Goldman Fund Makes Record Retreat From Muni Junk Bonds Over Risk

Goldman’s high-yield muni fund had beaten more than 90 percent of its peers over the last five years.

(Bloomberg) -- Goldman Sachs Group Inc. has shifted money to the sidelines of the municipal junk-bond market, waiting for it to crack.

The company’s $7.3 billion High Yield Municipal Fund, the third biggest focused on the riskiest state and local government debt, had about 62 percent of its assets in investment-grade securities by the end of April. It marks the fund’s biggest move ever away from the lowest-rated bonds and a wager that the run-up in prices will reverse as speculative projects start to run into distress, said Ben Barber, head of municipal bonds at Goldman Sachs’s asset management arm, which oversees $62 billion of the securities.

"What we’re hoping for is there’s a new round of opportunities in the muni market over the course of 2019 or 2020," he said in an interview. Goldman’s high-yield muni fund beat more than 90 percent of its peers over the last five years.

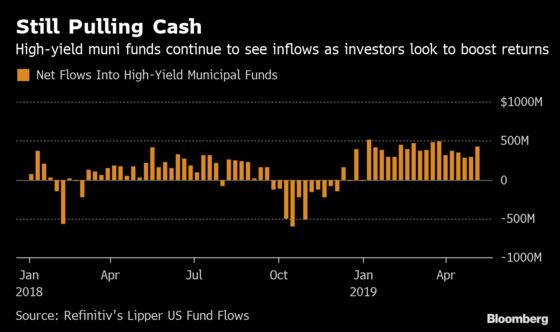

Barber is adding to a small but growing chorus on Wall Street that’s raising concerns about a corner of the $3.8 trillion municipal market that finances shopping malls, charter schools, retirement homes and speculative business ventures. Investors have piled into such securities as low interest rates leave them hunting higher yields, driving the sector to a 5.7% return this year, according to the Bloomberg Barclays index. Analysts from Bank of America Corp. and UBS AG have recommended that investors back off amid uncertainty over whether the decade-long expansion will continue.

But Goldman’s pullback stands in contrast to other big high-yield municipal bond funds. Nuveen’s $19.3 billion fund, the largest tracked by Bloomberg, had just 20.7 percent exposure to investment-grade debt at the end of April. Invesco Ltd.’s $10 billion high-yield municipal fund, the second-biggest, had about one-third of its holdings in debt with better-than-junk grades.

Securities sold for speculative ventures are one of the few risky areas of a market that’s otherwise a haven from defaults, since most debt is backed by states and cities with the power to raise taxes.

Projects financed with municipal bonds typically can pay investors from a capitalized interest fund for about two years as they get off the ground, Barber said. Many may find it challenging as they reach the point soon when they will need to start generating money to pay their debts, he said.

"You’ve got a lot of deals that will have to stand on their own two feet this year and next," he said. "That could create some pretty good opportunities in the high-yield market."

In the meantime, Barber’s high-yield fund, which has returned over 8% over the past year, has been buying investment-grade bonds, such as general-obligation debt backed by governments’ revenue collections.

The fund owns debt issued by Illinois, the lowest-rated state, Chicago and the New Jersey Transportation Trust Fund Authority, all of which Barber said have been "beaten down" over concerns around their finances.

"You’re talking about sectors that are truly traditional municipal finance that have been beaten down," Barber said. "Our job is to find out whether they’re beaten down too much and what’s a good entry point. They’re still held in a high conviction."

--With assistance from Danielle Moran.

To contact the reporter on this story: Amanda Albright in New York at aalbright4@bloomberg.net

To contact the editors responsible for this story: James Crombie at jcrombie8@bloomberg.net, William Selway, Michael B. Marois

©2019 Bloomberg L.P.