Goldman Managers Say Buy U.S. Stocks Despite Dot-Com Valuations

Goldman Managers Say Buy U.S. Stocks Despite Dot-Com Valuations

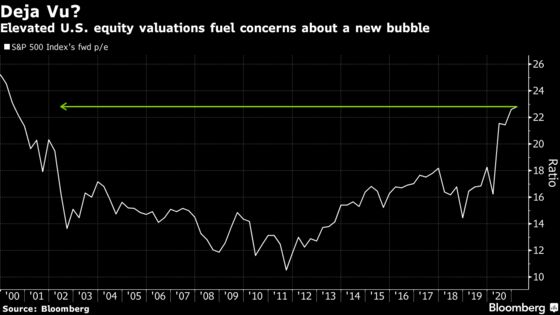

(Bloomberg) -- U.S. stocks are the most expensive since the dot-com bubble, but to Goldman Sachs Group Inc.’s $575 billion wealth management division, they’re still the best game in town.

Strategists there are telling clients to cast aside valuation worries as the S&P 500 soars to records through the pandemic. It’s all justified in a world of rock-bottom interest rates and where U.S. profit growth is faster than just about anywhere.

“When we look at these companies, they’ve not reached the types of valuations that would imply a fundamental scenario that just defies reason,” Brett Nelson, head of tactical asset allocation for the group, said on a call with reporters on Friday. “That was the case back in the late 1990s.”

Goldman’s wealth-management team says they expect the S&P 500 to post a return of about 8% this year on earnings growth of about 26%, which is slightly above consensus. While U.S. equities currently trade near forward price-to-earnings levels last seen in 2000, it says the key difference is that some of today’s most popular stocks, such as Apple Inc. and Facebook Inc., have positive free cash flows.

Conviction on the U.S. recovery is spurring strategists to go all-in on America First trades, recommending cheaper value shares and small-cap U.S. stocks. Equities outside the U.S. may trade at a discount to the S&P 500, but Goldman’s strategists say valuation concerns are no reason to overweight European or emerging-market stocks which have inferior earnings potential.

Reflation trades are the talk of Wall Street in the wake of last week’s Georgia victories for the Democrats -- making it easier to push through more aggressive fiscal measures. In the view of Goldman, however, the Democrats’ control of the Senate won’t guarantee passage of the more aggressive fiscal policies, another bullish set-up for equities.

“Our view is that it’s very much a government that is divided between Republicans and Democrats, and it’s very tight,” said Sharmin Mossavar-Rahmani, chief investment officer for wealth management at Goldman Sachs.

Another reason to overweight equities: Goldman projects negative returns for Treasuries in 2021 thanks to the global economic recovery, already low rates and stimulus measures.

“That’s the first time we’ve ever forecast negative returns for U.S. Treasuries over a five-year period going back to the Great Financial Crisis,” said Nelson.

While 10-year benchmark yields are expected to rise, they’re unlikely to reach a 3% tipping point that would tighten financial conditions and undermine the case for equities, Goldman’s strategists said.

©2021 Bloomberg L.P.