Hedge Fund Investor Has Tense Flashback to Late 1990s Japan

Hedge Fund Investor Has Worrying Flashback to Japan 20 Years Ago

(Bloomberg) -- Luke Newman, an equities fund manager at Janus Henderson Investors, is having an uneasy feeling of deja vu.

Two decades ago, at the start of his career, Newman was covering Japanese stocks as an analyst at Deutsche Asset Management. Now, as a hedge fund investor in European equities, he’s noticing some parallels in the region with the Japan of the late 1990s and it’s making him nervous.

“We see a lot of quite worrying similarities between what we witnessed in Japan over the last 20 to 30 years and Europe,” Newman, who manages about $7 billion in long-short equity strategies, said in an interview in London.

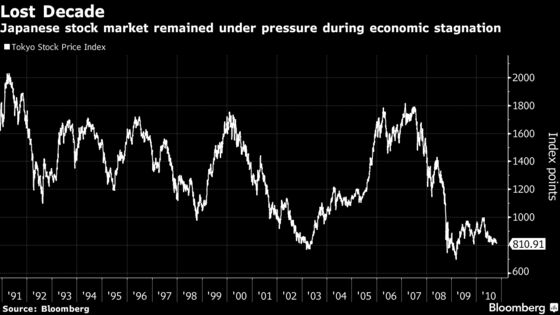

Correlations between Europe’s current position and Japan’s lost decade keep piling up with tepid economic growth, slow inflation and low bond yields. The key risk in such an environment, according to Newman, is getting stuck with highly leveraged companies that don’t provide a robust cash flow. Instead, he recommends focusing on the so-called growth stocks, or firms with strong balance sheets and earnings expectations.

“If the market sniffs any risk of deflation, the last thing you want is financial leverage,” said Newman. “And the winners have been those companies that can demonstrate that they can grow their top line in a world with no growth.”

Newman joins a growing chorus of strategists and fund managers, including Pacific Investment Management Co., in worrying about Europe’s growing similarity to Japan. This has investors doubting that the European Central Bank will be able to extricate itself from a negative interest-rate policy, mirroring Japan’s struggle to revive its economy from years of flat-lining growth.

Quality and growth stocks have been a big winner of this year’s rally as investors sought companies that could provide both protection and a return in a late-cycle environment. However, such inflows have made the valuations of some of the more popular European stocks like Nestle SA swell to record highs, making them an expensive and a potentially risky bet.

Here, too, Newman sees a similarity to his days of covering Japanese companies in the early 2000s, when he couldn’t comprehend why Toyota Motor Corp. was trading at such elevated price-to-earnings levels compared to other car stocks. But now he understands that back then, Toyota was the equivalent of a contemporary European quality growth stock. And if geopolitical or growth risks persist, such companies can rise even further, he says.

“If the market believes there’s downside risk to the U.K. or even U.S. yields from here, I wouldn’t be surprised to see those quality growth companies trading at even higher levels,” he said.

At the same time, the likes of JPMorgan Chase & Co. are bullish on both the euro-zone and Japanese stocks and believe that Europe is different from the land of the rising sun in a positive way: leverage levels in the private sector have stabilized and nominal growth and core inflation beat Japan’s deflation.

But Goldman Sachs Private Wealth Management’s Silvia Ardagna agrees with the sentiment behind the spreading investor anxiety over Europe’s lack of economic expansion.

“The fact that growth has been very low has been a big concern,” said Ardagna in an interview. People worry that Europe is going through a Japanification -- there’s very little space to stimulate growth.”

From watching Japan, Newman also learned that a market that rewards growth stocks can go through several months when investors move “violently” in the other direction. Newman said this helped him prepare for the shift into the cheaper, so-called value stocks that occurred in Europe in September and continued in October, when the fund shorted some high-quality tech and utility companies.

However, in the long run, he says that growth shares are still the better bet.

“It’s still a balanced argument but in the absence of any new reflationary policies, such as a sustained period of well targeted fiscal stimulus, it is hard to see why low valuation alone would support cyclically exposed, overly leveraged industrial or financials,” Newman said.

--With assistance from Michael Msika.

To contact the reporter on this story: Ksenia Galouchko in London at kgalouchko1@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, Jon Menon, Celeste Perri

©2019 Bloomberg L.P.