David Harding Rewrites Winton Hedge Fund Playbook in Search of Returns

David Harding Rewrites Winton Hedge Fund Playbook in Search of Returns

(Bloomberg) -- David Harding was a hedge fund pioneer whose quantitative models generated double-digit returns for decades. Today, he’s in the unusual position of having to reinvent his business all over again.

The algorithms he built don’t work so well anymore.

“It’s pretty tough to make money in the hedge fund game at the moment,” Harding, 57, said in an interview with Bloomberg Television in New York. “Quite a lot of these strategies have become crowded, more money has been squeezed into a narrower space and the return-to-risk ratio is deteriorating.”

That’s what happened to “trend-following,” the strategy that Harding helped develop in the 1980s and which his London-based Winton Group relied on heavily until an abrupt shift in 2018. It also describes the situation confronting rival quant managers whose returns have also suffered, such as AQR Capital Management and Systematica Investments.

Quants now face a dilemma: keep trading the same way hoping that returns improve or spend time and money on new strategies that might not work. Harding concluded the status quo wasn’t an option if he wanted to keep competing in the hedge fund game.

Last year, reeling from one of his worst monthly losses since the financial crisis, Harding took drastic action. He slashed trend-following from a 50 percent weighting in the flagship Winton Fund to 25 percent and started rewriting the firm’s playbook. Winton would trade thousands more securities, expand into new markets and develop fresh algorithms to try to recapture its former edge.

“The fees have been coming down, the asset sizes have been increasing, a lot of firms are being pushed to the wall,” he said. “I’ve definitely not got my back to the wall, but I am absolutely driven to innovate and can’t afford to be complacent.”

Trading 7,000 Stocks

Winton now trades about 7,000 stocks, up from 1,500 as recently as four years ago. It’s testing ways of generating trading signals from company events such as acquisitions and leadership turnover. The firm has a major project in grain futures that involves time-series modeling with data stretching back more than 100 years. It’s also studying weather patterns to see if there’s a way to predict -- and trade -- climate change.

There’s a catch, however. Many of Winton’s clients had signed on because they wanted trend-following. As Harding began shifting away from his mainstay, some abandoned him. Investors pulled about $3.8 billion last year -- much less than his worst-case scenario. The firm now manages $23.5 billion, down from $33.7 billion in 2015.

Harding, who studied natural sciences at Cambridge University and remains a believer in the cold truth of data, co-founded his first hedge fund while in his 20s. He was hand-drawing charts as a futures trader in London when he had an epiphany: markets were inherently inefficient and could be beaten by computers that systematically buy and sell according to programmed instructions.

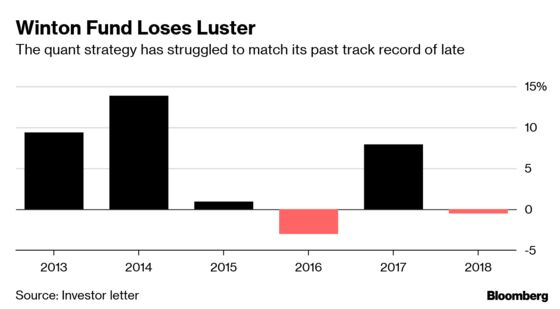

Early on, he embraced trend-following, a quant strategy that anticipates further price changes in the same direction. Once so reliable that the Winton Fund boasted average annual returns of 19 percent for two decades, trend-following has lost its steam.

The fund dropped 3 percent in 2016 before rebounding with a 7.9 percent gain in 2017. In February of 2018, an exceptionally volatile month in markets, it plunged 5 percent and finished slightly down for the year. The fund has yet to make money in 2019.

DIY Trend Following

Harding’s old money machine has become a commodity.

“You can do it at home,” he said. “Once something becomes that easy and that accessible, then you know you’re not going to make substantial supra-normal returns doing it.”

Another reason: less leverage. While borrowed money helped to stoke Winton’s returns in the past, Harding said he’s leery of using it now because “crowdedness creates the risk of catastrophe, the risk of an overnight massive move.”

Winton has since reduced costs to investors. It shaved its management fee to 0.9 percent from 1 percent a couple of years ago, and takes 16 percent of investment profits, down from 20 percent. Redemptions, Harding says, have stopped.

Now, Winton’s founder needs his experiments to start working. He says the expanded strategy hasn’t yet improved returns. Building new models is no different from scientific investigation; progress is incremental, with no guarantee of success.

The firm, for instance, spent two years and several million pounds trying to build a trading strategy based on purchasing managers indices -- economic data culled from company surveys. The effort yielded nothing conclusive.

“We definitely will discover things,” Harding said. “The question is whether they’ll be significant or important. We hope to make world-changing discoveries, but that’s not something you can do to order.”

To contact the reporters on this story: Erik Schatzker in New York at eschatzker@bloomberg.net;Nishant Kumar in London at nkumar173@bloomberg.net

To contact the editors responsible for this story: Margaret Collins at mcollins45@bloomberg.net, Vincent Bielski, Josh Friedman

©2019 Bloomberg L.P.