Hedge Funds Aggressively Shorting VIX Shouldn't Ring Alarm Bells

Hedge Funds Aggressively Shorting VIX Shouldn't Ring Alarm Bells

(Bloomberg) -- Hedge funds shorting stock volatility en masse is the latest canary in the coal mine for those fretting dovish central banks are setting the stage for the next market blow-up.

Not so fast, says a growing chorus of Wall Street voices.

As policy makers squeeze monetary uncertainty from asset prices, the fast money is betting against further swings in U.S. equities, according to futures data on the Cboe Volatility Index, or the VIX. Net shorts are close to record highs.

But strategists are pushing back on fears that complacent traders are gripped in a speculative mania. They’re citing everything from the billions riding passive products tracking the long side of the wager to the smaller value of VIX shorts versus previous highs.

The positioning data overall paints a far “more nuanced” picture on the state of the volatility landscape, according to Bank of America Corp.

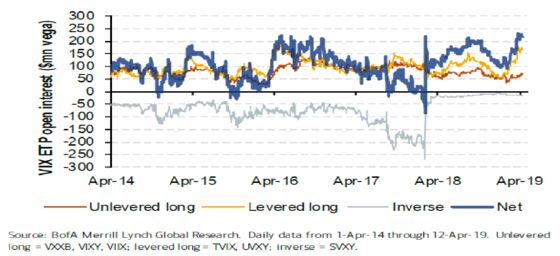

“Discussions tend to miss the other side of the trade -- namely, the net long volatility exposure in VIX exchange-traded products, which now stands near an all-time high,” strategists including Anshul Gupta wrote in a note.

Just look at vega, or the sensitivity of options to changes in implied volatility. At $215 million, the long vega in ETPs is greater than the short vega of the VIX futures shorts at $164 million, according to Bank of America data.

In other words, sliced and diced this way, the longs are sizeable.

Meltdown Memories

And for those obsessed with hedge-fund shorts, it’s foolhardy to take net-positioning data at face value.

Volatility speculators typically hold a mix of long and shorts either as a hedge or a relative-value strategy, with U.S. positions often the funding leg of global trades.

“We don’t care so much about ‘net’ positioning so much as we care about how much short vol is out there that could be covered,” wrote Pravit Chintawongvanich, Wells Fargo’s equity derivatives strategist, in a note. “Short VIX futures positioning is actually smaller than the previous highs and the net position looks the way it does because long VIX futures positioning is down a lot.”

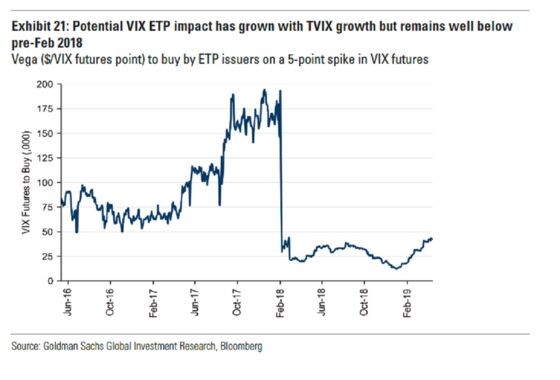

And it’s not even clear that investors in risk assets should fret too much about these signals from the volatility-derivatives market. While exchange-traded products that were short VIX futures arguably helped fuel February’s Volmageddon, their firepower has been considerably depleted.

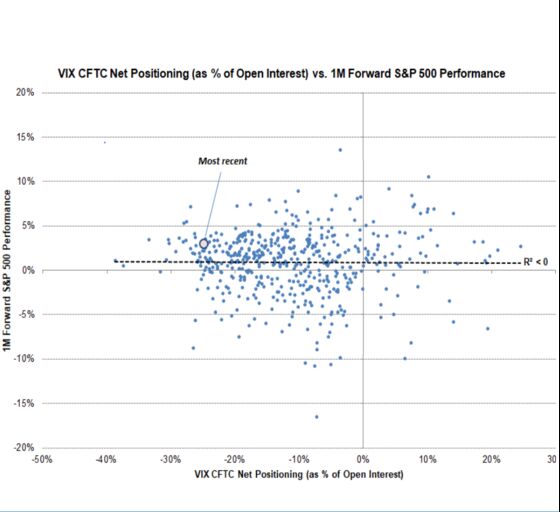

“We look to debunk any myth that extreme short positioning in VIX leads to a spike in the VIX in the near-term, particularly given the dampened effect of volatility ETPs following the events of February 2018,” Maxwell Grinacoff, quantitative strategist at Macro Risk Advisors, said in a note.

He found no real statistical link between net positioning in VIX futures and the forward one-month performance of the S&P 500, or the VIX itself.

That’s not to say futures speculation doesn’t matter.

In an equity sell-off, a feverish tug of war will break out between buyers of futures on the one hand and sellers on the other, pulling the contracts in opposite directions until an equilibrium emerges, according to the BofA strategists. All that will impact the VIX -- but outsized selling pressure is unlikely to spark a disruptive move.

As short ETPs are shadow of their former selves, large institutional sellers of volatility are more important players nowadays. These accounts have a higher pain threshold than the type of smaller retail players or leveraged funds that blew up in the first quarter of 2018.

Their presence was likely felt during the depths of the December equity sell-off when implied volatility was relatively cheap and skew, a cost measure for tail-risk protection, was suppressed. That all suggests the DNA of participants is just as important as the size of the short wagers.

“It is really a question of which side of the trade has the ‘weaker hand,’ i.e., is more reactive to risk as a vol spike unfolds,” the BofA strategists wrote.

To contact the reporters on this story: Yakob Peterseil in London at ypeterseil@bloomberg.net;Luke Kawa in New York at lkawa@bloomberg.net

To contact the editors responsible for this story: Samuel Potter at spotter33@bloomberg.net, Sid Verma

©2019 Bloomberg L.P.