Goldman Joins Loomis in Turning Bearish on Indonesian Rupiah

Goldman Joins PineBridge in Going Bearish on Indonesian Rupiah

(Bloomberg) -- Follow Bloomberg on LINE messenger for all the business news and analysis you need.

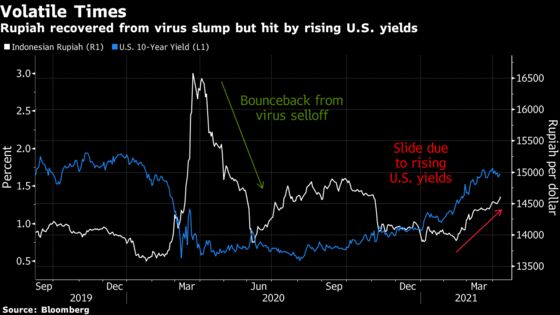

Indonesia’s central bank says the rupiah is “very undervalued” following a two-month slide. Investment banks and money managers are predicting further losses.

Goldman Sachs Group Inc. says climbing U.S. yields and a potentially firmer dollar will keep hurting Indonesian assets in the near term, while PineBridge Investments Asia Ltd. says the rupiah will keep sliding due to the global risk-off trade and as overseas funds take home dividends. Loomis Sayles Investment Asia Pte. is bearish due to the Covid-19 situation.

The rupiah has dropped 3.8% this year, the worst performer in emerging Asia after the Thai baht, as surging U.S. Treasury yields led to an outflow of funds from emerging-market assets. The currency fell as low as 14,635 per dollar on Tuesday, the weakest level since November.

“The rupiah is among the most vulnerable among high-yield emerging-market currencies under risk-off sentiment,” said Arthur Lau, head of Asia ex-Japan fixed income at PineBridge in Hong Kong. “In the coming months, we expect the weakness of the rupiah to remain due to seasonal dividend and coupon repatriation in April-May and higher seasonal imports in the second quarter.”

Indonesia’s currency is seen as a bellwether of risk in emerging Asia due to the relatively high foreign ownership of local assets and its generally open economy. The rupiah’s prolonged slide suggests there is a deeper shift away from developing nations than just a pullback from last year’s liquidity-fueled surge.

Emerging-market stocks, bonds and currencies have all declined over the past three months with the biggest foreign-exchange losses in Brazil, Argentina and Turkey.

| Read More: |

|---|

| Indonesian Rupiah Is ‘Most Overheld’ Currency in APAC, BNY Says |

| Specter of Worse Emerging-Market Rout Drives Loomis Fund to Sell |

“One of the most frequently asked investor questions in recent weeks has been whether it is time to buy the dip in Indonesia local markets?” Goldman Sachs analysts led by Zach Pandl in New York wrote in a research note this month. “The answer is ‘not yet’, in our view.”

Goldman says its analysis indicates Indonesian bonds are not yet in cheap territory, and strong U.S. data suggests there’s the potential for even higher Treasury yields, which would be a further negative for the Asian nation’s assets.

Bank Indonesia sees the rupiah rebounding due to the country’s low inflation and improving economic growth. Meanwhile, policy makers will seek to stabilize the currency in line with its fundamentals, Deputy Governor Dody Budi Waluyo said last week.

Amundi Singapore Ltd. is also positive over a longer horizon.

“Over the medium term, Indonesia will benefit from structural tailwinds, such as further finalization and implementation of the omnibus law, and from the relatively quicker economic recovery post-Covid,” said Joevin Teo, head of investment in Singapore. “This should continue to bolster investor interest and inflows in both the bond and currency markets.”

Back among the bears, Loomis Sayles believes there’s little reason to be positive about the rupiah at present, especially with the country struggling to bring the coronavirus under control.

“The fundamental reason for being bullish rupiah right now isn’t there,” said Thu Ha Chow, a portfolio manager at the firm in Singapore. In addition to the risk of a rising dollar and U.S. yields, “there’s no massive turnaround story in terms of what’s going on with the Covid situation,” she said.

©2021 Bloomberg L.P.