Global Bond Sell-Off Persuades Some Investors to Buy the Dip

And it appears some are pouncing, with traders cashing out bearish wagers and buy-the-dip buyers rushing in Thursday afternoon.

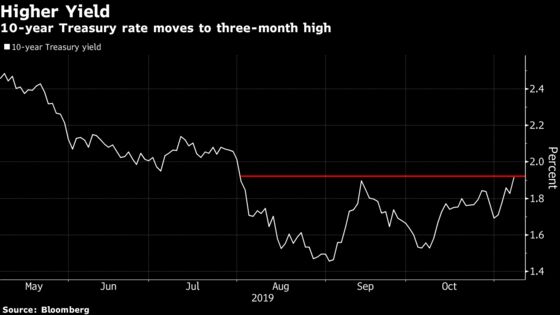

(Bloomberg) -- Recent losses in Treasuries, which crescendoed Thursday into one of the worst days since Donald Trump was elected president, look like a buying opportunity for many investors who have a grim view of the economy’s prospects.

And it appears some are pouncing, with traders cashing out bearish wagers and buy-the-dip buyers rushing in. The rekindled interest in the safety of bonds nudged yields on the 10-year, which had climbed to a three-month high of 1.97% on Thursday, down to as low as 1.89% in early European trading Friday before bouncing back to around 1.94%. European bonds rebounded after French and Belgian yields had climbed above 0% Thursday.

Signs of progress in U.S.-China trade talks have thrashed bonds for days, and the two countries agreed Thursday to roll back tariffs on each other’s goods if a deal is reached. The Treasury market has seen a huge turnaround since August, when fears that global growth is slowing prompted the biggest monthly rally since 2008.

“Sentiment factors have shifted the needle quite quickly from, ‘Oh, it’s the end of the world,’ to ‘Wow, there are no problems,’ and that’s a massive overreaction,” Aberdeen Asset Management’s James Athey said in an interview this week with Bloomberg Television. The sell-off has “absolutely, without question” created a buying opportunity, particularly if the 10-year yield hits 2%, he said.

The U.S. is the most attractive government-bond market to own, given that the dollar remains the world’s reserve currency and the Federal Reserve has the most room to cut rates before it gets to zero, “if you believe like I do that we’re headed to a recession,” Athey said.

Athey was joined by Barclays Plc, which recommended investors enter long positions in five-year Treasuries, and JPMorgan, who said traders should bank the profits made by shorting their three-year counterparts.

Money manager Raymond Lee at Kapstream Capital also expects the sell-off to be contained, saying there’s value in developed markets with positive bond yields such as the U.S.

“I don’t expect to see two or three years of rates backing up in a sustained way,” he said in an interview in Singapore. “Yields may bounce around on headlines a bit, but inflation is still contained and rates are likely to stay low.”

Option Traders

For some Treasury options traders, the sell-off was reason to scoop up profits on lucrative one-week bets that called the recent climb in yields. The trades were struck last week when the 10-year yield was around 1.70% and netted a profit of more than $40 million as the level breached 1.90% on Thursday.

Diminished appetite for government debt is pushing the 10-year yield toward 2%, a level it hasn’t surpassed since Aug. 1. It’s also sent yields on French and Belgian 10-year securities above zero for the first time in months.

Some are suggesting the sell-off hasn’t gone far enough. Bond valuations “still look rich,” particularly in Europe where negative yields are pervasive, said Scott Thiel, chief fixed-income strategist for BlackRock Investment Institute.

As Athey sees it, trade policy wasn’t the biggest factor behind broader worldwide weakness in the past 12 to 18 months. Instead, China is undergoing a secular shift in the pace and make up of its growth that leaves the country “less impactful” on the global economy. There’s “really not much left in the engine of global economic growth at this stage,” he said.

--With assistance from Ruth Carson and John Ainger.

To contact the reporters on this story: Vivien Lou Chen in San Francisco at vchen1@bloomberg.net;Edward Bolingbroke in New York at ebolingbrok1@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Nick Baker, Boris Korby

©2019 Bloomberg L.P.