Growth Angst Shakes Markets Already Obsessed With Inflation Risk

Growth Angst Shakes Markets Already Obsessed With Inflation Risk

(Bloomberg) -- Investors who spent the last year stressing over inflation gave evidence Tuesday that obsession could be supplanted by -- or, worse, combined with -- worries about a slowdown in growth.

Spurring the shift is the shock that pervades markets when oil spikes as much as 12% in one day, a sight that can’t help but sow queasiness among traders weeks before Federal Reserve rate hikes while a war rages in Europe. Amid the anxious circumstances, investors bailed from stocks. They’re also diving headlong into bonds, where yields have plunged even though inflation fears persist, and may even increase amid fallout from the Ukraine war.

It was a subtle but notable change among investors who to date have been unconvinced the gathering clouds would translate into anything like a recession, at least in the U.S. While the view remains an outlier in light of robust growth projections and solid data, it’s an outcome investors looked less confident of avoiding based on the contour of trading Tuesday.

“What the market is doing now is pricing in for that increasing risk of a global recession and spiking energy, spiking commodity prices will aggravate that,” Bloomberg Intelligence’s Mike McGlone said on the “QuickTake Stock” streaming program Tuesday.

The S&P 500 sank 1.6%, with all sectors other than energy closing in the red. Banks and technology firms fell the most, with Apple Inc. sliding after saying it would halt sales of all products in Russia. The 10-year Treasury yield tumbled back below 1.75% after topping 2% before the invasion.

The price of oil rose Tuesday by the most in almost two years. West Texas Intermediate futures in New York surged to above $105 a barrel, contributing to the biggest gain in the Bloomberg Commodity Index in more than a decade. Rising prices not only hurt consumers at the pump but also make the cost of transacting business and shipping goods worldwide more expensive. JPMorgan Chase & Co. recently said prices are likely to average $110 in the second quarter.

Additional penalties against Russia -- a major oil producer -- are exacerbating the pressure on commodities prices, with the European Union identifying seven Russian banks it’s looking to exclude from the SWIFT messaging system. The nation banned residents from transferring hard currency abroad as President Vladimir Putin sought to counter the fresh sanctions walloping his economy.

“You have that specter of the late 1970s, early 1980s of that stagflationary fear of ever-ratcheting-down growth and ever-ratcheting-up inflation,” Alicia Levine, head of equities and capital markets advisory for BNY Mellon Wealth Management, told Bloomberg TV. “And what this conflict does is it plays into the inflationary piece.”

To be sure, economists see the economy continuing strong throughout 2022. Real gross domestic product is forecast to expand 3.7% this year, fortified by strong consumer spending and private investment. The economic backdrop is sturdy enough that Fed Chair Jerome Powell is expected to signal to lawmakers Wednesday that the U.S. central bank will go ahead with plans for raising interest rates in March, with traders mainly interested in whether comments hint of a potential half percentage-point move.

“One of the stranger arguments made in recent weeks has been the claim that the U.S. economy is on the verge of rolling over, or that we are entering a period of ‘stagflation,’” wrote Michael Shaoul, chief executive of Marketfield Asset Management, in a note Tuesday. “It still needs to be recognized that the starting point for monetary tightening is a very strong economy, with activity levels restrained by the availability of goods, materials, labor and logistics.”

But higher commodities prices have the potential to be a drag on growth and stoke inflation to the extent the Fed may need to tighten faster than it otherwise had planned. Strategists at Goldman Sachs estimate that a $10-per-barrel increase in the price of oil boosts U.S. core inflation by 3.5 basis points and headline inflation by 20 basis points. And though that also lowers GDP growth by just under 0.1 basis points, the hit to growth could be greater if geopolitical risks tighten financial conditions materially and increase uncertainty for business.

The “risk of a recession is rising as considerable upside remains to commodity prices, including oil,” said Marko Papic, chief strategist at the Clocktower Group. He makes a parallel to the 1973 Yom Kippur war, which led to the OPEC oil embargo. The S&P 500 fell as much as 16% then and was still down more than 40% a year later, Papic’s work shows.

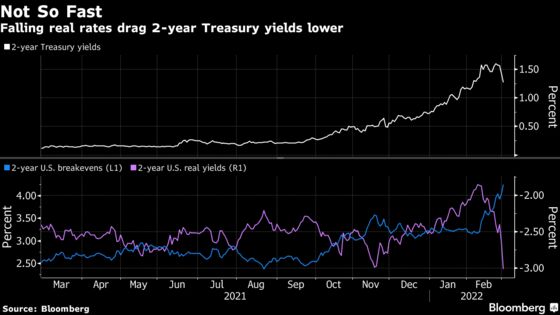

While risk appetite has ebbed and flowed in equities since Russia invaded Ukraine last week, demand for bonds as a haven has been brisk. Yields on benchmark Treasury notes have dropped by about 30 basis points after reaching a pre-pandemic high of 2.06% two weeks ago.

The move in short-dated Treasuries -- which are more sensitive to monetary-policy expectations -- has been just as violent, with two-year yields plunging 32 points in the past week. Traders have all but removed bets the Fed will raise rates by 50 basis points this month and now about five interest-rate hikes are priced in for 2022, compared to almost seven as of mid-February.

Rates markets are also flashing warnings that inflation is spiking at the same time growth expectations are flagging. Short-dated breakeven inflation expectations -- one component of nominal rates -- have soared to all-time highs, while real yields -- often viewed as a proxy for growth expectations -- sink deeper into negative territory.

As growth worries climb, bears also point to a model run by the Atlanta Fed, called the GDP Now forecast, which shows current-quarter growth tracking barely above zero. The tool is a real-time compilation of economic reports that evolves as data is released.

Meanwhile, strategists at Barclays cite another sign of frayed nerves: The put-to-call open-interest ratio for U.S.-focused exchange-traded funds last week hit its highest level since the 2020 Covid crash.

“Risk is now higher than normal across all main market classes,” wrote strategists led by Maneesh Deshpande.

Morgan Stanley’s Michael Wilson says that while uncertainties are ever-present, the current backdrop has more worry-factors than usual. Besides geopolitical concerns, he also says earnings growth could decelerate by more than expected. The negative-to-positive guidance ratio during the latest earnings season spiked to 3.6, the highest since the first quarter of 2016, a period mired in a global manufacturing recession. Additionally, earnings revision breadth is falling quickly and is close to turning negative.

Although fears of stagflation -- a mix of high inflation prints within a no-growth environment -- have started to swirl, most analysts say it’s too soon to ascribe the term to the current environment. That’s not to say they’re not worried about growth prospects. Investors have been partial toward defensive areas of the market, with energy, utilities and health care among the best-performing sectors over the past five sessions.

“Growth is still too strong for traditional stagflation to be a likely outcome. It seems stagflation-lite -- high inflation and slowing growth -- is what most people are worried about,” said Dennis DeBusschere, founder of 22V Research. “How long stagflation-lite fear lasts will dependent on how long the war lasts.”

©2022 Bloomberg L.P.