Goldman's CDS Dance With Hedge Funds Lands It in New Legal Mess

Goldman Is Sued by Merger Client Over Costly Loan Changes

(Bloomberg) -- Just three months ago, Goldman Sachs struck an unusual deal with a group of hedge funds to offload a buyout loan from its books -- saving the bank and the funds from potential losses.

Now, that odd arrangement is at the center of a lawsuit accusing the Wall Street firm of gorging on fees while exposing the acquirer in the buyout, United Natural Foods Inc., to hedge-fund sharks who stand to reap gains if it falters. United Natural had hired Goldman Sachs for the takeover and is now demanding at least $52 million -- and potentially much more -- from the bank.

“I have never experienced this kind of egregious and immoral behavior from a bank in my entire life,” United Natural Chief Executive Officer Steve Spinner said in an interview after his company filed the suit Wednesday in a state court in New York. Goldman vowed to vigorously fight the case, calling it “entirely without merit.”

The latest drama focuses on the much-maligned credit-default swaps market, where hedge funds and others wager on the ability of companies to keep up with their borrowings. Again and again, the contracts have played strange roles in debt transactions, sometimes straining allies or encouraging unlikely alliances.

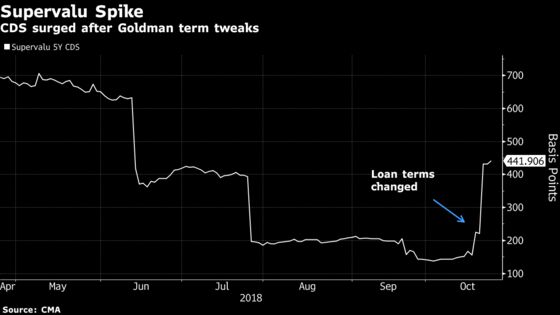

The lawsuit describes the bank’s attempt to tweak the terms on a $2 billion financing deal in a way that allowed hedge funds to reap a windfall from their CDS bets, as first reported by Bloomberg in October. United Natural said it heeded the bank’s advice, agreeing to changes so it could complete the takeover of grocery chain Supervalu.

The moves effectively enlisted the help of hedge funds that had been betting on Supervalu’s demise. Those funds now stand to benefit if United Natural struggles to repay.

United Natural is also claiming the bank unfairly withheld fees, burdened it with additional interest expenses and relied on “scare tactics” by a senior banker to back it into a corner.

United Natural, a supplier to Whole Foods, announced the $2.9 billion Supervalu acquisition in July. At the time, the buyer said Goldman Sachs Group Inc. would act as lead underwriter for debt supporting the deal. But as markets made investors skittish, the investment bank faced the prospect of being saddled with losses.

Hedge funds were facing losses too. They had been betting against Supervalu’s debt, but the company’s sale threatened to create a situation known in market parlance as an orphaned CDS contract. Because new debt being issued to purchase Supervalu would have paid down the grocer’s obligations, it could have made swaps linked to Supervalu effectively worthless -- referencing an entity with no significant borrowings.

‘Would Get Ugly’

The key was to restore the value of the roughly $470 million of net CDS wagers linked to Supervalu’s debt. The cost of those derivatives had plunged through most of last year. But by tweaking the loan documents to make Supervalu a co-borrower on the new financing, Goldman sparked a surge in the value of the swaps. That, along with several other concessions, helped the bank fill its order book for the loan.

United Natural claims that Goldman left it exposed to a group of lenders whose interests are at odds with its own and who are motivated to create roadblocks aimed at forcing a default so that they can notch further gains in the CDS market.

The company said it never received a final list of funds participating in the loans and, had it known, would’ve raised concerns.

Yet, Goldman and lenders including Bank of America Corp. that helped with the syndication, might have struggled to place the deal without making concessions for the hedge funds.

United Natural said it went along with the changes after warnings from Stephan Feldgoise, who helps oversee Goldman’s mergers business in the Americas. The bank allegedly warned that if the company didn’t adjust the terms, it might “scare off” investors, trigger “blowback” from its own shareholders and “things would get ugly.”

Feldgoise and Bank of America are also named as defendants. A Goldman spokeswoman declined to comment on his behalf. And a Bank of America spokesman also declined to comment.

It’s another twist in Feldgoise’s time at Goldman Sachs, which included a stint as chairman of the firm’s global fairness committee. In mid-2017, division chiefs announced he would be departing the bank, stepping down from his post in senior management to become an advisory director. Yet he’s still at the bank, now in a heated battle with a client for whom he’s handled various deals.

--With assistance from Davide Scigliuzzo.

To contact the reporters on this story: Sridhar Natarajan in New York at snatarajan15@bloomberg.net;Chris Dolmetsch in Federal Court in Manhattan at cdolmetsch@bloomberg.net

To contact the editors responsible for this story: Michael J. Moore at mmoore55@bloomberg.net, ;David Glovin at dglovin@bloomberg.net, David Scheer, Dan Reichl

©2019 Bloomberg L.P.