Hate the President? It’s Showing Up In Your Work Rating Bonds

Hate the President? It’s Showing Up In Your Work Rating Bonds

(Bloomberg) -- In politics, people’s passions come out. Now there’s evidence Wall Street analysts can’t always keep them at bay.

The phenomenon is explored in a November working paper called “Partisan Professionals: Evidence from Credit Rating Analysts." Authors Elisabeth Kempf of the University of Chicago and Margarita Tsoutsoura of Cornell University find party affiliation shows up in the rating of securities.

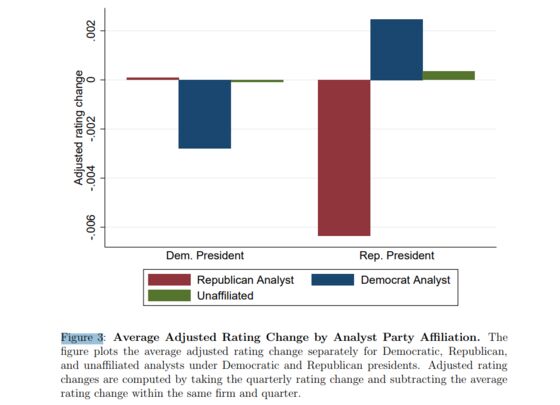

Kempf and Tsoutsoura wanted to see how personal preferences might shape a supposedly clinical process in finance, an inquiry that fits with the behavioral school of economics. The takeaway: bond ratings get more negative when they’re done by someone who isn’t in the party of the president in power.

“Partisan bias affects the decisions,” Kempf and Tsoutsoura write. “Analysts who are not affiliated with the U.S. president’s party are more likely to downward-adjust corporate credit ratings.”

To see if it was happening, the researchers looked at the evolution of ratings along the standard scale, from AAA on down. On average, an analyst who isn’t in the president’s party lowers ratings 0.015 notches more than someone from the same side of the aisle each quarter. Since the average quarterly rating change is 0.16, the effect is notable -- it accounts for a near 10 percent change.

The effect is magnified when partisan conflict is elevated. Using the Federal Reserve Bank of Philadelphia’s Partisan Conflict Index, which uses news articles to put a number on the degree of political disagreement, Kempf and Tsoutsoura find when the gauge increases by a single standard deviation, the effect of partisan bias on credit downgrades is 75 percent larger. The connection also grows during election quarters and among analysts who are more politically active.

“The importance of partisan conflict and voting frequency strongly support the interpretation that our results are capturing the effect of partisan bias, and further raises the bar for alternative explanations,” they write.

The authors sampled about 450 credit analysts who together cover more than 1,700 companies. All of the subjects worked at Fitch, Moody’s or Standard & Poor’s between 2000 and 2015, and their party affiliations were retrievable through voter registration records.

The effect observed in the study filters into markets where political leanings don’t register. On average, stocks fall almost 2 percent in the three days surrounding a cut to a company’s rating. And the stock market doesn’t notice any political preference.

“We find little evidence that the stock price response to a downgrade differs significantly when the downgrade is announced by an analyst who is ideologically misaligned with the president,” write Kempf and Tsoutsoura. “In other words, the stock market does not seem to correct analysts’ ideological bias.”

There are other real-world consequences. A firm with a lower credit rating could have a higher cost of capital, affecting investment decisions. The study finds that could amount to a change of 2.8 percent in a company’s investment plans.

“Rating actions by partisan analysts have non-negligible price and potential real effects,” the authors write, adding it “can therefore distort firms’ financing and investment decisions.”

To contact the reporter on this story: Sarah Ponczek in New York at sponczek2@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Chris Nagi

©2018 Bloomberg L.P.