Heady Time for Dollar as Questions Swirl on Strength, Volatility

Trump repeats his dislike of an overly strong greenback

(Bloomberg) -- U.S. President Donald Trump’s ire at the dollar’s resilience is setting him at odds with those traders who have been turning its strength and stability into a source of revenue.

The greenback’s relatively high yield and muted volatility have made it a destination of choice for investors seeking to benefit from the so-called carry trade. But recently they’ve been starting to question how long the favorable conditions will last, and fresh comments on Saturday from Trump warning that the currency is too strong may inject an extra measure of uncertainty.

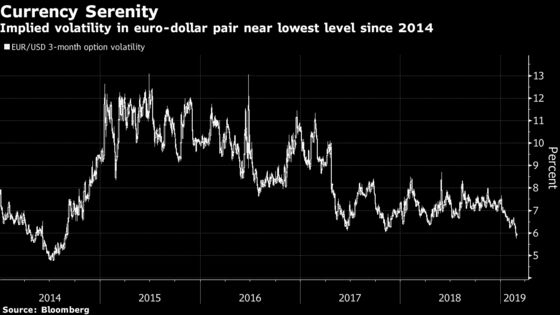

The greenback has so far defied many bearish forecasts for 2019, with a cooling global economy and a dovish tilt by central banks around the world keeping a number of other currencies such as the euro under pressure, even as the Federal Reserve hits pause on further rate hikes. While Treasury yields have retreated amid the Fed’s recent policy pivot, those in Europe, Japan and elsewhere are mired close to all-time lows, maintaining a healthy premium for U.S. debt. And implied volatility in major developed-market currencies has been edging down close to levels unseen since 2014.

That has created conditions that are ripe for carry trades: where traders borrow in lower-yielding currencies such as the euro and put that money to work earning interest in something higher-yielding like the dollar. The risks to this, though, are that volatility will pick up or that the greenback itself could lose value, whittling away any potential profit from the interest-rate differential.

Trump, who has previously lamented the valuation of the greenback, said over the weekend that the U.S. dollar is too strong and he also took a swipe at Federal Reserve Chairman Jerome Powell as someone who “likes raising interest rates.”

“I want a strong dollar but I want a dollar that does great for our country, not a dollar that’s so strong that it makes it prohibitive for us to do business with other nations and take their business,” Trump said.

The dollar weakened by as much as 0.2 percent against the yen and as much as 0.3 percent versus the euro in early Monday trading in the Asia-Pacific, although it remained within its Friday ranges against both. The Bloomberg Dollar Spot Index erased losses to be little changed in early London trading.

For traders, a reckoning could be on the way later this year if the dollar bears ultimately prove correct, and the diminishing attractiveness of the carry trade might in turn fuel U.S. currency weakness.

“The strength we’ve had in the dollar has been closely related to the fact that interest rates are higher than everywhere else,” Andrew Sheets, Morgan Stanley’s chief of cross-asset strategy, said before Trump’s weekend comments on the currency. “In 2019, those factors are in the process of peaking and reversing. If that happens, then I think relative interest rates between the U.S. and the rest of the world should put in a peak. If so, then the currency should peak.”

The median forecast of analysts surveyed by Bloomberg is for the greenback, as measured by Intercontinental Exchange’s U.S. Dollar Index, to tumble by more than 4 percent this year from levels reached late Friday. It had climbed by more than 6 percent over the past 12 months as of Friday.

The ICE Dollar Index is just one measure of greenback strength, and one that is focused on how the currency performs against a small group of developed-market peers. While it’s up about 0.3 percent since the end of 2018, a trade-weighted gauge from the Fed was down by around 1 percent as of Feb. 22. The Bloomberg dollar index, which also includes emerging currencies, was off by around 0.2 percent on the year as of Friday’s close.

Much of that may reflect solid performance this year by a number of emerging-market currencies, which are themselves a popular place for carry traders to invest. After many years as a low-rate funding currency to rival the likes of the yen as a go-to haven, the dollar is now going head-to-head with high-yield developing-market peers that often rise and fall with global risk sentiment.

Over the past 12 months, a dollar carry trade funded by the euro would have returned about 11.6 percent as of early London trading Monday, based on data compiled by Bloomberg. Among a list of 31 major currencies tracked by Bloomberg, that was bested only by the Mexican peso and the Indonesian rupiah. Of course, that period also saw the dollar appreciate by more than 7 percent against the euro in spot terms alone, and a reversal of fortune could see much of that benefit undone for unwary traders.

Noelle Corum, a portfolio manager at Invesco’s fixed-income group, said she’s looking for currencies in places where growth expectations have gone “too pessimistic” and that could especially strengthen once the dollar takes a turn.

“I definitely think that the dollar will be weaker” by the end of the year, Corum said. “Think about what’s currently priced in. Where’s the growth going to come from?”

--With assistance from Benjamin Purvis and Paul Dobson.

To contact the reporter on this story: Justina Vasquez in New York at jvasquez57@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Greg Chang, Boris Korby

©2019 Bloomberg L.P.