Glass-Half-Full Hedge Funds May Get Doused

Glass-Half-Full Hedge Funds May Get Doused

(Bloomberg Opinion) -- Fund managers appear to be betting that the long economic recovery and bull market will continue to age well. That wager, though, might be past its time.

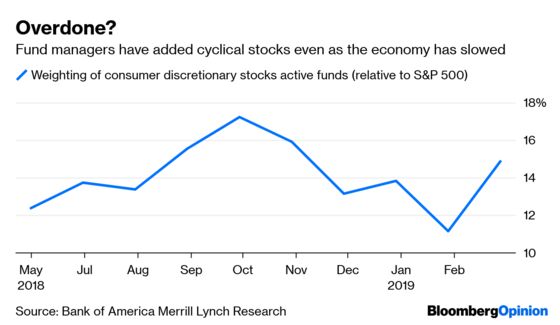

In Bank of America Merrill Lynch’s latest survey of active stock managers, which came out late Monday, strategists at the firm found that professional investors had upped their exposure to cyclical stocks to the highest level in four months as of the end of February. That was a quick turnaround from late last year, when enthusiasm for the sector was dropping. Back in October, fund managers recorded their lowest exposure to internet retailers since Bank of America began asking. Their bets on Amazon.com Inc. and others have since rebounded, with shares of Ebay Inc. up nearly 30 percent this year as just one example. Exposure to auto stocks by fund managers also doubled in the past three months, putting it at the highest since June 2016.

Among hedge-fund managers, consumer-discretionary stocks placed third among outsize sector bets, but all of the the top four comprised groups that are generally aligned with the economy. Communication services was the largest overweighted sector among hedge funds, followed by material producers, consumer-discretionary shares and industrial companies. Recession-resistant consumer-staple stocks, on the other hand, ranked among the least-held sectors by hedge-fund portfolios.

Investors’ seeming faith in the economy may be out of sync with what is really going on. The housing market was the first to give off a whiff of economic weakness, showing cracks last year. That was before corporate profit growth slowed faster than expected. The warning signs have been coming with more frequency lately. Friday’s February jobs report showed employers added just 20,000 positions to their payrolls, the lowest number for that month since 2010, and down from 330,000 additional hires in the same month the year before. On Monday, consumer sales were also weaker than expected. And economists now believe GDP growth could slow to within the 1 percent range in the current quarter.

None of this seems to have hurt hedge funds and mutual funds too badly, yet. Bank of America Merrill Lynch in another research report last week noted that through February, nearly 70 percent of all active growth funds – which tend to place more cyclical bets – were beating their index. Large-cap funds in general were up an average of 12 percent through February, about half a percentage point better than the S&P 500 Index.

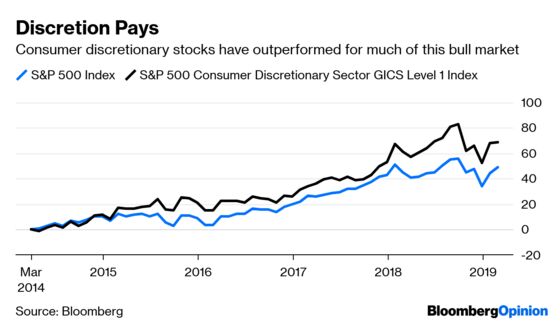

Cyclical stocks have turned down lately, though, and what was true for the first two months of the year hasn’t been the case in March. Shares of industrial companies have dropped nearly 3 percent this month. Financial stocks, too, are down slightly. Discretionary stocks, on the other hand, have continued to rise, though less than the market for the past two weeks. They’re still up 11.3 percent, trailing the S&P 500 only slightly.

It’s possible that fund managers have shifted their bets recently, which may explain some of the reversals. Still, as of the end of February, the average fund was overweight consumer discretionary stocks by about 15 percent, and underweight consumer staples by about 40 percent. It wasn’t always this way. For much of 2013, 2014 and 2015, fund managers had more of their portfolios in defensive sectors, like health care and utilities, than cyclical ones. That turned out to be a bad bet as the economy continued to chug along. Now that the economy is running out of steam, investors seem like once again they may be off schedule.

Theanalysis is all based on relative weighting.The Bank of America survey looks at how active professional stock-fund managers are weighting sector bets in their portfolios, versus how those sectors are weighted in the S&P 500.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Stephen Gandel is a Bloomberg Opinion columnist covering banking and equity markets. He was previously a deputy digital editor for Fortune and an economics blogger at Time. He has also covered finance and the housing market.

©2019 Bloomberg L.P.