German Stocks Keep Shrugging Off the Weak Economy: Taking Stock

German Stocks Keep Shrugging Off the Weak Economy: Taking Stock

(Bloomberg) -- Watching Tiger Woods winning the Masters again can tell one thing: comebacks are possible. The Stoxx Europe 600 is still a few percent away from its 2018 highs. It’s a decent performance, especially judging by an economic outlook that is not getting any brighter.

Capping off some dismal manufacturing indicators this year, the German government is likely to halve its growth expectation from 1% to 0.5% tomorrow, according to a Der Spiegel report last week. Investors are likely to not care, already eyeing better times.

Judging from the recent rebound in relevant stocks, the market has maneuvered for something better. While expectations into the earnings season remain rather low, the relative rate of earnings downgrades has slowed in recent months, and a weaker euro is providing exporters with some leeway. Autos have staged a nice comeback in April, and that’s playing positively for the DAX.

German Economy Minister Peter Altmaier’s Wednesday press briefing should bring one of the last institutions in line with the consensus, which has already firmly reduced its growth expectation for Europe’s biggest economy.

The German stock market is not the hottest place to be, especially when you look at the DAX without dividends. That said, they are still chasing historic highs and analysts at UBS recently voiced a bullish stance on German stocks, noting in a publication earlier this month that there is progress on some potential catalysts.

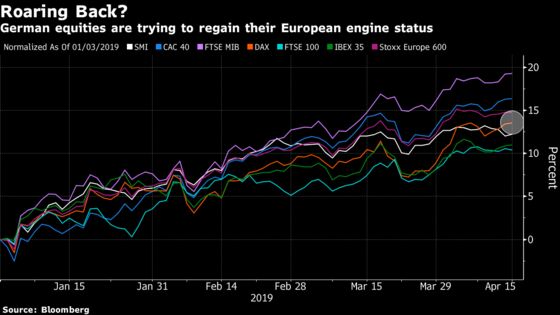

German equities, heavily skewed to exporters, are moving with the global trade sentiment. Trade talks have softened in recent months and the engagement between the U.S. and China isn’t as hostile as it was before. Improved Chinese macro data has sent some relief signals that help outweigh a still fragile domestic and European data.

Last week, Deutsche Bank strategists noted that despite a slump in exports last year, Germany is a beneficiary of China’s efforts to modernize its production facilities under the “Made in China 2025” strategy.

That may be part of the reason that while German stocks have underperformed their French and Italian counterparts and are lagging the broader Stoxx 600, they are up a decent 14% this year and doing a lot better than a couple of months ago, both in relative and absolute terms.

The gain already matches the forecast of analysts for the full year and momentum seems to slow, so we might be due for a breather now that we are entering earnings season. In the meantime, Euro Stoxx 50 futures are trading up 0.2% ahead of the open.

- Watch the debut of Europe’s biggest IPO so far this year: Nexi. A flurry of deals have already graced markets in the second quarter and investors also will be girding themselves for another potential float to come in the shape of Nordic buyout house EQT Partners. It could all result in a hangover for investors, but perhaps the cure is fewer unicorns and more unicorn IPOs.

- Watch trade-sensitive sectors as European negotiators got the green light to get started on trade negotiations with the U.S., with a target of getting something done by September. Meanwhile, the U.S. and China continue to talk, particularly on farm goods. The four biggest economies in the world are now gripped by trade negotiations.

- Watch for central bank policy impact as Chicago Fed President Charles Evans said he can see the central bank keeping rates where they are until late 2020, while the Fed is also starting to consider its employment mandate. In Europe, the ECB continues to argue that negative rates have been positive.

COMMENT:

- “The better economic data releases from China could not have come at a better time for German exporters facing the trade headwinds from their partners across the Atlantic,” Jefferies strategists write in a note. “While the earnings story is absent, monetary conditions remain loose while the worst of the technical action has passed, in our view. Despite the manufacturing PMI slumping to a July 2012 low, there are positive surprises from the construction & services sector. We recently turned bullish.”

COMPANY NEWS AND M&A:

- Telia to Buy Back Shares for SEK15b Over Three Years

- House Democrats Subpoena Deutsche Bank, Others Amid Trump Probe

- BMW Joins Volkswagen in Predicting Sales Growth: China Auto Show

- UniCredit Says Amount Previously Set Aside Sufficient for Fine

- Zalando Sees Positive 1Q Adjusted Ebit in Single-Digit Millions

- UBS Tops Asia Private Banking League for Sixth Straight Year

- Rio Warns More Disruption Ahead as Iron Ore Shipments Plunge

- Tenaris Says Argentine Court Reverses Decision Against Chairman

- Lufthansa Slumps to First-Quarter Loss as Fuel Costs Increase

- Novartis Says FDA Accepts Brolucizumab BLA, Sees End-2019 Launch

- Thales to Start Gemalto Buyout as Soon as Possible to Reach 100%

- VAT Group Expects 2Q Net Sales CHF125m-135m, Confirms Guidance

NOTES FROM THE SELL SIDE:

- Citi says a rebound in assets under management for Swiss banks will support recurring revenue streams, while concerns on the sector look overdone, raising its rating on Vontobel to buy from neutral. Citi stays overweight Swiss banks with buy ratings on all stocks covered; order of preference is Credit Suisse (also on Citi’s Focus List), EFG International, Vontobel, Julius Baer and UBS.

