Copper-Gold Ratio Breaks From Treasury Yields in New Normal

Copper-Gold Ratio Breaks From Treasury Yields in New Normal

(Bloomberg) -- The relationship between the copper-gold ratio and Treasury yields, one Jeffrey Gundlach’s favored indicators, looks broken.

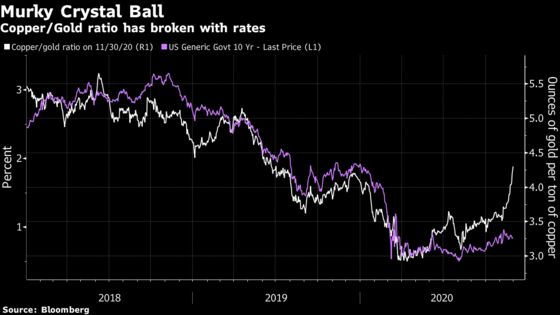

The ratio had an uncanny link to 10-year yield levels over the past five years. Yet in recent weeks, copper has rallied hard while gold plunged, sending the ratio to levels that suggest 10-year yields should be about double -- even with today’s eight basis-point jump to 0.92%.

To explain the breakdown, strategists are citing changes in demand for commodities amid uneven economic recoveries, as well as aggressive central bank stimulus policies as their long-term growth and inflation assumptions are challenged.

“Central banks have indicated that growth is allowed to run hot before they step in and change rates,” said Ole Hansen, head of commodity strategy at Saxo Bank A/S. “On that basis the correlation looks likely to break with growth and demand not being met by rising rates.”

Regime Shift

Many investors heed market observations by Gundlach, the billionaire money manager and chief investment officer of DoubleLine Capital. He has said the copper-gold ratio works “phenomenally well” as a short-term predictor of where Treasury yields are headed.

The correlation between the ratio and yields was statistically significant at about 0.5 measured on a weekly basis over the past five years, according to data compiled by Bloomberg. The previously stable relationship worked because copper is a cyclical commodity, and gold is a perceived haven with sensitivity to inflation and rates.

Now, it appears to be going through a regime shift -- a statistical term that implies large and persistent change in the structure of a complex system like the global economy.

That doesn’t mean that copper, gold and Treasuries will no longer correlate -- merely that the level at which they correlate, or even their relative betas, might shift.

Read More: Copper-Gold Ratio’s Crystal Ball for Treasury Rate May Be Broken

“Co-movement does not necessarily mean causality from one to the other,” said Harry Tchilinguirian, BNP Paribas SA’s head of commodity market strategy. ”Nor does it mean there is always a long-term stable relation between the two.”

Through the 1990s to the early 2000s, U.S. interest rates were much higher than the metals ratio -- based on a model using current data -- would have implied. Now, the assumption is that the Federal Reserve and other central banks are placing rates lower for expected levels of inflation and growth.

Copper Boom

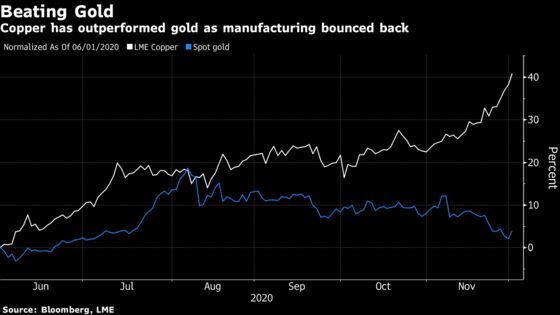

This repricing has altered the internal fundamentals of markets broadly, and commodities specifically. Gold, for instance, has taken a beating on the unwinding of a mania-like rush that drove 11 consecutive months of flows through October into gold ETFs. Meanwhile, copper is getting a boost from a faster recovery in manufacturing compared with services and an expectation of a pivot to greener policies.

“Booming Asian economies are boosting copper prices and hopes of a vaccine-related economic recovery in Europe and the U.S. is depressing gold and the dollar,” said Caroline Bain, the chief commodities economist at Capital Economics.

Rise of Asia

For others, the correlation breakdown between commodities and Treasuries may also reflect a shift in the engines of growth toward Asia, at the expense of the West -- a long-running trend accelerated in the wake of Covid-19.

While the virus is still raging in Europe and the U.S., China has seen a faster return to normal. That bodes well for copper demand, but doesn’t imply higher 10-year yields, which may be more beholden to “the tug of war” between catalysts including Covid cases and the timing of U.S. fiscal stimulus, according to Societe Generale asset allocation strategist Sophie Huynh.

“Asia is definitely the region where the certainty of recovery is now clear,” Huynh said. “Investors have more visibility on 2021 organic GDP growth.”

©2020 Bloomberg L.P.