Hedge Fund Investors Ditch Misfiring Quant Trade Losing Billions

Hedge Fund Investors Ditch Misfiring Quant Trade Losing Billions

(Bloomberg) -- Quant strategies designed to zig when markets zag are getting thrashed by extreme stock swings in a year that should have proved their shining moment.

These market-neutral funds keep lagging other alternative strategies, while Eurekahedge data this month showed they’re already reeling from $2 billion of outflows in 2020.

Not only did they largely fail to live up to their promise in the historic equity selloff, the ferocious rebound is confounding their risk models with its unprecedented whiplash.

After years of disappointment, the investing style -- which combines long and short bets to buck the overall market direction -- ranks among the least popular breed of hedge fund in a Barclays Capital Solutions survey.

All this is intensifying a debate on whether now is just the time to revamp this systematic cohort. Making risk indicators more flexible and adding short-term signals to guide allocations are among the fixes put forward by the likes of Franklin Templeton and Jupiter Asset Management.

“Some of the things people are traditionally focused on didn’t provide the returns they were expecting,” said Brian Meloon, managing director for research at Campbell & Company, citing the underperformance of short bets this year.

While the nuts and bolts of their strategies may vary, a few generalizations are possible. As fundamental signals failed to predict the right winners and losers in a pandemic market, even having a short book was not enough to make up for losses in the long leg.

With more rigid risk controls, many funds were also forced to deleverage at the height of the selloff, leaving them unprepared for the subsequent rebound.

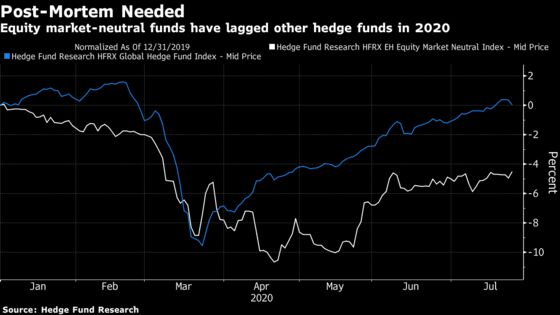

All that means market-neutral funds have dropped nearly 5% this year to lag a flat performance among hedge funds overall, Hedge Fund Research data show. Some have shuttered entirely. High-profile stumbles -- like the 20% loss for Renaissance Technologies’ institutional fund -- show the exceptional mayhem wrought by the pandemic.

At Los Angeles Capital Management, Chief Investment Officer Hal Reynolds saw the mania up close. Some of the signals his quant model usually used to predict stock behavior stopped working in the grip of the selloff, so the firm built a Covid factor to track how different shares are exposed to the virus.

The team discovered that while value shares are increasingly sensitive to the pandemic, growth shares are becoming less so -- reinforcing their bias toward the latter ever since.

“The megacap tech companies that are really driving the digital economy, they’re benefiting from the crisis,” said Reynolds.

Ian Heslop’s team at Jupiter is also studying better ways to run the value factor and looking at less standard factors and shorter-term signals. Alternative data that are specific to particular stock sectors look promising too, he added.

“If you have a material amount of fundamental underpinnings to your portfolios then you’d be getting quite a few of these stocks wrong,” said Heslop, head of global systematic equities. His $1.5 billion market-neutral fund is down 3.4% this year.

This need for a Covid factor attests to just how little use fundamental indicators like profit margins and valuations are in unprecedented times. It suggests there are benefits in making trading rules more flexible for an industry that has traditionally touted the long-term benefits of all-weather strategies.

The pandemic is intensifying a long-term performance problem. While hedge funds should not, by definition, be directly compared to a benchmark, a nearly 200% gain in the S&P 500 over the past decade has undoubtedly boosted pressure on an industry that looks ineffective next to it.

Market-neutral funds have performed even worse than their peers including macro and long-short funds since 2010, HFR data show.

One issue is that quants are more likely to use fixed volatility levels to manage their leverage. That caused many to miss this year’s rebound after getting thrashed in the market rout.

“These losses triggered further deleveraging in these funds, causing many of them to be under-invested for the recovery,” said Justin McEntee, who oversees such strategies at a Franklin Templeton unit allocating to hedge funds.

Those who have fared better were more flexible with risk, used the options market to capitalize on spiking volatility and quickly modeled a new factor to minimize their exposure to Covid-19, according to McEntee.

Some quants are hopeful the wild swings have left behind a litany of dislocations they can now exploit. But the gut-wrenching stock moves in recent months are still largely stopping market-neutral strategies from taking high levels of risk.

“Our models are not thinking about a day or a week, we’re looking at a year,” said Reynolds at Los Angeles Capital.

©2020 Bloomberg L.P.