- Jefferies writes Barclays corporate and investment banking revenue likely to be slower than anticipated in 2019, albeit with easier comparatives for 2H. 2019 revenue estimates cut by ~4%, pretax profit by 8% on slower investment bank activity, modestly lower margins in U.K. business; similar cuts made for 2020 and new EPS estimates introduced for 2021. Kepps buy and raises PT to 280p from 263p.

TECHNICAL OUTLOOK for Stoxx 600 index:

- Resistance at 392.7 (July high); 403.7 (100% Fibo)

- Support at 385.7 (76.4% Fibo); 374.5 (61.8% Fibo)

- RSI: 66.5

TECHNICAL OUTLOOK for Euro Stoxx 50 index:

- Resistance at 3,516 (76.4% Fibo); 3,596 (May high)

- Support at 3,403 (61.8% Fibo); 3,309 (50% Fibo)

- RSI: 68.4

MAIN RESEARCH AND RATING CHANGES:

UPGRADES:

- Draegerwerk upgraded to hold at HSBC; PT 44 Euros

- LVMH upgraded to add at AlphaValue

- Ontex upgraded to buy at Kepler Cheuvreux; PT 25 Euros

- Rational upgraded to buy at Berenberg

- TomTom upgraded to buy at Kepler Cheuvreux; PT 9 Euros

- Vontobel upgraded to buy at Citi

DOWNGRADES:

- Anglo American downgraded to hold at HSBC; PT 23.40 Pounds

- BP downgraded to outperform at RBC; Price Target 6.25 Pounds

- Kongsberg downgraded to hold at SEB Equities; PT 135 Kroner

- VIB Vermoegen downgraded to hold at Bankhaus Lampe

- Worldline downgraded to hold at HSBC; PT 55 Euros

INITIATIONS:

- Adevinta rated new outperform at Macquarie; PT 99 Kroner

- Datagroup rated new buy at Quirin Privatbank AG; PT 46 Euros

- InterContinental Hotels rated new outperform at MainFirst

- LondonMetric rated new sector perform at RBC; PT 2.05 Pounds

- Melia Hotels rated new outperform at MainFirst; PT 9.50 Euros

MARKETS:

- MSCI Asia Pacific up 0.4%, Nikkei 225 up 0.3%

- S&P 500 down 0.1%, Dow down 0.1%, Nasdaq down 0.1%

- Euro little changed at $1.1304

- Dollar Index down 0.01% at 96.93

- Yen up 0.09% at 111.94

- Brent down 0.2% at $71/bbl, WTI down 0.1% to $63.4/bbl

- LME 3m Copper up 0.1% at $6485/MT

- Gold spot down 0.3% at $1284.5/oz

- US 10Yr yield down 1bps at 2.55%

MAIN MACRO DATA (all times CET):

- 10:30am: (UK) March Claimant Count Rate, prior 2.9%

- 10:30am: (UK) March Jobless Claims Change, prior 27,000

- 10:30am: (UK) Feb. Average Weekly Earnings 3M/YoY, est. 3.5%, prior 3.4%

- 10:30am: (UK) Feb. Weekly Earnings ex Bonus 3M/YoY, est. 3.4%, prior 3.4%

- 10:30am: (UK) Feb. ILO Unemployment Rate 3Mths, est. 3.9%, prior 3.9%

- 10:30am: (UK) Feb. Employment Change 3M/3M, est. 181,000, prior 222,000

- 11am: (EC) Feb. Construction Output MoM, prior -1.4%

- 11am: (EC) Feb. Construction Output YoY, prior -0.7%

- 11am: (GE) April ZEW Survey Current Situation, est. 8.5, prior 11.1

- 11am: (GE) April ZEW Survey Expectations, est. 0.5, prior -3.6

- 11am: (EC) April ZEW Survey Expectations, prior -2.5

--With assistance from Hanna Hoikkala.

To contact the reporters on this story: Michael Msika in London at mmsika4@bloomberg.net;Jan-Patrick Barnert in Frankfurt at jbarnert3@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, Kasper Viita

©2019 Bloomberg L.P.