Goldman Models Impact of Rate-Shock Scenarios on Markets

Goldman’s analysis takes a hypothetical hawkish federal funds target-rate shock of 150 basis points.

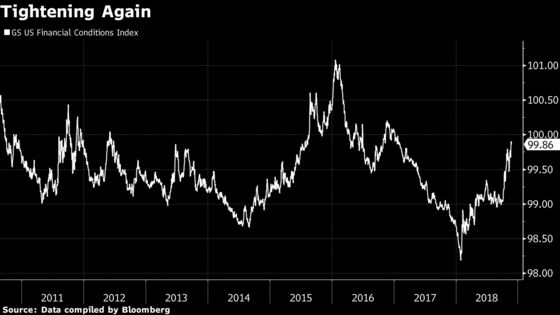

(Bloomberg) -- Goldman Sachs Group Inc. economists have proposed some “rules of thumb” for the impact of Federal Reserve interest-rate hikes on financial conditions and the U.S. economy, which showcase the importance of policy makers’ communications.

While an unexpected 1.5 percentage points of Fed rate rises would tend to boost 10-year Treasury yields by 45 basis points, cut equity prices by 9 percent and boost the dollar by 4 percent, anticipated monetary moves have a “much smaller” effect, Goldman’s modeling showed.

Ten-year Treasury yields have already climbed by more than 60 basis points this year, following 75 basis points of Fed rate hikes. The S&P 500 Index is down 1.5 percent for the year to date, while the Bloomberg Dollar Spot Index is up 4 percent.

Most forecasters see the Fed tightening by another 1 percentage point or less, with little likelihood of an acceleration from the quarter-point per quarter pace of the past year. Speculation instead has centered on the potential for a pause in 2019, in part thanks to the surge in financial-market volatility since early October. More hawkish Fed scenarios typically center on the historically tight job market at some point triggering a break-out of inflation.

“Our rule of thumb is that a 1 percentage point fall in the unemployment rate raises wage growth by 0.35 percentage points, but leads to a more modest 0.1 percentage-point rise in core PCE inflation,” Goldman economists including Daan Struyven wrote in a note Sunday. PCE inflation refers to the main gauge Fed officials use for their own projections.

The Goldman economists advised against an “overly mechanical interpretation” of their study. They also noted that relationships between the different factors can change over time and aren’t always linear, and that financial conditions are affected by many things other than Fed policy.

The study estimated that a 1 percentage point increase in the budget deficit relative to gross domestic product raises 10-year yields by about 20 basis points, based on historical average effects.

Goldman’s model now calculates the risk of a recession is 26 percent on a two-year horizon, up 5 percentage points this year -- mostly due to tightening financial conditions -- but still below average. For a three-year horizon, recession risk is now 43 percent, “just above the historical average,” the economists wrote.

To contact the reporter on this story: Joanna Ossinger in New York at jossinger@bloomberg.net

To contact the editors responsible for this story: Chris Nagi at chrisnagi@bloomberg.net, Christopher Anstey, Cormac Mullen

©2018 Bloomberg L.P.