Hedge Fund That Timed Big Short, Crypto Rally Eyes Venezuela

Hedge Fund That Timed Big Short and Crypto Rally Eyes Venezuela

(Bloomberg) -- Venezuela’s bond market has been rocked over the past few years by defaults, sanctions and a collapse in crude oil prices. Yet the disastrous cocktail is attracting hedge funds including London’s Altana Wealth Ltd. that say the situation can’t get any worse.

Altana is pitching the South American nation’s government notes, which can be bought at pennies on the dollar, as the “trade of the new decade,” according to two letters to investors seen by Bloomberg.

In one of the letters, founder Lee Robinson said he plans to launch a Cayman Islands-based portfolio next month to capitalize on Venezuelan bond prices that he says could eventually multiply tenfold. He compared the risk-reward to returns delivered during the dot-com craze of the 1990s, shorting sub-prime mortgages before the collapse of that market in 2008 and riding the cryptocurrency rally in recent years.

“At these levels, the downside is low and the upside is the best we’ve ever seen for a sovereign debt restructuring,” Robinson and his colleague Steffen Kastner wrote in one of the letters.

A spokesman at Altana declined to comment.

Robinson, who previously worked for hedge fund billionaire Paul Tudor Jones, has a track record with opportunistic wagers. In 2014, he started a digital currency fund, which rode a rally in Bitcoin to four-digit returns.

Altana manages about $300 million across a number of funds including currency and distressed debt money pools.

Only a small pool of investors have both the patience and the legal ability to make the trade. Sanctions imposed by the Trump administration last year prevent U.S. funds from buying Venezuelan debt. That means firms from Europe to Latin America and the Middle East are the primary buyers, oftentimes through vehicles domiciled in the Cayman Islands for tax purposes.

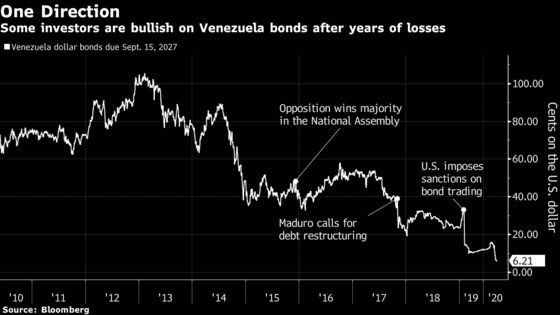

The nation’s dollar bonds due in 2027 fetch 6.25 cents, while state-run Petroleos de Venezuela’s notes due in 2020 trade at 11.64 cents. Those prices can’t drop much lower. The risk for investors is how long they’ll wait for a restructuring as the country careens toward its eighth straight year in recession and grapples with hyperinflation, sanctions and declining crude exports.

Venezuela’s situation is complicated further by its political crisis. Nicolas Maduro’s regime has access to most accounts in Caracas, yet U.S. courts recognize opposition leader Juan Guaido as the head of state.

In one of its letters, Robinson’s fund said it hired legal advisers to file claims in court to protect against statute of limitations. The firm’s thinking is that U.S. restrictions on the bonds, which drove last year’s steep decline, will eventually be lifted and the recovery value on the debt in a restructuring far exceeds market prices, according to the letters.

‘Five-Year Investment’

Altana isn’t alone in taking a closer look at Venezuela’s bonds.

Francisco Ghersi and Carmelo Haddad, who oversee Knossos Asset Management, made a name for themselves with their big bets on the nation’s debt. But after the government defaulted in late 2017, the Caracas natives diverted their attention to other high-yield Latin American notes from Argentina to Ecuador.

Now, they’re looking to buy a mix of Venezuelan bonds and stocks. Their thinking is that one day -- be that months or years away -- a market-friendly leader will return to power in Caracas.

“It’s a five-year investment,” Ghersi said. “It’s a bet that in the long run something will happen and the prices are good enough to put some money to work.”

©2020 Bloomberg L.P.