Half a Year of Gains and Many Unanswered Questions

Half a Year of Gains and Many Unanswered Questions

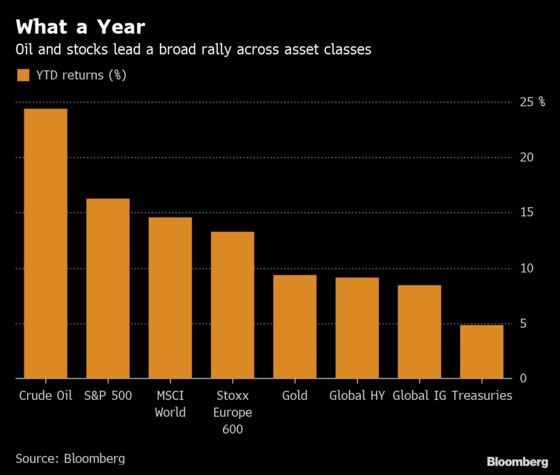

(Bloomberg) -- Trade jitters, political uncertainty, slower growth. All the issues that plagued investors and sent stocks sliding around this time last year still linger. Yet stocks are up 13% so far in 2019, the best performance in the first half since 1998. One key difference has been the dovish tone adopted by central banks of late. Traders may need more than that to keep them going through the rest of the year.

June is usually a bad month for equities, but not this year. Optimism spurred by comments from the ECB and the Fed propelled the Stoxx Europe 600 Index toward its best returns for the period since 2012. The rally has been broad, and across most asset classes.

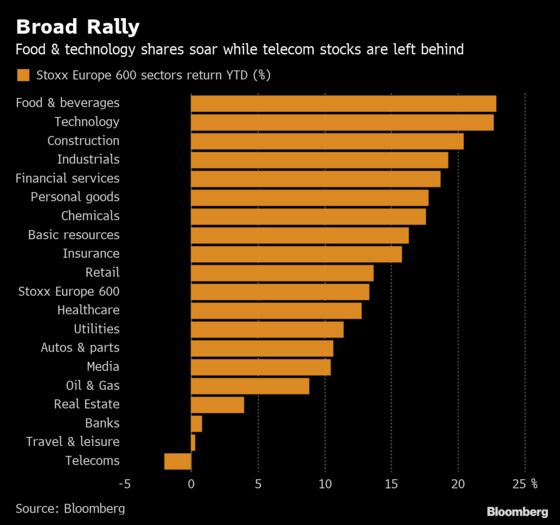

Sector-wise too, all are in the green except for telecoms. The networks are suffering from margin pressure, high costs of 5G licenses and regulations. Sanctions on Huawei are another hurdle for the industry as it might end up costing them $62 billion. Also trailing the broader market are banks and travel shares, with minimal gains.

Leading the advance are food and beverage makers, boosted by their defensive appeal and a broad exposure to global growth. The appetite for growth equities has also buoyed the technology sector.

That brings us to the growth-value performance gap, which has become more extreme. Barclays strategists sees potential returns for value stocks, but that depends on bond yields finding a floor. That might be a problem in the short term, especially if the ECB ends up cutting rates in the coming months.

The rally has done little to staunch fund outflows though. European stocks suffered nearly constant redemptions in 2019, taking the three-year total outflows to about $200 billion. Strategists have been wondering what could lure investors back. Nothing, says Societe Generale, which sees the trend as a structural re-balancing of portfolios into global and emerging markets funds.

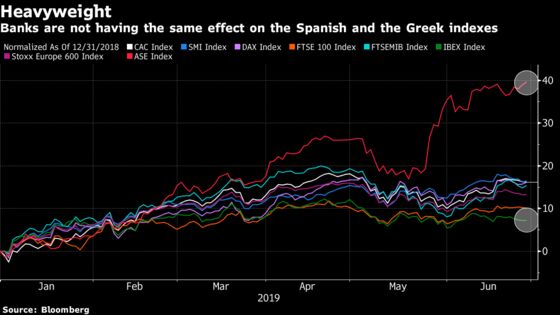

Country-wise, Spain is the laggard of Europe, penalized by weightings of banks and utilities. The IBEX even managed to record a worse performance than the Brexit-ridden FTSE 100. At the top, Greek banks are soaring, taking the country’s benchmark ASE Index close to 40% gains.

Overall, this looks like 1995 to Citi strategists, the last time that U.S. equities, bonds, IG, HY and oil all returned at least 10% in the same year, using annualized returns. Fun fact: the Fed also cut rates in July that year, something that markets are pricing in as a virtual certainty at next month’s meeting. Citi says European equities have, on average, returned nearly 10% in the 6 months following the first Fed rate cut.

