Hedge Funds See More Juice in Carbon Market's Two-Year Rally

Hedge Funds See More Juice in Carbon Market's Two-Year Rally

(Bloomberg) -- The speculative fervor that made European carbon allowances the hottest commodity of 2018 shows little sign of abating with more hedge funds seen doubling down on expectations for higher prices.

Some 15 to 20 funds have begun or are considering multi-month or multi-year bets in Europe’s market for emission rights, according to Louis Redshaw, the former head of emissions at Barclays Plc who now advises investors including funds on the market. Buyers as far afield as the U.S. and India are getting into carbon.

Carbon futures, which reflect the price factories and utilities pay for their emissions, soared as the European Union implemented reforms aimed at reducing a supply glut, mainly by cutting the amount of permits auctioned. That drew investors including Lansdowne Partners U.K. LLP and Northlander Commodity Advisors LLP, the commodity hedge fund run by Ulf Ek.

Carbon market participants this year are expecting further gains this year, albeit not as strong as in 2018.

“There’s a lot of speculative buying going on,” said Bostjan Kovacevic, a trader at carbon brokerage Belektron who has noticed more outsiders and fewer emitters in the market at the moment.

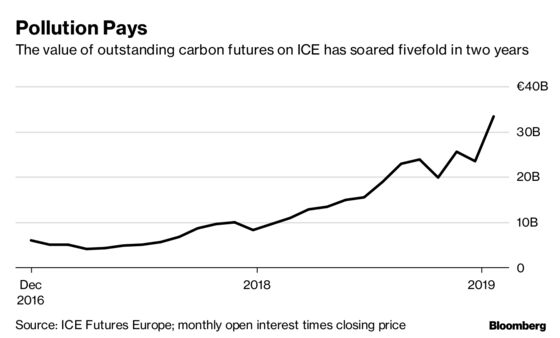

The value of outstanding carbon contracts has swelled to more than 30 billion euros ($34 billion) on ICE Futures Europe, a five-fold jump in two years. After climbing to a decade-high 25.79 euros a ton in September, carbon futures may surge to near 29 euros a ton or more this year, according to a Bloomberg survey last month. Prices are little changed so far in 2019.

Carbon’s gain helped Lansdowne’s Energy Dynamics fund return 6 percent net of fees last year as the MSCI World Energy Sector Index fell 18 percent. Northlander benefited from a bet in the carbon markets, returning 53 percent in 2018 net of fees, according to a note to investors seen by Bloomberg.

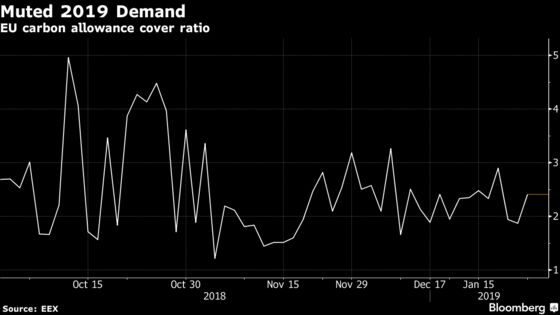

“There is multiple times upside still,” Per Lekander, a fund manager at Lansdowne. He correctly called the market’s rally that started in 2017 as well as its decline in 2011. Now, he's watching key market metrics gauging how demand in the near-daily auctions for allowances.

“I am watching the cover ratio very closely. It needs to jump for the bullish scenario to materialize, and I think it will,” he said. “If it has not materialized in four weeks, I think the recovery to fundamental value -- which I put well north of 50 euros a ton -- will be more gradual over a few years.”

After years of being a niche commodity, the emissions market’s growing liquidity is helping draw more participants such as hedge funds, many of whom had a difficult 2018, the industry’s worst in seven years. The wager is that the European regulator’s overhaul of its market will yield even more gains after spurring prices to triple last year. The risk is whether that intervention has already been factored into market rates.

“Some hedge funds might be licking their wounds a bit” and may remove money from the carbon market, said Redshaw, founder of Redshaw Advisors Ltd. Even so, he’s not expecting a “mass exodus.”

There’s still a lengthy list of hazards to carbon’s continued rally.

Many have already taken profits. Even though the value of outstanding futures has jumped on ICE, the actual open interest figure is lower than this time last year.

The outlook is also muddied by the impact of Brexit as well as Germany’s plans to exit coal-fired power, which could stifle demand for permits. Another consideration is the artificial nature of the market; the supply of the pollution rights is controlled by governments and regulators that can make surprising changes to the rules.

And even though the almost-daily auctions of allowances are 40 percent smaller, a measure of demand known as the cover ratio hasn’t picked up.

The market has always enjoyed some interest from financial firms. About half the companies buying allowances in auctions weren’t factories, power stations or airlines in 2016, the last year the European Union published data on the types of auction bidders.

To contact the editor responsible for this story: Reed Landberg at landberg@bloomberg.net, Andrew Reierson

©2019 Bloomberg L.P.