Goldman Says Saudi Fiscal Adjustment Preferable to a Devaluation

Goldman Says Saudi Fiscal Adjustment Preferable to a Devaluation

(Bloomberg) -- A currency devaluation would be too costly for Saudi Arabia and the better option is to adapt to the oil shock through fiscal changes, according to Goldman Sachs Group Inc.

“Unlike a devaluation, fiscal policy can shift the burden of adjustment on those more capable of bearing it through, for example, taxes on luxury goods,” Farouk Soussa, a Goldman Sachs economist, said in a report. “This is not to say there would be no economic or sociopolitical costs, but we believe these would be lower than in the case of a devaluation.”

Saudi Arabia tethers its currency to the dollar and tends to move in lockstep with the U.S. Federal Reserve. While Goldman argues that the policy “has been of significant benefit to the Saudi economy over the years,” the arrangement comes under strain during oil downturns, since declines in foreign-exchange reserves erode confidence in the peg.

Read more: Gulf Currency Pegs Hold Firm Even as Oil Crashes. For How Long?

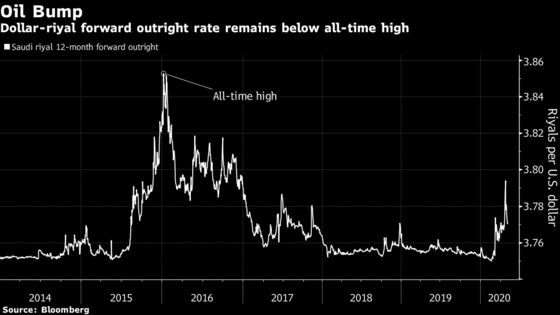

Pressure has again intensified this year with the collapse in crude prices and a drawdown of reserves. Still, 12-month dollar-forwards for the Saudi riyal are well short of the all-time high reached in 2016 after the previous crash in commodity markets.

- To maintain confidence in the peg, authorities need to have enough reserves to cover narrow money, as measured by the M1 gauge -- which includes the amount of currency in circulation and short-term local currency deposits. This “threshold level” of reserves is around $300 billion in Saudi Arabia

- Under Goldman’s base case, oil prices will recover to $40 per barrel by the end of this year and $60 by the end of 2021; in that scenario, Saudi reserves don’t drop through the threshold level and start to recover toward the second half of 2021

- In a “downside scenario” where oil prices remain at $30 indefinitely and with the peg at current levels, Saudi Arabia would require a minimum 50% devaluation to keep reserves above the threshold level in absolute terms; a devaluation of at least 80% would be needed to stabilize them

- The economy would experience inflation and balance-sheet shocks in case of a large devaluation

- Under the peg, Goldman projects that Saudi reserves will be depleted by early 2023 if oil prices stay at $30, all else equal

“An FX devaluation would have to be very large in order to generate an income effect sufficient to reduce external imbalances,” Soussa said.

Alternatively, to cope with oil at $30 per barrel, Goldman estimates that Saudi Arabia would need a fiscal adjustment of close to 15% of gross domestic product.

Scaling back current spending to 2016 levels alone would achieve around half of such an adjustment, it said. A doubling of non-oil revenue from their “current low base” of around 10% of GDP could contribute the rest, according to Soussa.

“The magnitude of devaluation of the riyal would have to be very large in order to be of material benefit to external and fiscal imbalances in a $30 oil price scenario,” Soussa said. “The most obvious alternative is an adjustment in fiscal policy.”

©2020 Bloomberg L.P.