Central Banks Fight Bond Rout With Action and Promise of More

The resolve of central banks trying to curb rising market interest rates is being tested.

(Bloomberg) -- Central banks from Asia to Europe escalated their efforts to calm panicking markets, pledging to buy more bonds and signaling more policy accommodation, after U.S. Treasury yields surged to the highest level in a year.

The Reserve Bank of Australia waded in with more than $2 billion of unscheduled purchases, while Korea announced buying plans for the next few months. European Central Bank Executive Board member Isabel Schnabel said more stimulus could be added if the surge in yields hurts growth.

While the response appeared to calm bond investors, it’s unlikely to bridge a deepening divide between traders and central banks over the pace of the economic recovery. Officials fear the so-called reflation trade, already rippling through all markets, could seep into economies that have yet to rebound from the coronavirus shock.

”Do central bankers come out and effectively put their foot down? We obviously saw some big buying in Australia out of sync with their normal program. That hasn’t helped dramatically,” Iain Stealey, international chief investment officer of global fixed income at JPMorgan Asset Management told Bloomberg Television.

The ECB, for example, has “more ammo, but as we know, the talk is fairly empty,” he said.

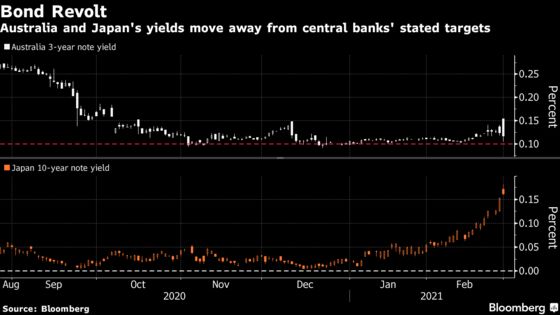

In the Asia-Pacific region, the RBA is taking the lead in acting as a breakwater for rising yields, a role typically played by the Bank of Japan. Its offer to buy A$3 billion ($2.4 billion) of debt acted to brake the selloff, with Australia’s three-year bond yield erasing gains. Treasury yields also came down from the 1.61% highs reached Thursday night as Asian investors piled in.

While the BOJ hasn’t acted, Finance Minister Taro Aso fired a warning shot as the benchmark yield surged to within a couple of basis points of the perceived top of the central bank’s target zone. “It’s important that yields don’t suddenly jump up and down,” said Aso in Tokyo. “We need to make sure not to lose the market’s trust with fiscal management.”

Governor Haruhiko Kuroda later said the BOJ won’t change its yield target, and wants to keep the nation’s yield curve low.

Read: BOJ’s Tolerance for Rising Yields Tested Before Policy Review

In Europe, German bonds rallied on Friday, with the yield on 30-year debt falling three basis points to 0.21%. Italian benchmark debt also reversed a slide at the open to trade higher, with the 10-year yield down one basis point at 0.79%.

The move coincided with ECB officials escalating their rhetoric against excessive market optimism about the state of the euro area economy.

“A rise in real long-term rates at the early stages of the recovery, even if reflecting improved growth prospects, may withdraw vital policy support too early and too abruptly given the still fragile state of the economy,” said Schnabel, who is responsible for the ECB’s market operations. “Policy will then have to step up its level of support.”

There are expectations that global central banks will try to contain a further rise in yields, said Kei Yamazaki, a senior fund manager in Tokyo at Sumitomo Mitsui DS Asset Management. “Fed officials have been tolerating the recent rise in yields, but the current risk-averse market will also prompt them to calm the market verbally.”

While markets are increasingly pricing in higher inflation and the potential for rate hikes, every major central bank from the Federal Reserve to the ECB see a prolonged period of easing as economies gradually recover. That would suggest this week’s tussle is set to continue.

“Selling begets more selling,” said John Pearce, chief investment officer of UniSuper Management Pty. in Sydney. “In the short-term it doesn’t look like it’s stopping.”

©2021 Bloomberg L.P.