Hedge Fund Killjoys Shun Reflation Trade That’s Sweeping Stocks

Hedge Fund Killjoys Shun Reflation Trade That’s Sweeping Stocks

(Bloomberg) -- Bets on faster economic growth are suddenly all the rage in the equity market. But one group of sophisticated investors is sitting out the trade.

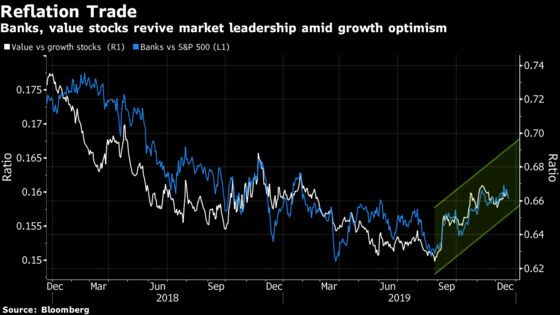

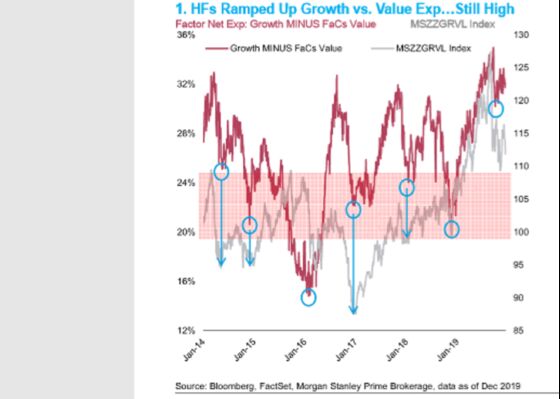

Hedge funds have remained steadfast this year in their aversion to companies seen as most poised to benefit from a pickup in economic growth, or reflation. As of mid-December, the industry was positioned cautiously, with cyclical holdings relative to defensive shares and exposure to growth versus value stocks both hovering near five-year lows, according to prime brokerage data compiled by Morgan Stanley.

The reticence of hedge funds stands out in a market where optimists are ratcheting up their growth expectations at a record pace and money is flowing to shares of banks, often seen as an economic barometer. As much love as financial stocks are getting, hedge funds are avoiding them. Their net positions in the industry are stuck near a decade low.

The existence of skeptics can be framed as good news as it signals the potential for more people to turn bullish and help propel further stock-market gains. On the other hand, it reveals some doubts underneath the recent buoyancy: What if there is no pickup in growth even after a U.S.-China trade truce and a new round of monetary easing? After all, a decade of near record-low interest rates has only been enough to spur the slowest U.S. economic expansion since World War II. Moreover, the trade dispute isn’t solved and the uncertainty over the U.S. presidential election is looming next year.

It’s “not yet time to engage in the reflation trade,” said Masanari Takada, a quantitative strategist at Nomura Holdings Inc. “The question of whether the first-stage trade deal leads to reflationary conditions without a hitch can not be considered in isolation from these future events.”

Read more: Maybe It’s Time to Start Worrying About Stock Euphoria

To be sure, caution has been the name of game for hedge funds over the past two years as they mostly refused to embrace any equity rally amid an aging bull market. Their skepticism proved prescient in 2018, when the S&P 500 fell to the brink of a bear market in the fourth quarter. During this year’s record-setting rally, they’ve paid a price for largely sitting out the gains.

They’ve started to step up buying since October, though it’s mostly done through short covering. As a result, their bearish bias toward some cyclical shares has eased. For instance, they’re no longer short retailers. And their net exposure in chipmakers has climbed toward the historic average after hitting the lowest level in at least four years, Morgan Stanley data showed.

Their overall tilt, however, continues to favor stocks that either offer higher dividends or are seen as especially resilient to an economic slowdown. According to Morgan Stanley’s latest tally, software and interactive media companies account for two of hedge fund clients’ largest growth exposures on the long side.

Hedge funds will get left behind should the reflation trade keep going. Cyclical shares such as banks are taking over leadership from defensive companies like utilities while value stocks in the S&P 500 Index are poised to beat their growth counterparts for a fourth straight month.

Growth optimism is spreading so fast that the percentage of money mangers in a Bank of America survey expecting the global economy to improve over the next 12 months just had the biggest two-month jump on record. If that consensus is right, hedge fund managers may have to play catch-up.

“Hedge funds maintained relatively low directional exposure throughout much of 2019, which limited the amount of market beta that was captured,” Morgan Stanley wrote in the note to clients. “There could be more ‘normalization’ of these trends in 2020 and there’s plenty of room for positioning to adjust.”

To contact the reporters on this story: Lu Wang in New York at lwang8@bloomberg.net;Melissa Karsh in New York at mkarsh@bloomberg.net

To contact the editors responsible for this story: Brad Olesen at bolesen3@bloomberg.net, Brendan Walsh, Dave Liedtka

©2019 Bloomberg L.P.