Hedge Funds Debunk ‘Indexers Killed My Rally’ Theory of Sell-Off

Hedge Funds Debunk ‘Indexers Killed My Rally’ Theory of Sell-Off

(Bloomberg) -- It’s getting harder and harder to lay the blame for last month’s market rout squarely on passive investors.

Index trackers were in the firing line after some technology-focused exchange-traded funds were forced to ditch billions of dollars of Facebook Inc. and Alphabet Inc. in late September. Some speculated that the sales fed a broader stock-market correction that began a few days later.

But as regulatory documents disclosing trades by active managers trickle out, it’s clear passive investors made up a relatively small contingent of sellers. Hedge funds were net sellers of both companies last quarter, data compiled by Bloomberg show, with the likes of Appaloosa Management and Viking Global Investors cutting stakes. While the filings don’t pinpoint the timing of these trades, they indicate a broader souring of sentiment around the two firms.

“When you start thinking about more active money out there today, it’s still effectively at least double” ETFs, said Joe Smith, deputy chief investment officer at Omaha, Nebraska-based CLS Investments, which manages $9 billion. “There’s a lot of names that have been bid up. Now that we’re going through the earnings seasons and also some of these changes that have occurred, people are finally starting to look under the hood.”

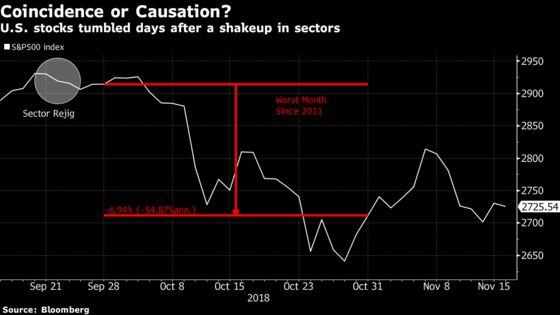

Facebook has a $414 billion market capitalization; Alphabet is worth $743 billion. They’re both giants next to ETFs with about $40 billion of assets that have been implicated in the worst month since 2011 for U.S. stocks.

What Happened

It’s all part of the greater scrutiny that passive investing is attracting as it conquers a larger and larger region of the market. That growth has spurred legitimate concerns about how indexing affects volatility, liquidity and valuation -- as well as the growing influence of the companies that create and maintain these benchmarks.

In this instance, S&P Global Inc. and MSCI Inc. -- two of the largest index providers -- decreed last year that Facebook and Alphabet should no longer be considered technology companies. The duo were spun out of some tech-focused benchmarks and into a new communications services sector, alongside Netflix Inc., which moved from the consumer discretionary category, and a bunch of old-school telecom stocks. Two large tech ETFs run by State Street Corp. and Vanguard Group had to sell their stakes as a result.

“The stocks that were sold were also very volatile, which means if there wasn’t a concurrent buy as part of the rebalance, then they would probably move a lot more than average,” said Oliver Brennan, a London-based macro strategist at TS Lombard, who wrote a note arguing that sector rebalancing helped stocks roll over. “I’m not trying to suggest the trigger and the sole cause for the selloff was the rebalance, but it happened at the exact worst time.”

‘Everyone Knew’

The change took effect in September. TS Lombard estimates sector ETFs sold around $10 billion of Facebook, Alphabet and other stocks, like Twitter Inc., that moved out of tech. Those companies should have been picked up by communications services ETFs but investors were slow to move their money to reflect the new weightings, Brennan wrote in a Nov. 4 note.

That’s certainly true: communications ETFs house just $5.5 billion, with Vanguard and State Street’s products investing 30 to 40 percent in Facebook and Alphabet.

But Vanguard’s $20 billion tech-focused VGT didn’t have much left to sell in September. It adopted interim indexes and gradually sold out of the two companies. By the end of August, the ETF had just 1.3 percent in Facebook and 2.4 percent in Alphabet, worth about $840 million, data compiled by Bloomberg show. State Street’s $19.5 billion XLK had about $3.6 billion of exposure at the reclassification in September, the data show.

“Everyone knew this was on the move for almost nine months leading up to it so it’s hard to see why this would be the catalyst in this discrete period of time,” said Rich Powers, head of ETF product management at Vanguard. “The sector funds are relatively small in assets relative to the total market cap of the industry, and the trading that happens among active funds.”

Active Approach

Hedge funds turned underweight on technology, communications and internet retail companies for the first time since at least 2010, RBC Capital Markets wrote in a note on Friday.

Meanwhile, active manager Wellington Management Group reduced its position in Facebook by 13 million shares in the third quarter, while T Rowe Price Group Inc. axed 10 million shares -- both more than XLK sold. AllianceBernstein and JPMorgan Chase & Co. unloaded some Facebook and Alphabet shares in the three-month period ending Sept. 30.

That’s not to say the sector switch had no impact at all. Some active managers look to keep positions within 5 or 10 percent of certain benchmarks and may have adjusted their holdings to reflect the new categories, while others could have used the reclassification as a pivot point to rethink their allocations.

Entering October, valuations of technology stocks were pretty stretched -- the Nasdaq 100 Index’s price-to-earnings ratio was about 25 percent higher than the S&P 500’s. The companies had also been at the forefront of a rally in growth and momentum stocks, making them ripe for a large correction, particularly as hawkish statements from the Federal Reserve sent bond yields soaring.

“When some of these big moves happen, people thirst for a rational and logical explanation, and indexes and ETFs often fit that bill very nicely,” said Lance Humphrey, a money manager in the global multi-assets team at USAA Asset Management. “Indexes and ETFs are very easy punching bags.”

--With assistance from Lu Wang.

To contact the reporter on this story: Rachel Evans in New York at revans43@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Chris Nagi, Eric J. Weiner

©2018 Bloomberg L.P.