Hedge Funds Ramped Up Leverage in Stocks Just Before Market Rout

Hedge Funds Ramped Up Leverage in Stocks Just Before Market Rout

(Bloomberg) -- Individual investors weren’t the only ones falling in love with stocks right before they went south. Turns out the savviest of institutions were in equally high spirits.

Hedge funds, which use borrowed money to amplify returns, went risk-on in a major way this month. Net leverage, a measure of industry risk appetite that takes into account long versus short positions, rose by about 5 percentage points, one of the fastest expansions in years, according to data compiled by Morgan Stanley’s prime brokerage unit.

While positioning like that could still pay off, it adds to a sense that traders got way too confident at a time when the coronavirus threat was showing no sign of subsiding. Bullish investors have been stung over the last four days as stocks posted the biggest drop since 2015.

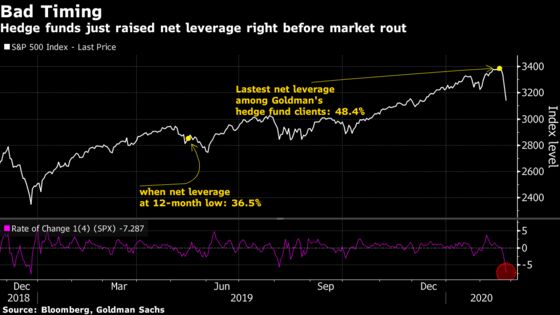

At Goldman Sachs Group Inc., clients have also ramped up their leverage after holding it steady since late 2019. At 48.4% on Thursday, the ratio stood at the 95th percentile over the past year, the firm’s data showed.

The burst of optimism is a departure from much of 2019, when hedge fund stock pickers resisted the the rally. It adds to growing evidence that almost everyone was bullish just before the bottom fell out. Prior to last week, small investors were rushing into winners like Tesla Inc. and loading up call options. Money managers in a Bank of America Corp. survey boosted equity holdings while slashing cash levels to a seven-year low.

Throw that into a market where valuations are the highest since the dot-com bubble, and it’s a recipe for trouble. Down almost 8% over four sessions through Tuesday, the S&P 500 erased a monthly gain that at one point was poised to be the best February in 20 years.

“Any perception of liquidity that the market tends to give you disappears pretty quickly,” Tom Plumb, president of Plumb Funds, said in an interview at Bloomberg’s New York headquarters. “Even these very smart investors can get caught up into the current waves of sentiment.”

Morgan Stanley’s hedge fund clients bought the dip Monday, with purchases spreading across sectors. Technology, whose global sales and supply chain are jeopardized by the spread of the coronavirus, saw the highest demand.

Despite the sudden turmoil spurred by coronavirus concerns, however, there are signs that hedge funds can withstand pain. Their picks aren’t faring significantly worse than the broader market. A Goldman basket tracking the industry’s most-popular shares fell 8.4% during the rout, just a tad more than the Russell 1000.

Break down the index by hedge fund ownership and the pattern holds. On Monday, when the benchmark dropped 3.3%, stocks in the top quantile of hedge fund ownership lagged behind the bottom group by only 0.41 percentage points, data compiled by Bloomberg showed. For perspective, during the October 2018 rout, the group’s most favored stocks fell twice as much as the least favored.

That, along with gains from bets against stocks in a down market, limits career risk for managers, lately a top concern in an industry whose performance is under growing scrutiny. Longer-term, their favorite stocks are beating the market. Goldman’s basket of hedge fund VIP stocks is up almost 1% this year, compared with a 3% loss for the S&P 500.

“A paper cut on your finger is not fun,” said J.C. O’Hara, chief market technician at MKM Partners LLC. But “for managers to get shaken out of their positions, they need to lose a finger,” he said.

Still, it doesn’t mean all is well.

One lurking risk, according to Morgan Stanley, is a potential reversal in so-called crowded stocks. Over the past two years, hedge funds have stuck to a troublingly similar script, favoring dividend shares and companies whose sales are seen as resilient amid a slowing economy. They’ve mostly avoided those priced at lower valuations relative to earnings and book value, many of which -- such as energy companies -- are sensitive to economic swings.

In the thinking of Morgan Stanley, when everyone is gravitating toward the same kind of stocks, the danger of a reversal grows.

The firm’s combined risk metric, which tracks leverage, industry and style preferences, and crowdedness, just peaked and started rolling over. During the past few years, such a pattern has tended to foreshadow a rotation from the most-crowded longs to the most-crowded shorts by a lag of between two to three months, Morgan Stanley found.

Last week, the firm’s hedge fund clients sold growth stocks while adding to value and cyclical shares. The selling of momentum on Thursday was the biggest since last September. At Goldman, a retreat from growth companies continued among its clients.

“It remains unknown if this the start of a larger reversal,” Morgan Stanley wrote in the note to clients last week. “A rotation might not be imminent, but positioning is now arguably back to some of the most stretched we’ve seen

To contact the reporters on this story: Lu Wang in New York at lwang8@bloomberg.net;Melissa Karsh in New York at mkarsh@bloomberg.net

To contact the editors responsible for this story: Brad Olesen at bolesen3@bloomberg.net, Chris Nagi, Richard Richtmyer

©2020 Bloomberg L.P.