Goldman Says Narrow Breadth in S&P 500 a Bad Sign for Stocks

The U.S. benchmark is around 17% below its February record, but the median stock trades 28% from its peak.

(Bloomberg) -- The narrowing group of winners in the S&P 500 doesn’t bode well for the future performance of U.S. stocks, according to Goldman Sachs Group Inc.

The U.S. benchmark is around 17% below its February record, but the median stock trades 28% from its peak, Goldman strategists including David Kostin wrote in a note Friday. Meanwhile, the five largest companies make up 20% of the gauge’s market capitalization, exceeding the 18% level the measure reached in March 2000 and raising investor concerns about narrow market breadth, they said.

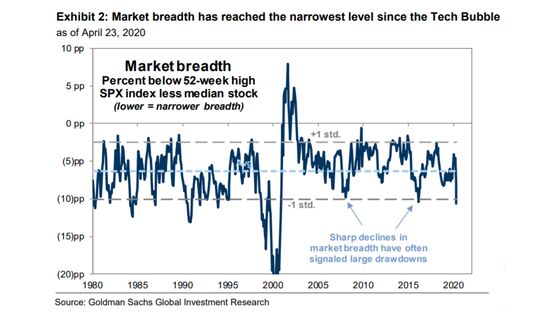

“Sharp declines in market breadth in the past have often signaled large market drawdowns,” the strategists wrote. “Narrow breadth can last for extended periods, but past episodes have signaled below-average market returns and eventual momentum reversals.”

Breadth narrowed ahead of the recessions in 1990 and 2008, in the tech bubble, and during the economic slowdowns of 2011 and 2016, according to the note. In the recent rally, market leaders have been the same large-cap, strong-balance sheet stocks that had been outperforming before the outbreak, resulting in a surge in already-elevated market concentration, it said.

Goldman’s caution dovetails with that of Bloomberg Intelligence Chief Equity Strategist Gina Martin Adams, who said in a report Thursday that that U.S. equity breadth has not moved at a pace consistent with strong rallies off lows. Less than half the members of the S&P 500 were trading above their 50-day moving average, she noted.

In early February, before the coronavirus sell-off, Kostin and his team had downplayed the dominance of large-cap technology giants in the U.S. benchmark, arguing that lower growth expectations, lower valuations and greater reinvestment could help them sustain their leadership.

©2020 Bloomberg L.P.