even outbidding some of China’s biggest builders. As they did so, their debt ballooned, leaving them exposed when the government launched a nation-wide campaign to deleverage the sector that triggered a wave of failures.

The clan, which comprises at least 11 developers traded in Hong Kong and mainland China, includes some of the most troubled names. Yango Group Co. and Yuzhou Group Holdings Co. are responsible for at least $3.24 billion of defaults on dollar bonds this year -- more than half the sector’s total -- while many have asked investors for more time to repay their debt.

“Fujian-based developers such as Ronshine, Yuzhou, Zhenro have been aggressively funding land acquisitions with debts,” said Dan Wang, a credit analyst at Bloomberg Intelligence. “This has left them vulnerable in a property market downturn and in a scenario where capital markets shut down.”

China’s private housing market expanded rapidly after its liberalization in the 1990s, leading to a surge in prices for one of the few safe investments available to the nation’s emerging middle class. Developers in Fujian, a province originally famous for its apparel and manufacturing businesses, were relatively late to the property game and had to use leverage to catch up.

To help gain scale, many firms that originated in the province moved their headquarters to bigger cities, while their founders or top executives sought to gain political influence. Ou, who created Zhenro’s predecessor in 1998, transferred the company’s main offices to Shanghai in 2016 and is a delegate for one of China’s top advisory bodies, along with four bosses from the developers with Fujian roots.

While generally smaller than giants such as China Evergrande Group and Country Garden Holdings Co., aggressive land acquisitions allowed the Fujian companies to grow quickly. In 2016, Zhenro made headlines for buying a parcel in Wuhan at a peak price, outbidding some of the country’s top names including Sunac China Holdings Ltd. with premiums exceeding 400%. The same year, Ronshine China Holdings Ltd. -- founded by Ou’s younger brother -- set a national record by splashing 11 billion yuan ($1.73 billion) for a site in Shanghai, while Sansheng Holdings (Group) Co. in 2020 paid the most ever per square meter for a plot in the eastern city of Wuxi.

The strategy paid off: Revenue surged for the companies from the group, rising more than 10-fold at Zhenro and Ronshine in the six years through 2020. Now five of China’s top 30 developers have their roots in Fujian, from two in 2012.

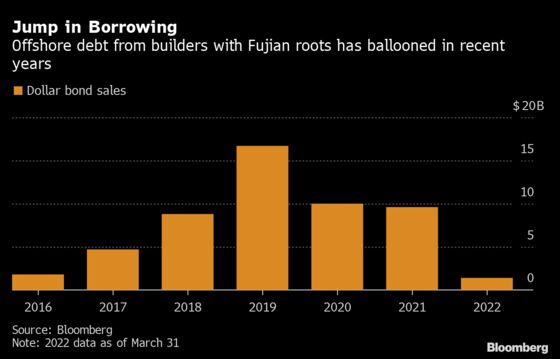

But the quick expansion led to a pile of debt, including a large pool of money borrowed from global investors. Annual dollar bond sales by developers with Fujian roots rose ninefold from 2016 to peak at $16.7 billion in 2019, representing more than one-quarter of all dollar debt sold by the sector that year. As of March 31, the group had $32 billion of dollar bonds outstanding.

None of the 11 builders responded to requests for comment.

While China has relaxed some of its rules to ease the burden on the real estate market, Country Garden’s results showed the gap is widening between the better funded developers and the others. For many, the outlook remains bleak as home sales are still falling and access to financing remains tight.

Adding to investors’ concerns, Shimao Group Holdings Ltd., Powerlong Real Estate Holdings Ltd. and Ronshine are among those that delayed the release of their 2021 financial results, citing reasons including auditor resignations and the impact of Covid-19. Ronshine, which until a few months ago was deemed one of the safest bets for being in compliance with the government’s three red-lines policy, was downgraded deep into junk in March by both Moody’s Corp. and Fitch. Meanwhile, Tahoe Group Co.’s chairman is being probed for an undisclosed offense.

“The liquidity strain of China’s property sector is set to cast a long shadow over the land market,” Bloomberg Intelligence analysts Kristy Hung and Lisa Zhou wrote in a note. “Debt troubles for private developers should sap their appetite to invest, as their near-term liquidity outlook fails to improve even after policymakers’ shift to a supportive tone.”

An additional problem is that the Fujian developers often joined forces to win big projects and share the debt burden. That means if one is in trouble, it can easily spread to the others. Zhenro has joint developments with builders including CIFI Holdings Group Co., Yango and Shimao, and the dollar bonds of the latter two trade near record lows.

“It’s common for the second-tier developers to team up to compete against the top ones,” said Kenny Ng, a strategist at Everbright Securities International in Hong Kong. But when the overall market sentiment cools, “it could trigger a chain effect.”

The slump has cost the Fujian bosses billions. Shimao’s Hui Wing Mau, Zhenro’s Ou and Lin Zhong of CIFI have all seen their fortunes slump. Ou is no longer a billionaire, according to the Bloomberg Billionaires Index.

Zhenro managed to buy itself some time with a debt swap to cover five of its notes. On Thursday, it pledged to accelerate asset sales after reporting its financial position weakened.

Still, Fujian builders face further obstacles as the crisis unfolds. Dollar bonds are trading at highly stressed levels even for developers that haven’t defaulted.

“We have been cautious on the bonds issued by Fujian developers, as they are typically more aggressive than peers,” said Zhijun Zhang, chairman of private fund manager Beijing DingNuo Investment Management Co. “Investors are expecting more bond defaults.”

©2022 Bloomberg L.P.

With assistance from Bloomberg