Fund Manager Who Predicted India Credit Crunch Sees Risks

Suyash Choudhary said that “pockets of risk” remain that could reignite investor concern.

(Bloomberg) -- A fund manager who predicted India’s credit crunch months before it got serious last year said that “pockets of risk” remain that could reignite investor concern.

While the worst of the country’s liquidity shortage and soaring funding costs appears to have subsided for now, a string of corporate defaults suggests that those woes could come back, according to Suyash Choudhary, 40, head of fixed income at IDFC Asset Management Co.

“There is still a chance that two or three such risks can interact with one another and therefore cause something bigger,” Choudhary said in an interview. Two of IDFC Asset’s funds have given the best returns among the top debt funds in India over the past year, according to Value Research data.

More bad news out of India’s credit market in recent weeks suggests that investors may not have seen the last of turmoil sparked by shadow bank IL&FS Group’s debt default last year. Troubled Dewan Housing Finance Corp.’s rating was cut to default and that of Eros International Media Ltd. lowered 10 steps on concern about its ability to repay debt.

Also causing investor concern is news that the auditor of Indian tycoon Anil Ambani’s shadow bank and its unit resigned, citing lack of satisfactory responses to its questions. Nerves have already been rattled by defaults at Jet Airways India Ltd. and debt concerns at conglomerate Essel Group.

HDFC Asset Management Co, the country’s largest asset manager, Monday said that it has decided to provide a liquidity arrangement to certain of the fund’s fixed-maturity plans to deal with their exposure to bonds issued by troubled Essel Group companies.

Choudhary doesn’t claim credit for foreseeing the IL&FS default, but he said the red flags in the credit market were beginning to show a year or more before it.

There was a certain amount of euphoria as seen by a compression of spreads on lower-rated assets, major funds flows into such investments, and a larger inclination toward venturing into illiquid structured transactions, he said.

Things have improved since last year. The country’s sovereign risk premium is much better, especially after a strong election mandate, Choudhary said. There’s also reasonable confidence that regulators will step in to arrest the fallout if any risk event were to happen, he said.

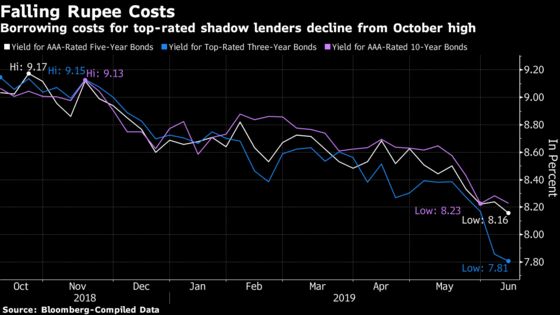

Average yields on top-rated five-year corporate bonds issued by non-bank finance companies have fallen to 8.25% on Monday, after soaring to as high as 9.22% in October, according to data compiled by Bloomberg.

A key risk, Choudhary sees, is in asset managers investing in lower-rated credit for portfolios which are ill-equipped to take such calls. That’s because secondary-market liquidity, price discovery or means of hedging risk haven’t kept pace with the market expansion, he said.

A stressed government fiscal situation and large debt supply means Choudhary’s area of preference remains bonds due in 10 years or less. He prefers top-rated corporate notes and government and state debt.

--With assistance from Divya Patil.

To contact the reporters on this story: Subhadip Sircar in Mumbai at ssircar3@bloomberg.net;Ragini Saxena in Mumbai at rsaxena30@bloomberg.net

To contact the editors responsible for this story: Tan Hwee Ann at hatan@bloomberg.net, ;Andrew Monahan at amonahan@bloomberg.net, Ken McCallum

©2019 Bloomberg L.P.