Goldman Warns SEC Proposal Could Shroud Hedge-Fund Crowding

Goldman Warns SEC Proposal Could Shroud Hedge-Fund Crowding

(Bloomberg) -- A proposal by U.S. regulators to change hedge-fund reporting requirements will make it harder to detect crowded trades, according to Goldman Sachs Group Inc.

The Securities and Exchange Commission wants to boost to $3.5 billion from $100 million the required amount in equity holdings traded on U.S. exchanges before a hedge fund needs to file a 13F form. The agency cites issues such as the cost burden on smaller funds to do the reporting, as well as the effects of market inflation and potential front-running by other market participants.

Goldman has tracked equity hedge-fund positioning quarterly since 2007. It said this change would cut the number of funds in its analysis to 59 from 822, and shrink equity assets covered to $815 billion from $1.2 trillion.

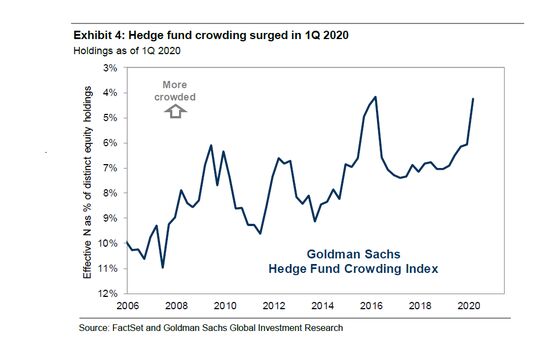

“The primary drawback of fewer hedge fund filings is lack of clarity around crowding risk,” strategists led by David Kostin said in a note July 17. “Reported hedge fund holdings allow investors to understand crowding risk, and to appropriately hedge portfolios.” However, they said their analysis of sector tilts would be “broadly consistent” with the original sample of funds.

Goldman said the change would likely prompt alterations to the methodology for constructing its Hedge Fund VIP List, which is derived from the 13F data and contains 50 stocks that appear most frequently among the top 10 holdings within hedge-fund portfolios. The basket has outperformed the S&P 500 in 61% of quarters since 2001 with an average quarterly excess return of 57 basis points, the strategists said.

Comments on the proposal are currently running 233-2 against the adoption of the updated regulation, according to Goldman.

Click here to see 13F filing summaries compiled by Bloomberg.

Risk managers used the data to identify crowded positions, and hedge funds characterize the cost of 13F filings as inconsequential, the strategists said. The front-running concern was backwards because the filing takes place after the purchase occurs and with a 45-day lag after quarter-end, they added.

“Clients believe transparency aids in price discovery,” the strategists said. “More information is better than less.”

©2020 Bloomberg L.P.