Goldman's Copsey Keeps Faith in Stocks Amid ‘Overdone’ Bond Run

Goldman's Copsey Keeps Faith in Stocks Amid ‘Overdone’ Bond Run

(Bloomberg) -- It’s hard enough to find a stock bull these days. But one sanguine enough about the economic outlook to forecast just one more rate cut this year? That’s a contrarian.

While Goldman Sachs Group Inc.’s investment management arm is still waiting for better entry levels to buy the dip, it continues to favor equities and credit over government bonds in a rejection of growing fears of an imminent recession. The unit, which oversees about $1.7 trillion, expects the Federal Reserve to lower rates only once more in 2019 before eventually returning to a hiking cycle, versus the futures market that’s pricing in a good chance of three more cuts.

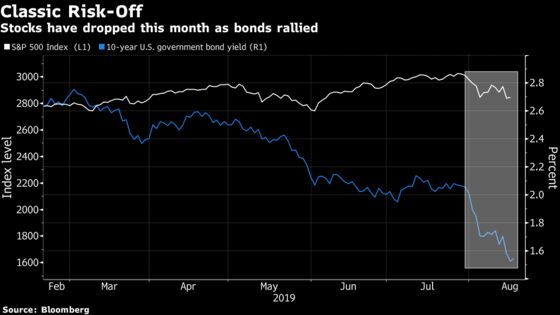

Goldman’s stance goes against the consensus investor view that has triggered a rally in bonds while punishing stocks in August. Bond funds saw the fourth-biggest ever week of inflows through Aug. 14, while equity funds saw outflows, according to a Bank of America Corp. report.

“We don’t subscribe to the view that this is the end of the business cycle,” said London-based executive director David Copsey, who is part of the global portfolio solutions group managing about $122 billion at Goldman Sachs Asset Management. “If our central thesis comes true -- which is economic growth continues to slow from an elevated level but remains around trend in the second half of the year and recessionary risk is low -- we would believe core inflation will gradually continue to grind higher.”

Ripe for Contrarians

With global shares erasing $4 trillion this month, the riskiest credit buckling and government bonds reaching parabolic levels, the time seems ripe for contrarian bullishness. But it’s not for the faint of heart: securities have swung wildly all week between conflicting trade headlines and a bond market flashing recessionary signals.

Copsey rejects several of the market’s glummest theses. An inverted yield curve isn’t always immediately followed by a recession, he stresses. In his view, the usual signals of fragility -- debt levels of households and non-financial corporations -- are still quite benign. The U.S. core personal consumption expenditure index, one measure of inflation, has been picking up, he notes.

He also doubts the current impact of the U.S.-China trade war will be strong enough to end the global growth cycle.

“There’s potentially a natural barrier on how bad things can get because ultimately while both sides have credible concerns and credible agendas that they’re looking to pursue, neither of them wants to ultimately negatively affect their domestic long-term growth prospects,” he said by phone late Thursday.

Credit Suisse Group AG strategists too argue that the yield curve is not necessarily flashing a sell sign for equities. The most dependable signals still show a recession is unlikely before 2021, they wrote in a note Thursday, saying they are overweight European cyclicals -- some of the most beaten up stocks in this month’s sell-off.

Some dip-buying was evident on Friday. The S&P 500 climbed 0.9% as of 9:42 a.m. in New York, while the Stoxx Europe 600 was up 1%.

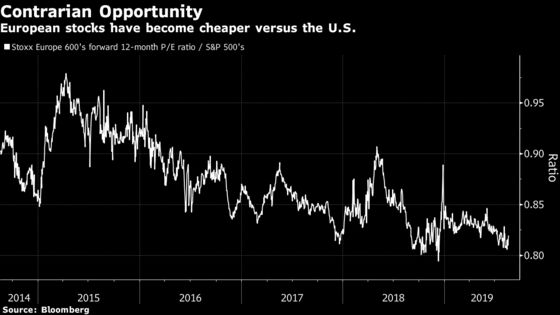

Within stocks, Copsey’s team is looking for shares with high dividends and dislocated value rather than exposure to the market’s broader direction or cyclical risk. Another contrarian view: it’s overweight Europe, especially economies such as Spain’s that are more domestically driven, as that region is cheaper and some temporary headwinds to growth should fade, he said. It’s neutral on the U.S. and emerging markets.

As for government bonds, he says they’ve probably run their course.

“The reaction from bonds is probably somewhat overdone now,” Copsey said. “To justify these yield levels and the market pricing of rate cuts, we would need to see a further deterioration in the growth data, beyond our current expectations.”

To contact the reporter on this story: Justina Lee in London at jlee1489@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, Namitha Jagadeesh, Jon Menon

©2019 Bloomberg L.P.