FX May Be a Better Hedge Than Bonds in a Near-Zero World

FX May Be a Better Way to Hedge Than Bonds in a Near-Zero World

(Bloomberg) -- Bonds aren’t quite the hedge against equity losses that they used to be, and that could have more and more investors looking for answers in the foreign-exchange market.

With interest rates around the world near zero, it’s become much cheaper to bet against various currencies that are typically tied to the global growth outlook, such as the Australian dollar and the Norwegian krone. While many of these once had a significant rate premium over the likes of the U.S. dollar, that has shrunk drastically.

Investors shorting these currencies now give up very little in terms of rate differentials, or carry, even as their link to cyclical growth outcomes appears to remain intact. At the same time, government bonds have been relatively range-bound, blunting their ability to act as a shock absorber for equity losses and potentially imperiling the classic 60/40 portfolio.

“As government bond yields approach zero, their sensitivity to volatility events declines, reducing their efficacy as a hedge,” JPMorgan Chase & Co. strategist Meera Chandan wrote in a report Tuesday. “FX could thus see increased involvement from proxy-hedgers.”

| Related Stories |

|---|

In New 60/40 Portfolio, Riskier Hedges Are Displacing U.S. Debt The 40 in 60/40 Portfolios Is Getting Wilder and Wilder Rates Flash Danger for 60/40 Portfolios With Shrug at Stock Rout A $19 Billion Bond ETF Shows the ‘60/40’ Strategy Still Works |

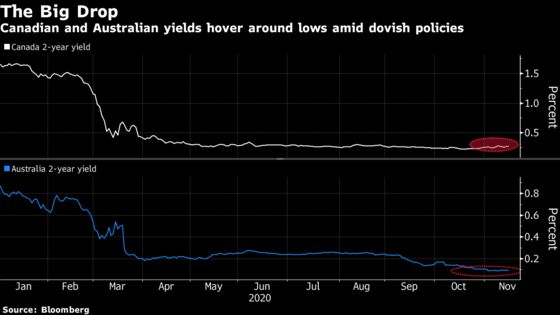

Spurred on by a wave of central bank easing, yields on Australian two-year notes have fallen to around 0.1% from close to 1% at the start of this year, while equivalent Canadian rates have slumped to less than 0.3% from almost 1.7%.

The carry cost of betting against developed-market cyclical currencies such as the New Zealand and Canadian dollars is “negligible,” according to Chandan, and in her view, the Norwegian and Australian currencies are the standouts.

Over the past five years, both have tended to move in line with equities as much as major emerging-market currencies like the South African rand and the Mexican peso, according to JPMorgan. “But the carry cost is a fraction by comparison,” Chandan wrote.

©2020 Bloomberg L.P.