Hedge Funds Back Off on Oil as Saudis Signal OPEC to Open Spigot

Hedge Funds Back Off on Oil as Saudis Signal OPEC to Open Spigot

(Bloomberg) -- Saudi Arabia is scaring hedge funds.

Money managers slashed bets on rising West Texas Intermediate crude prices to the lowest in more than a year, with total positioning on the U.S. benchmark down to a level last seen in 2015. While Saudi Energy Minister Khalid Al-Falih said OPEC is in “produce-as-much-as-you-can mode” to offset sanctions on Iran, a global equity meltdown and worries over demand haven’t helped either.

“You have sanctions on Nov. 4 that kick in and the big question is how much will those other countries” produce to make up the gap, said Mark Watkins, who helps oversee $151 billion at U.S. Bank Wealth Management. At the same time, “the global economy is showing some signs of stress and that’s making investors just a little bit more nervous as a whole.”

Saudi Arabia already boosted oil production to 10.7 million barrels a day, near an all-time high, and it can increase it even more to help plug any supply shortfalls due to U.S. sanctions against Iran, according to Al-Falih. Iraq also chimed in and said it will increase oil output. OPEC has been raising production since May.

Yet, OPEC later said the rise in oil inventories in recent weeks, coupled with fears about an economic slowdown, “may require changing course.”

Mixed Messages

“The market is grappling with the fundamental question: Are we oversupplied or under-supplied?” said Tamar Essner, an analyst at Nasdaq Inc. in New York. “We’ve been given very mixed signals from major producers.”

Hedge funds’ net-long position -- the difference between bets on higher prices and wagers on a drop -- in WTI crude tumbled 15 percent to 206,295 futures and options in the week ended Oct. 23, according to the U.S. Commodity Futures Trading Commission. Longs dropped 9.8 percent to the lowest in almost three years, while shorts bumped higher by 13 percent.

Investors are skittish after more than $6.7 trillion was lost in global equities’ value since late September, as expectations for earnings were tested amid heightened trade tensions and tightening financial conditions. The S&P 500 is on track for the worst month in eight years.

“It looks like people are de-risking and taking money off the table,” Essner said. “With the heightened uncertainty and volatility in the broader markets, you can’t overlook the increased correlation between oil prices and equities.”

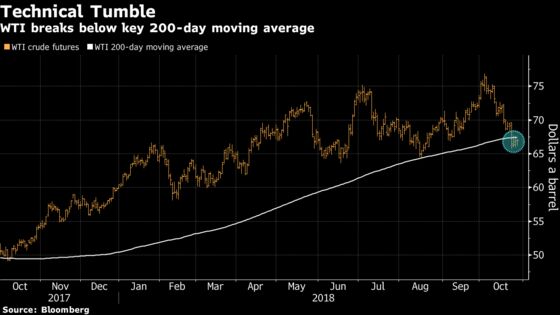

Technical charts also show weakness in crude. WTI closed below its 200-day moving average during the report period for the first time in a year, typically a bearish signal. And front-month WTI has closed at a discount to its second-month contract for more than a week, another indication of an oversupplied market known as contango.

But, it’s not all doom-and-gloom for the bulls. Hedgeye Risk Management says the oil market could be in for a surprise when U.S. sanctions on Iranian crude begin next month and Brent could gain $5 a barrel, with a spike to $90 a possibility.

| OTHER POSITIONS: |

|

To contact the reporter on this story: Jessica Summers in New York at jsummers24@bloomberg.net

To contact the editors responsible for this story: David Marino at dmarino4@bloomberg.net, Carlos Caminada, Simon Casey

©2018 Bloomberg L.P.