Hedge Funds Chasing 400% Return Show Risk in China's Wild Market

Hedge Funds Chasing 400% Return Show Risk in China's Wild Market

(Bloomberg) -- As China’s share market was cratering at the end of 2018, Liu Yue bet almost his entire fund on just two stocks. It could have ended in tears, but he knew his firm had a once-in-a-lifetime opportunity to snare the ultimate prize for a hedge fund in China -- being crowned champion of the year.

His bet paid off and Guangdong Chaokin Investment Co. has since been swamped with investor inquiries. Many of his peers haven’t been as lucky.

In a market where hedge funds number close to 9,000, there’s increasingly only one good way to stand out: produce stunning returns. But there’s a problem with this approach -- one-way bets on stocks can go sour just as quickly as share prices soar. It’s led to a dramatic and abrupt end for some of China’s most-feted hedge-fund managers.

“The ‘curse of the champion’ does exist,” said Liu Youhua, an analyst at Shenzhen PaiPaiWang Investment & Management Co., referring to the accelerating phenomenon of top-performing funds ending up on the scrap heap. “And it’s set to continue.”

Rising Trend Capital Management is one of the latest casualties. The Shenzhen-based hedge fund run by Huang Ping shot to fame in 2013 with a 120% return, before capping that with an even better 301% gain in 2014 (making it the only Chinese hedge fund to cinch the championship title twice). Its fortunes turned in 2016 after it bet on Dandong Xintai Electric Co. just as the power-transmission-equipment maker was near delisting.

License Revoked

Rising Trend recorded losses of around 200 million yuan ($29 million) on Xintai Electric that year alone and Huang, in an unrelated matter, was fined 62 million yuan for manipulating six stocks in 2015 via 37 different accounts. The hedge fund had its license revoked permanently in May.

Amid this year’s stock-market rally, sky-high returns are back. A total of 56 hedge funds tracked by PaiPaiWang more than doubled returns in the first half, with a little-known manager called Grapefruit Investment boasting the highest gain, at 391%.

It’s hard to repeat industry-beating performance anywhere in the world but Chinese hedge funds, especially smaller ones, face more incentives than most to “go out on a limb,” said Yan Hong, head of the China Hedge Fund Research Center in Shanghai. A base of mostly retail investors, many of whom are chasing returns without paying much attention to risk, only fuels that desire to stand out, he said.

Regulators are starting to take notice.

The Asset Management Association of China, the body responsible for hedge-fund registrations, has this year canceled the registration status of more than 300 private-fund-management firms on the grounds they’ve become “out of touch” or that they’ve failed to submit required legal opinions after experiencing “abnormal operating conditions.”

The China Securities Regulatory Commission, as the nation’s stock-market regulator, has also been taking more of an interest. Of the 453 private funds it inspected in 2018, almost one-third were found to have violations ranging from illegal fundraising to misuse of investors’ money. That’s the highest percentage in at least three years, according to Bloomberg calculations based on CSRC data.

The desire to shine isn’t so surprising considering the nature of China’s hedge-fund market.

The sector is beset by smaller players, often run by self-taught operators. Funds’ assets under management average just 264 million yuan, according to AMAC data, however more than half run strategies with less than 100 million yuan, the minimum needed to sustain operations unless performance fees are high, Yan said.

Capital is also readily available. Rising Trend, for example, raised 240 million yuan in 10 minutes in November 2014, completing a product sale that was originally scheduled for three days in just one, according to local media reports.

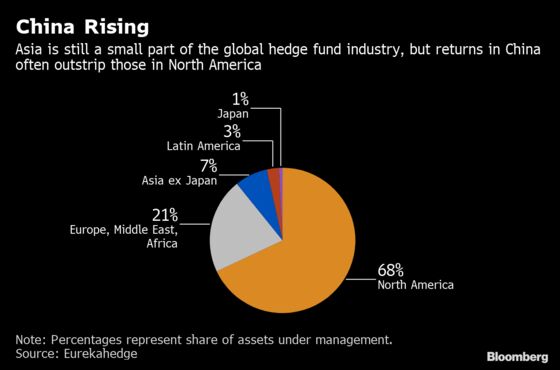

Top performers in China have also routinely generated much higher returns than their global peers, beating them every year in the five years through 2018 by an average 156 percentage points, Bloomberg calculations based on data from Preqin Ltd. and PaiPaiWang that exclude funds investing in cryptocurrencies show.

But those gains can be short-lived: Of the top 20% of hedge funds in annual rankings for the three years from 2014 through 2016, more than half ended up among the bottom 40% the following year. (Rankings have been relatively more stable in 2017 and 2018 because the market has stayed largely bearish.)

“In pursuing very high returns, the risk inevitably goes very high as well,” rendering performance unstable, PaiPaiWang’s Liu said.

Pig Feed, Mineral Water

Chaokin’s Liu, who is head of investment at the firm, agrees his idea to put around 80% of his flagship fund into New Hope Liuhe Co., a company that makes pig feed, and Shanghai Maling Aquarius Co., which produces bottled water and frozen food, was a gamble.

His investment committee initially rejected the idea as too high risk. Since the beginning of the year, the company, based in the southern city of Guangzhou, had been sticking to its trusted strategy of focusing on industry bellwethers like soybean sauce maker Foshan Haitian Flavouring & Food Co. amid an economic slowdown.

But then unexpected rallies in some of those bellwether stocks pushed up returns for the fund, and by November, Liu sensed the 2018 hedge-fund champion title was in reach.

The 152% gain and No. 1 ranking brought many inquiries from potential investors, including one new client who traveled 1,200 kilometers from Shanghai to put in 10 million yuan, helping to boost assets under management by about 20%. Chaokin now manages just under 1 billion yuan, much of it from local businesses.

“Both the market and the prices of those stocks were low, otherwise we wouldn’t have dared,” Liu said. “There was a lot of luck there.”

To contact Bloomberg News staff for this story: Zhang Dingmin in Beijing at dzhang14@bloomberg.net

To contact the editors responsible for this story: Katrina Nicholas at knicholas2@bloomberg.net, Peter Vercoe

©2019 Bloomberg L.P.

With assistance from Bloomberg