GrubHub Outlook Sparks Slump While Bulls Keep the Faith

GrubHub Outlook Sparks Slump While Bulls Keep the Faith

(Bloomberg) -- GrubHub Inc. shares tumbled on Tuesday after the food-delivery company gave an outlook that was below expectations, although analysts continue to be positive on its longer-term potential.

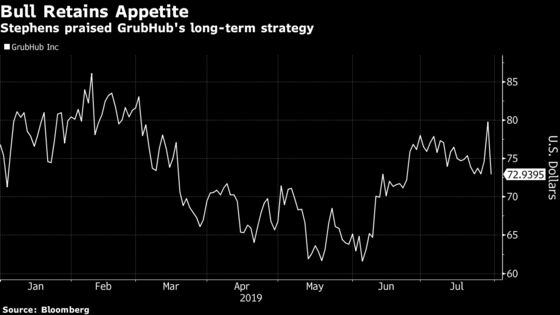

The stock dropped as much as 13%, and closing with a decline of that magnitude would represent the company’s biggest one-day wipe-out since October 2015. Shares last traded at $72.57, down 9% on the day. At current levels, the stock has lost half of its value since a September peak.

The company’s adjusted third-quarter Ebitda outlook stands at $53 million to $60 million, missing mid-point expectations of $61.5 million; it also lowered the higher range of its full year adjusted Ebitda to $250 million from $265 million.

Stephens analyst Will Slabaugh wrote that the “soft” guidance was related to higher marketing costs, an expense he favors.

“Despite the [near-term] profitability headwinds, we continue to support GRUB’s strategy to go after market share, which we expect to lead to upside in revenue and grow earnings power over time,” he wrote to clients. He affirmed his overweight rating and Street-high $135 price target, a level that implies an upside of more than 85% from current levels.

Beyond the outlook, Slabaugh wrote that GrubHub’s second-quarter results featured “broadly encouraging” trends for active diners and gross food sales, both of which came within expectations.

Thomas Champion, an analyst at Cowen, wrote that GrubHub’s third-quarter Ebitda outlook was “well below” consensus expectations, but added that the full-year revenue view topped forecasts. He kept his outperform rating and $103 target.

Tuesday’s move lower came just one day after GrubHub jumped nearly 7% on the back of analyst speculation that it could be a takeover target.

Following the second-quarter results, Bloomberg Intelligence wrote that industry consolidation was “likely, with GrubHub a potential target” of merger and acquisition activity. Analyst Andrew Eisenson added that slowing growth in metrics like gross food sales “reinforces our view that either more investments are needed or the company should seek to be acquired.”

Separately, D.A. Davidson touted the company’s abilities in a competitive marketplace, citing an internal test of GrubHub and its major rivals. “After analyzing and comparing prices and delivery times across the most popular food delivery apps, we found GrubHub and Seamless to offer the lowest prices and one of the lowest delivery times,” analyst Tom Forte wrote, affirming his buy rating and $100 price target.

To contact the reporter on this story: Ryan Vlastelica in New York at rvlastelica1@bloomberg.net

To contact the editors responsible for this story: Catherine Larkin at clarkin4@bloomberg.net, Jennifer Bissell-Linsk

©2019 Bloomberg L.P.