Goldman Asset Sees Rate Cuts Sustaining Rally in EM Bonds

Goldman Asset Sees Rate Cuts Sustaining Rally in Emerging Bonds

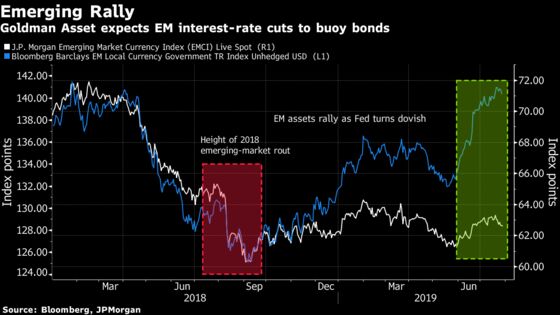

(Bloomberg) -- The building blocks for a sustained rally in emerging-market bonds are in place as their central banks embark on a rate-cutting cycle, according to Goldman Sachs Asset Management.

Last month’s easing by South Korea, Indonesia and South Africa is a foretaste of things to come as policy makers step up efforts to bolster growth, said Angus Bell, a senior portfolio manager who helps oversee $45 billion of developing-nation debt. A dovish Federal Reserve and improved local fundamentals will only embolden EM central banks to push rates lower, he added.

“We continue to like the idea of owning emerging-market local rates,” Bell said in an interview in Singapore before the Fed’s decision to cut U.S. rates. “We now find ourselves almost in perfect alignment where developed-market central banks are easing, EM central banks’ shackles are off. There are still opportunities and I still think there’s more to go.”

Goldman Sachs Asset joins peers like BlueBay Asset Management in predicting more gains even as a Bloomberg Barclays index of local-currency EM bonds has climbed 6.9% in 2019. Investors have been piling into the high-yielding securities as the Fed’s signal to ease policy amid faltering global growth saw the amount of negative-yielding bonds around the world rise to $14.1 trillion.

The Fed on Wednesday delivered the widely-expected interest-rate cut, but Chairman Jerome Powell said the first reduction since the financial crisis was to “insure against downside risks” and didn’t signal the start of a lengthy easing cycle.

“We should acknowledge that the market has moved very very quickly to pricing in rather dovish outcomes for the Fed,” said Bell. “We’re not taking a super aggressive directional view on U.S. rates across our EMD portfolios at the moment.”

Preferred Picks

Goldman favors local-currency government debt in Korea, Indonesia and South Africa, he said, adding that the money manager is also buying Russia’s ruble, the Brazilian real and the Indonesian rupiah for carry.

Bank Indonesia, Bank of Korea and South Africa’s central bank all lowered rates by a quarter of a percentage point in July, while Turkey slashed its benchmark by 425 basis points, the biggest reduction in 17 years.

READ: JPMorgan Asset Favors EM and High-Yield Bonds as Fed Cuts Rates

“The level of vulnerabilities in aggregate across EM are relatively controlled and contained,” Bell said. “We are not in an environment where people are talking about the Fragile Five, and indeed if you look at aggregate current accounts, they’re relatively balanced at the moment.”

The BOK could consider additional monetary-policy response if economic conditions at home and abroad worsen and downside risks grow, Yonhap News reported Thursday, citing a central bank statement provided to parliament.

Still, some other investors are less sanguine. S.E.A. Asset Management Pte and Schroder Investment Management Ltd. warn that enthusiasm for easy monetary policy may have gone too far and lingering U.S.-China trade tensions could eventually curb appetite for riskier assets.

Here are some more of his comments:

What is your outlook for Turkey?

“If past behavior is anything to go by, the central bank is perhaps being quick to lower rates before they’ve seen the subsequent decline in inflation – so that’s what we’re watching very, very closely. We have had some selective positions in the dollar bonds, where we think ultimately in the probability of default, we think we’re getting appropriately compensated.”

How will the U.S.-China trade war pan out?

“The key question really remains as to whether or not these broader disagreements with respect to technology transfer, intellectual property rights et cetera can be sufficiently resolved -- our fear is that those themes will be more challenging to find an immediate agreement on.”

Where do you see the 10-year Treasury yield by year-end?

“Where the U.S. rate curve is pricing things at the moment, to us, seems appropriate. It’s not going to surprise us if we see the 10-year trade in a range somewhere they are today, which is just above 2%.”

--With assistance from Chester Yung.

To contact the reporter on this story: Ruth Carson in Singapore at rliew6@bloomberg.net

To contact the editors responsible for this story: Tan Hwee Ann at hatan@bloomberg.net, Shikhar Balwani, Liau Y-Sing

©2019 Bloomberg L.P.