2019 Was Great for European Markets. Now for the Bad News

2019 Was Great for European Markets. Now for the Bad News

(Bloomberg) --

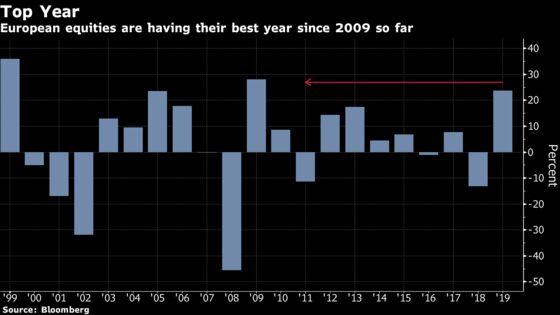

With the Stoxx 600 now trading at a record high after surging 24% since the start of the year, 2019 is on track to be the third-best year for European equities in two decades after strong runs in 1999 and 2009 -- 9 seems to be the lucky number. Now, what comes next is anyone’s guess, but looking at 2020 the market is set to face serious hurdles which could make it difficult to repeat this year’s rally.

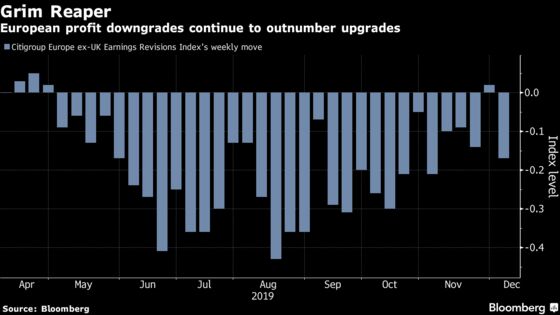

First, the earnings trend. Forecast downgrades have been a main feature of 2019, as bottom-up analysts relentlessly cut their their estimates. The negative trend is still going on, and most strategists say the 2020 consensus is still too high. Next year, companies in the Stoxx 600 are expected to see profit growth of 8.9%, compared to 9.3% for S&P 500 companies, according to data compiled by Bloomberg.

Earnings downgrades for Europe, excluding the U.K., have outnumbered upgrades since April. For UBS Global Wealth Management, tepid profit growth predictions support its preference for U.S. stocks over Europe.

“The U.S. profit cycle feels ‘long in the tooth’ but we still see a mix of better revenue growth, and higher and more sustainable margins than in the euro zone,” said Maximilian Kunkel, chief investment officer for Germany at UBS Global Wealth Management. “Greater volumes of share buybacks are likely going to mean that U.S. earnings growth is going to outperform euro-area earnings growth.”

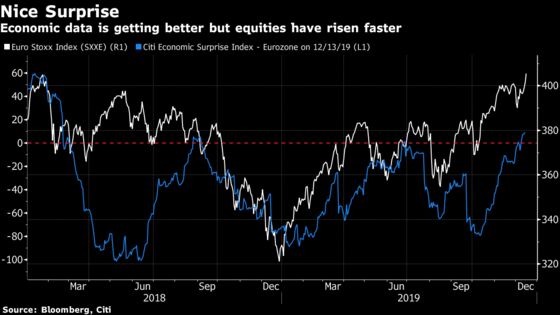

Economic growth remains a big question mark for Europe in 2020, with risks of a further slump in manufacturing. The challenging outlook was highlighted by the European Central Bank last week, which revised down its projection for expansion next year.

The latest batch of PMI data on Monday confirmed that economic woes aren’t behind us yet. IHS Markit said the bloc’s employment growth slowed to a five-year low and Composite PMI signaled fourth-quarter output will be the weakest since the region exited a double-dip recession in the second half of 2013. In France, service-sector resilience largely countered an unexpectedly sharp drop in manufacturing momentum, while Germany’s industrial slump deepened. That said, overall economic surprises have been on the rise and turned positive in December, but further improvement might be needed.

A Conservative government and the Brexit deal it will pursue is “no silver bullet,” said James Dowey, a fund manager on the global equity team at Liontrust Asset Management. The departure from the EU will “very likely incur significant long-term economic costs” and the real problem for the U.K.’s economy and its companies is still low productivity, which Brexit is more likely to hinder than help.

And while the risk of a no-deal exit is small, “2020 is likely to remain a complicated year of negotiations and roller-coaster headlines” which will keep Brexit-sensitive assets in the U.K. and Europe volatile, said Esty Dwek, head of global market strategy at Natixis IM Solutions.

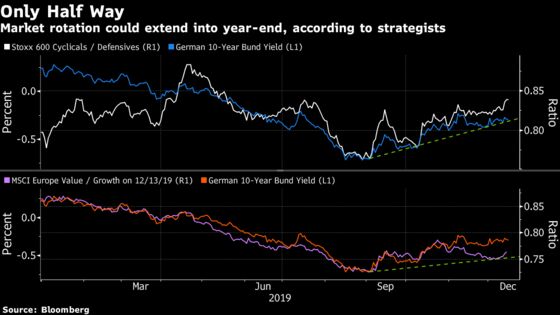

Finally, portfolio managers will be worried about bond yields. Firstly, the U.S. yield curve has been a good indicator of incoming recessions in the past. Second, market leadership is driven by bond yields and the recent inflection of the 10-year German bund yield should drive value and cyclical shares higher.

To contact the reporters on this story: Michael Msika in London at mmsika4@bloomberg.net;Ksenia Galouchko in London at kgalouchko1@bloomberg.net;Sam Unsted in London at sunsted@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, Jon Menon

©2019 Bloomberg L.P.