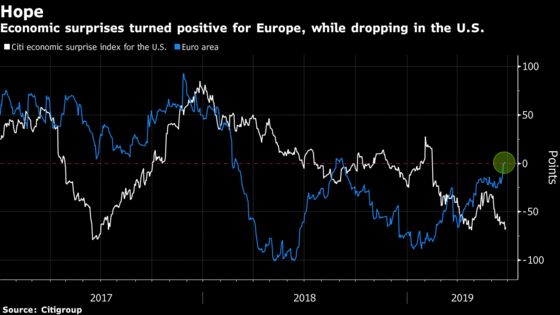

We’re not there yet, and given this is well expected, would it be enough? Earnings estimates are still being cut, while the future of global trade hangs on talks that have yielded little concrete developments so far. The G-20 summit starting today will still be closely watched, and the absence of escalation might be enough to please investors. One positive point for Europe is that economic surprises are in the green again. Further confirmation will be needed as it also happened last August before taking a turn for the worse.

In the meantime, Euro Stoxx 50 futures are trading little changed ahead of the open.

- Watch sportstwear manufacturers after U.S. Nike reported its first earnings miss for 7 years, though revenue met expectations. Watch Adidas and Puma, as well as retail company JD Sports Fashion.

- Watch Swiss equities after Switzerland barred shares listed in the country from trading in the European Union from Monday. Though manageable in the short-term, it could threaten the attractiveness of Swiss capital markets in the future.

- Watch the pound and U.K. stocks after Conservative Party leadership candidate Boris Johnson has kept open the option of suspending, or proroguing, the U.K.’s Parliament in order to force through a no-deal Brexit. Opposition to the move is strong. Theresa May has warned she may vote to stop a hard Brexit scenario. All this in the face of slumping consumer confidence in Britain.

- Watch crypto currencies and related stocks after Bitcoin went back to where it was before the five-day rally it just went through. Big investors in the market are still optimistic overall, but are wishing they’d sold off a bit more of their holdings before the rally reversed.

COMMENT:

- “Markets are now looking towards 2020 prospects”, Citi strategists write in a note. “Bottom up, analysts forecast 11% global growth. This looks high compared to our 7% top-down projection and suggests that more downgrades are likely. Fortunately, history suggests this should not be fatal for stock markets. Since 1989, there have been 15 years when global equities have risen despite analyst downgrades (including 2019 YTD). We expect 2020 to be similar.”

COMPANY NEWS AND M&A:

- VW’s Truck Unit IPO Raises $1.8 Billion, Pricing at Low End

- Merlin Entertainment Reportedly Set to Go Private for $7.6 Billion

- Orange Launches Sale of Remaining Stake in BT Group (1)

- Deutsche Bank Passes U.S. Stress Test in Surprise Fed Decision

- Credit Suisse Expects to Remediate Fed Concerns in Time

- Glencore Confirms 19 Fatalities at Congo Mine (2)

- Enel Plans to Raise 56.8% Stake in Enel Americas by Up to 5%

- BMW Denies Hiring Freeze Report; Aims to Keep Employment Flat

- Airbus Working on Tech for Single-Pilot Planes, CNBC Cites CTO

- HSBC Cuts Cash Rebate on Mortgage Refinancing in Hong Kong: HKEJ

- Boiron: French Body Advised Against Homeopathy Reimbursement

- Nyrstar Says No Decision Made to Date to Remove CEO

NOTES FROM THE SELL SIDE:

- Macquarie initiates Boohoo at outperform with a 315p PT that offers more than 49% upside, the broker calling the online retailer “a disrupter and a winner” in a fast changing fashion market.

- Bankhaus Lampe upgrades Tele Columbus to buy from hold, saying upcoming adjustments to growth strategy should see an uptick in value for investors. PT lowered to EU2.50 from EU4; that still offers more than 39% upside to Thursday’s close.

- Dialog Semi upgraded to buy from reduce, with co. strongly positioned for growth this year following reshaping of its product offering toward a portfolio which is gaining traction in the market, AlphaValue says.

- Plus500’s main challenges include client growth, revenue and profit, Peel Hunt says in note reinstating its rating of the company at reduce with PT of 526p and below-consensus estimates.

