Hedge Funds Are Behaving Like We Just Had a Financial Crisis

Hedge Funds Are Behaving Like We Just Had a Financial Crisis

(Bloomberg) -- Hedge funds haven’t been chasing the January rebound in U.S. equities on the heels of their worst year since 2011.

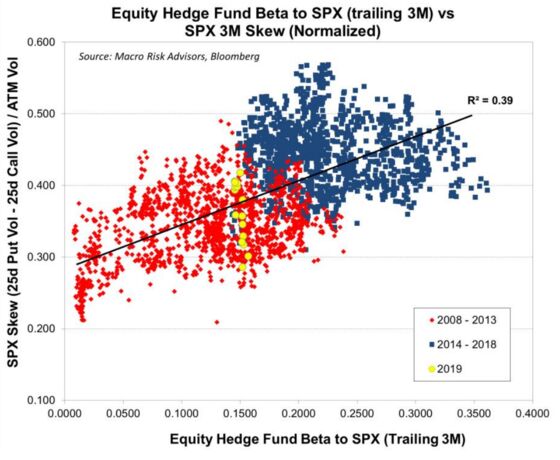

According to Macro Risk Advisors, these big-money managers are acting much more like it’s the aftermath of the 2008 financial crisis than the relatively low-volatility environment that’s dominated for most of the past five years.

The combination of hedge fund’s implied equity exposure to the S&P 500 Index and associated trends in the options on that benchmark gauge reveals the extent of their risk aversion. Equity derivatives strategist Vinay Viswanathan highlighted this dynamic in a Jan. 30 note to clients as reminiscent of the financial-crisis backdrop for U.S. stocks.

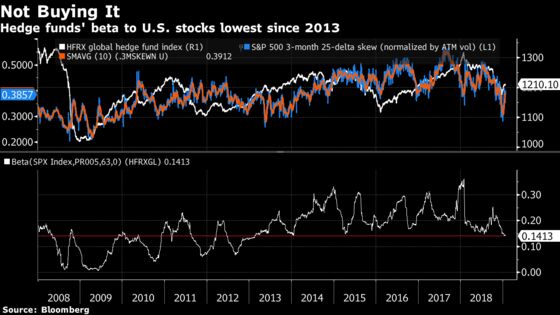

The portion of hedge funds’ returns attributable to the S&P 500 -- the trailing three-month beta -- is at its lowest level since 2013. Meanwhile, there’s relatively low demand for puts despite the December drubbing in equities and subsequent rebound.

According to the strategist, there are two likely explanations. Hedge funds may have added more to their short than long books -- in which case calls, rather than puts, would be the appropriate hedge -- or they don’t need to hedge because they aren’t loading up on long positions in U.S. equities.

“While speculative investors have seemingly not been scooping up tail hedges, the exposure of equity hedge funds to the S&P 500 has fallen with skew,’’ Viswanathan wrote. “The current level of equity exposure for hedge funds is more consistent with the 2008-2013 market regime than the 2014-2018 bull market.’’

Conversely, periods of higher hedge fund exposure to equities tend to occur in tandem with elevated option skew, he observes, offering a trading opportunity in options for investors willing to bet that these managers will warm to U.S. stocks and juice the current rally.

“In this environment, owning delta-hedged risk reversals (buying puts, selling calls, and buying shares -- a direct bet on skew) could be a unique way of betting on hedge fund exposure to equities rising,’’ wrote Viswanathan. “Naturally, that phenomenon should occur if the market continues to rally back from the carnage of 2018’s final quarter.’’

Read More: Hedge Funds Back in Sell Mode With Stock Exposure Near 2018 Low

To contact the reporter on this story: Luke Kawa in New York at lkawa@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Dave Liedtka, Randall Jensen

©2019 Bloomberg L.P.