Hedge Funds Build War Chests to Target Dislocated Debt in Europe

Hedge Funds Build War Chests to Target Dislocated Debt in Europe

(Bloomberg) -- The damage wrought by the coronavirus pandemic has funds across Europe smelling blood.

Investors who profit off others’ woes are raising cash like never before, anticipating that desperation will lead to opportunity from Manchester to Milan. About a dozen funds are in race to gather more than $11 billion, which would more than double the unspent capital available in European distressed debt money pools, according to data compiled by Preqin.

Even with taxpayers and central bankers in the U.K. and euro zone putting up trillions of euros to prevent a collapse, funds like Chenavari Investment Managers and Cheyne Capital Management reckon the worst economy since the Great Depression will still leave plenty of low-hanging fruit. Airlines, hotels, restaurants, and retailers are among those whose business model has been rocked.

“A multi-year distressed cycle awaits us,” said Anthony Robertson, chief investment officer for distressed debt at London-based Cheyne. “As the dust settles and the harsh reality of Covid reveals itself throughout the corporate world, we’ll see a very sustained period of significant economic weakness.”

For distressed debt funds, the moment marks a turnaround from an era when near-zero interest rates and steady - if unspectacular -- growth after the financial crisis a decade ago kept too many sickly companies on life support.

An index of distressed and restructuring funds has risen just 2% the past five years as compared to 7.7% return in a broader hedge fund index. The Standard & Poor’s 500 returned almost 55% in the period.

Even as the pandemic struck, specialists were struggling. Distressed funds lost 11% in March.

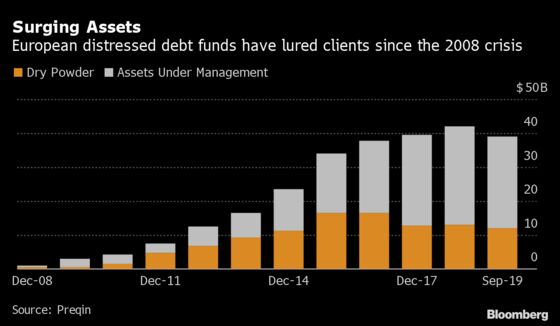

The cash that Europe-focused distressed-asset funds are seeking would add to the $12.1 billion available as of September -- so-called dry powder -- and total assets under management of $27 billion, according to data compiled by Preqin. That mirrors the U.S., where such funds had $69.1 billion of undeployed capital and $146.4 billion in assets. They’re looking to raise $68 billion more now.

Largest Europe-Focused Distressed Debt Funds in Market

| Fund Manager | Target Size (Million) |

|---|---|

| LCM Partners | EUR 4,000 |

| Fortress Investment Group | USD 3,000 |

| AGG Capital Management | EUR 2,000 |

| Alcentra | EUR 1,000 |

| Chenavari Investment Managers | EUR 1,000 |

| Source: Preqin, Bloomberg reporting | |

There are more investment targets because corporate Europe is more leveraged than ever, and an increased amount of the borrowings can no longer be paid back. The amount of debt classified as distressed in Europe has surged to more than 13 billion euros from only 2 billion euros at the start of 2020, according to Bloomberg Barclays index data.

Borrowers that have thrown in the towel recently include U.K. fashion retailers Laura Ashley, Oasis and Warehouse, and German restaurant chain Vapiano SE.

Still, there will be some hurdles to surmount. The European Central Bank and Federal Reserve are propping up bond markets, indirectly aiding borrowers that may otherwise collapse.

Governments across the world are offering loans and other support programs to prevent performing companies from going under. French shipping firm CMA CGM and Spanish ferry operator Grupo Armas-Transmediterranea are among borrowers to have received state-backed loans in recent weeks.

This means that there may not be as many distressed opportunities as expected and those that do arise are likely to be crowded and less lucrative.

“There is no doubt that a new distressed cycle is coming,” said Nicolas Roth, head of alternative assets at Geneva-based private bank Reyl & Cie. “However, with the world in a global synchronized recession, this cycle will certainly be very different from the previous one. The opportunities today are mostly in dislocated liquid markets such as CLO and MBS for now.”

Ruined Analogy

Warren Buffett has warned investors that this crisis is different to 2008 when there were “intelligent things to do” and not much competition. This time around, companies that would have relied on help from Buffett’s Berkshire Hathaway Inc. are accessing public markets instead.

For Andrew Beer, founder of New York-based Dynamic Beta investments, the Fed has ruined Buffett’s famous analogy that “when it’s raining gold, reach for a bucket, not a thimble.”

“Hedge funds were readying the proverbial buckets and getting ready to run outside but no-one expected the Fed to act with such speed and size,” Beer said. “Unlimited intervention basically meant the Fed has already swept up a swimming-pool size bucket of bars of gold.”

But corporate distress comes in different shapes and sizes and some investors argue there is plenty to go around.

The cash coming into struggling company debt will go down different avenues such as corporate, shipping, real estate and non-performing loans, according to Duncan Priston, the London-based co-head of European distressed credit at HIG Bayside Capital.

His firm invests in small to medium sized enterprises and typically puts smaller amounts of capital to work than larger investment houses like Oaktree Capital Group LLC which is raising $15 billion for the biggest distressed debt fund on record.

“Whilst there has been a dramatic increase in investor interest in distressed, it’s not not all chasing after the same targets,” said Priston.

©2020 Bloomberg L.P.