TECHNICAL OUTLOOK for Stoxx 600 index:

- Resistance at 392.7 (July 2018 high); 397.9 (May 2018 high)

- Support at 381.2 (50-DMA); 374.5 (61.8% Fibo)

- RSI: 54.1

TECHNICAL OUTLOOK for Euro Stoxx 50 index:

- Resistance at 3,514 (May high); 3,596 (May 2018 high)

- Support at 3,410 (50-DMA); 3,403 (61.8% Fibo)

- RSI: 58.2

MAIN RESEARCH AND RATING CHANGES:

UPGRADES:

- Brewin Dolphin raised to outperform at Macquarie; PT 3.64 Pounds

- Burberry upgraded to neutral at Goldman; PT 18 Pounds

- Dialog Semi upgraded to buy at AlphaValue

- H&M upgraded to hold at SEB Equities; PT 152.50 Kronor

- Julius Baer upgraded to outperform at Macquarie; PT 58.45 Francs

- PSP Swiss upgraded to neutral at JPMorgan; PT 115 Francs

- Sainsbury upgraded to neutral at Goldman; PT 2.15 Pounds

- Tele Columbus upgraded to buy at Bankhaus Lampe

DOWNGRADES:

- Epiroc downgraded to neutral at JPMorgan; PT 101 Kronor

- Wartsila downgraded to hold at HSBC; PT 14 Euros

INITIATIONS:

- Boohoo rated new outperform at Macquarie; PT 3.15 Pounds

- Ceres Power rated new buy at Liberum; PT 3 Pounds

- Equals Group PLC rated new market perform at KBW; PT 1.30 Pounds

- Ferratum rated new market perform at KBW; PT 11.90 Euros

- Funding Circle Holdings rated new underperform at KBW

- Hypoport rated new market perform at KBW; PT 290 Euros

- IntegraFin rated new outperform at KBW; PT 4.80 Pounds

- Nestle rated new hold at HSBC; PT 105 Francs

- Paypoint rated new market perform at KBW; PT 11.80 Pounds

- SMCP rated new buy at Oddo BHF; PT 20.50 Euros

MARKETS:

- MSCI Asia Pacific up 1%, Nikkei 225 down 0.5%

- S&P 500 up 0.4%, Dow little changed, Nasdaq up 0.7%

- Euro down 0.04% at $1.1365

- Dollar Index up 0.04% at 96.23

- Yen up 0.07% at 107.71

- Brent down 0.7% at $66.1/bbl, WTI down 0.7% to $59/bbl

- LME 3m Copper down 0.2% at $5979.5/MT

- Gold spot up 0.4% at $1415.3/oz

- US 10Yr yield little changed at 2.02%

ECONOMIC DATA (All times CET):

- 8:45am: (FR) May PPI YoY, prior 2.2%

- 8:45am: (FR) May Consumer Spending MoM, est. 0.3%, prior 0.8%

- 8:45am: (FR) May Consumer Spending YoY, est. 0.3%, prior 1.2%

- 8:45am: (FR) June CPI EU Harmonized MoM, est. 0.0%, prior 0.1%

- 8:45am: (FR) June CPI EU Harmonized YoY, est. 1.1%, prior 1.1%

- 8:45am: (FR) May PPI MoM, prior -0.6%

- 8:45am: (FR) June CPI YoY, est. 1.0%, prior 0.9%

- 8:45am: (FR) June CPI MoM, est. 0.0%, prior 0.1%

- 9am: (SP) 1Q F GDP QoQ, est. 0.7%, prior 0.7%

- 9am: (SP) 1Q F GDP YoY, est. 2.4%, prior 2.4%

- 9am: (SP) May Retail Sales SA YoY, est. 1.5%, prior 1.1%

- 9am: (SP) May Retail Sales YoY, prior 2.0%

- 10am: (SP) April Current Account Balance, prior 0

- 10:30am: (UK) 1Q F GDP QoQ, est. 0.5%, prior 0.5%

- 10:30am: (UK) 1Q F GDP YoY, est. 1.8%, prior 1.8%

- 10:30am: (UK) 1Q Current Account Balance, est. -32b, prior -23.7b

- 11am: (EC) June CPI Core YoY, est. 1.0%, prior 0.8%

- 11am: (EC) June CPI Estimate YoY, est. 1.2%, prior 1.2%

- 11am: (IT) June CPI EU Harmonized YoY, est. 0.7%, prior 0.9%

- 11am: (IT) June CPI EU Harmonized MoM, est. 0.1%, prior 0.1%

- 11am: (IT) June CPI NIC incl. tobacco YoY, est. 0.7%, prior 0.9%

- 11am: (IT) June CPI NIC incl. tobacco MoM, est. 0.1%, prior 0.1%

- 12pm: (IT) May PPI MoM, prior -1.5%

- 12pm: (IT) May PPI YoY, prior 2.8%

* For a daily wrap on developments in European equity capital markets, click here

To contact the reporter on this story: Michael Msika in London at mmsika4@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, Namitha Jagadeesh

©2019 Bloomberg L.P.