Why Hedge Funds Will Stick With Ever-Risky Short Volatility Trades

Why Hedge Funds Will Stick With Ever-Risky Short Volatility Trades

(Bloomberg) -- It’s a familiar spectacle on Wall Street: the short-volatility complex takes a beating -- and prophets of doom warn money managers the strategy is running out of steam.

But the trade isn’t going to be pounded into submission, even as late-cycle bears sharpen their claws and assets in passive products that bet against equity-price swings shrink to their smallest since 2013.

Market and technical forces practically guarantee hedge funds will keep calm and carry on -- setting the stage for the next wash-out, say volatility speculators.

“There are monetary conditions still supporting the trade,” said Yannis Couletsis, director at volatility hedge fund Credence Capital Management Ltd. “As long as central banks take a gradual and incremental pace of deleveraging, and their rhetoric continues to actually function as a volatility absorber, the short-vol carry will still make money.”

The VIX experienced its most violent shudder since February on Oct. 11, on the heels of a two-day 5 percent rout in the S&P 500 Index. That left short-sellers holding the bag, as the price of near-term futures surged above those further out on the curve.

Lincoln Edwards of Houndstooth Capital Management LLC, a $9 million hedge fund in Austin, Texas, that reaped 6,000 percent in February’s meltdown, estimates the losses on some of those short futures positions to be around $420 million.

But, in relative terms, the pain is limited.

The breakout in the VIX this month is less extreme than the February tumult and fewer funds are “leveraged to the hilt,” suggesting short-sellers are “sitting tight,” according to Tobias Hekster, co-chief investment officer at hedge fund True Partner Capital. “Their choking levels simply were not reached.”

After surging to as high as 29 last week, the volatility gauge closed around 20 on Monday.

The take-away? It’s likely "business-as-usual for the short-vol trade -- and thus setting us up for the next hiccup somewhere down the road,” Hekster said.

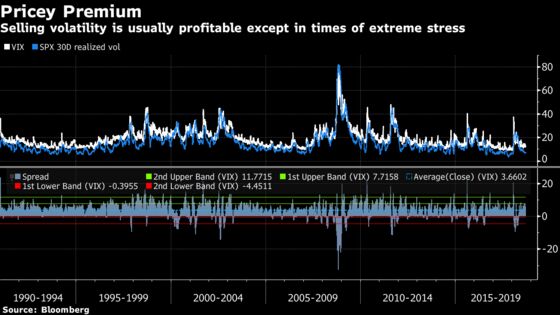

Pretty Premium

The classic version of the strategy depends on the shape of the futures curve, and the tendency of implied volatility to be more elevated than its realized counterpart -- a dynamic some say is exacerbated by the tide of central-bank liquidity.

Sellers of volatility expose themselves to the prospect of unlimited losses in tail scenarios, while the pain for option buyers is limited to the premium paid. That asymmetry keeps the difference between future expectations of volatility and what actually comes to pass at a persistent spread, all but guaranteeing short-sellers make money -- except when the VIX suddenly surges as per moves seen last week.

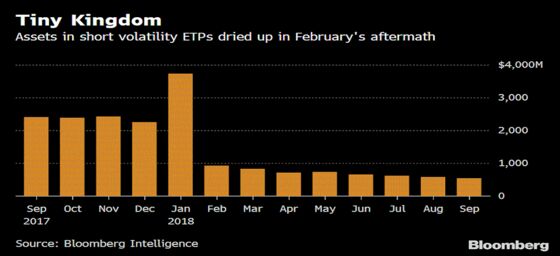

One key reason for the likely lack of lasting pain is the absence of the short-volatility exchange-traded products said to have exacerbated the hurt earlier this year.

According to the now-famous theory, volatility-related ETPs scrambling to rebalance their holdings snapped up VIX futures in the grip of February’s meltdown, effectively pushing up the price of the contracts -- and eventually the underlying index.

“The AUM of these products is a ghost of what it once was,” said Houndstooth’s Edwards. “That’s actually a really good thing for short-volatility speculators since they’re less likely to get squeezed like they did on February 5th.”

More to the point, data suggests short-sellers were sticking to their guns despite ominous signs like the inversion of the VIX futures curve. Speculators were net short some 113,000 VIX futures contracts on Oct. 9, four days after the curve inverted, CFTC data show.

“Given the degree to which volatilities were depressed going into this, there is no doubt in my mind that the volatility short trade was alive and kicking,” said Hekster.

These investors have developed nerves of steel in recent years, thanks to the frequency of outsized VIX spikes.

“Sudden bursts of volatility have become a more frequent phenomenon in the past few years,” Pravit Chintawongvanich, equity derivatives strategist at Wells Fargo Securities, wrote in a note. He points out that since 2007, there have been six such events, compared with five in the preceding 50 years.

Such bursts can be lethal for the short-volatility punt, unless traders have had the foresight to implement hedges. In a twist that further feeds the volatility complex: Large VIX moves create yet-another opportunity to short the index on the way down.

Regardless, it is the investing strategy’s bread-and-butter -- the tendency of longer-dated futures to be more expensive than shorter-dated contracts -- that will feed hedge funds and retail investors anew.

“Although large VIX spikes create the best opportunity to short volatility, I still believe that over 70 percent of the short-vol income comes from the futures curve roll-down,” said Couletsis.

--With assistance from Luke Kawa.

To contact the reporter on this story: Yakob Peterseil in London at ypeterseil@bloomberg.net

To contact the editors responsible for this story: Samuel Potter at spotter33@bloomberg.net, Sid Verma, Brendan Walsh

©2018 Bloomberg L.P.