Hedge Fund Manager Stakes Own Cash on a Bet Against Credit ETFs

Hedge Fund Manager Stakes Own Cash on a Bet Against Credit ETFs

(Bloomberg) -- After quitting his job at a $7 billion hedge fund to go it alone three years ago, Adam Schwartz happened upon a short so certain he built a notional position amounting to half his fledgling firm’s assets on it.

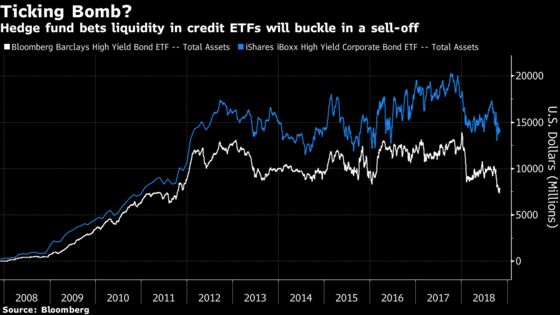

He’s been borrowing shares and stockpiling bearish options on exchange-traded funds that track major credit indexes, confident that a blow-up in fixed income will hit these passive vehicles the hardest.

Schwartz reckons it’s only a matter of time before rising rates choke off financing for highly leveraged companies, spurring a wave of bond defaults.

But running a hedge fund with mostly his own cash has given the 39-year-old freedom to bet on more extreme scenarios, like the one where credit ETFs -- which have vaulted to prominence promising liquidity comparable to stocks -- perish in the bloodbath.

“The ETF structure isn’t really designed for a large market sell-off,” Schwartz said by phone from Miami. “They will break if people don’t trust that they have the liquidity that they think they do today.”

Schwartz, who spent eight years at Jeffrey Tannenbaum’s Fir Tree Partners, is echoing a view held by some on Wall Street who warn that a day of reckoning is coming for the ever-popular instruments. While ETF providers such as BlackRock Inc. argue their funds provide a positive force by adding liquidity and price transparency in times of stress, others say they create a false sense of stability.

Black Bear Value Partners is small fry compared with the $630 billion market for bond ETFs, but you can’t doubt its convictions. Shorts make up about half of exposures by notional amount in the multi-asset hedge fund Schwartz set up and manages -- wagers that have yet to deliver much of a profit.

The positions involve products tracking U.S. credit and emerging-market bonds, he said, declining to disclose the fund’s size or the ETFs it’s shorting.

Investment-grade U.S. credit is particularly vulnerable because about half the companies in the major benchmarks have credit ratings just one level above junk, he says.

Rout Time

When the credit sell-off hits, Schwartz sees it playing out like this.

In a rout, where secondary liquidity in the ETF evaporates, authorized participants -- the only parties able to trade directly with the ETF -- will be compelled to redeem shares directly with the funds in exchange for bonds. But they’ll balk at receiving less-desirable securities, Schwartz believes.

Anxious to maintain orderly trading, the funds will give away their most liquid securities, leaving a portfolio clogged with distressed and illiquid notes. At some point, APs will refuse to transact with the fund, sending the ETF shares into a death spiral.

While what Schwartz and others predict is theoretically plausible, ETF proponents take pains to point out that it hasn’t happened yet. They characterize the frequent griping by active managers as sour grapes from those clinging to business amid the rising passive wave.

“People who are buying these things have to be pretty certain that the good times will last forever,” said Schwartz.

To contact the reporter on this story: Natasha Doff in Moscow at ndoff@bloomberg.net

To contact the editors responsible for this story: Samuel Potter at spotter33@bloomberg.net, Yakob Peterseil, Sid Verma

©2018 Bloomberg L.P.