Goldman Rips Into U.S. ‘Misconceptions’ About Share Buybacks

Buybacks have gotten an unfair rap in the U.S., according to a defense of the practice by Goldman Sachs Group Inc.

(Bloomberg) -- Buybacks have gotten an unfair rap in the U.S., according to a defense of the practice by Goldman Sachs Group Inc.

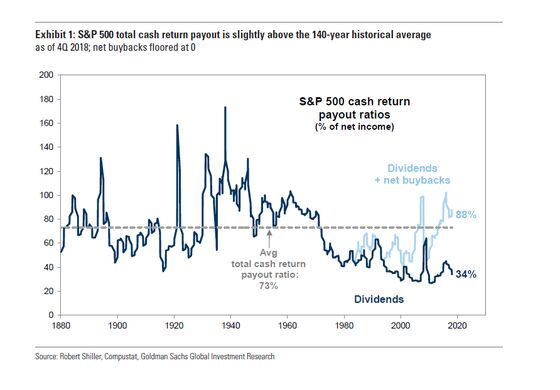

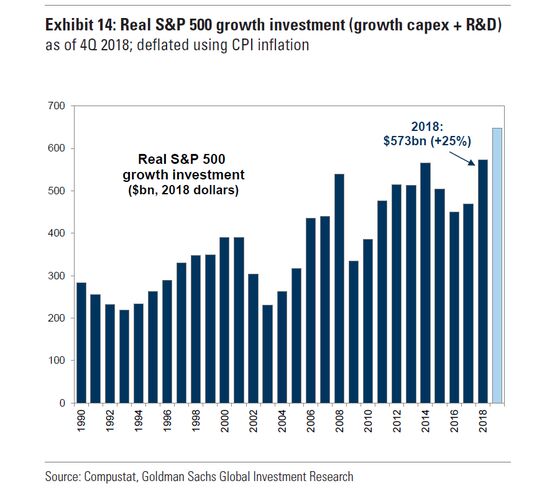

U.S. companies have “consistently” returned cash to shareholders for almost 140 years, so it’s far from a new development, strategists led by David Kostin wrote in a note Thursday. And buybacks don’t dominate corporate spending, they said -- growth investment has been the largest share of U.S. companies’ spending every year since at least 1990.

“One of the greatest misconceptions in the public discourse surrounding corporate buybacks is the belief that managements repurchase stock in an attempt to inflate earnings per share and meet incentive compensation targets,” Goldman wrote. “Executives whose compensation depends on EPS,” they said, “did not allocate a higher proportion of 2018 total cash spending to buybacks than companies where management pay is not linked to EPS.”

Buybacks have been getting increased scrutiny in the wake of the tax reforms in late 2017, when companies used money saved from the lower levies to return cash to shareholders. Republican Senator Marco Rubio of Florida released a plan last month that would curb buyback incentives. Democratic Senator Chris van Hollen of Maryland may propose legislation curbing executive share sales after repurchase announcements.

That’s after Democratic Senator Chuck Schumer and Senator Bernie Sanders, an independent who caucuses with Democrats, wrote an opinion piece in the New York Times arguing for limits on buybacks. Goldman’s ex-CEO Lloyd Blankfein issued a rebuttal defending the practice on Twitter, saying the money “gets reinvested in higher growth businesses that boost the economy and jobs.”

Growth investment “has accelerated sharply” since the tax reforms passed, contradicting “the widespread belief” that the changed policies led only to a surge in share repurchases, Goldman said. Companies have boosted buybacks relative to dividends to repatriate overseas profits and because of greater flexibility to match earnings volatility, the strategists added.

The tax-law changes did sharply boost cash spent on buybacks, with a 52 percent jump in 2018 to $819 billion for S&P 500 companies, the report said. Goldman estimates that will rise to $940 billion this year.

“Much of the cash that firms repatriated in 2018 has been recycled back into the domestic economy through a combination of both buybacks and dividends,” the report said.

Goldman found that firms with EPS-linked incentive compensation actually spent a greater portion of their cash on dividends than those without, even though executives in the first category would have had financial incentives to prefer repurchases. Further, the report said, evidence suggests buybacks aren’t crowding out capital investment. The pace of growth investment may even be accelerating.

“Corporates are generally efficient allocators of capital,” Goldman wrote. “We find some evidence that the companies that are able to generate the highest returns on assets are also those that invest the most in growth capex and R&D,” while “firms that generate lower asset returns may find the economics of cash return to shareholders to be superior to investing for growth.”

--With assistance from Kathleen Hunter.

To contact the reporter on this story: Joanna Ossinger in Singapore at jossinger@bloomberg.net

To contact the editors responsible for this story: Christopher Anstey at canstey@bloomberg.net, Teo Chian Wei, Ravil Shirodkar

©2019 Bloomberg L.P.